Labor’s fifth budget is, by any measure, a bold one. Framed around ‘resilience and fairness’, the 2026–27 budget delivers a trio of landmark tax reforms; to capital gains, negative gearing, and family trusts, alongside relief for everyday workers through new offsets and deductions. But for individuals and families reading closely, the budget is as notable for what it reverses as for what it introduces. Policies explicitly ruled out before the last election have been quietly revived. Tax cuts long promised and in some cases years in the making have been repackaged as fresh generosity. The overall picture is ambitious, consequential, and not without its contradictions.

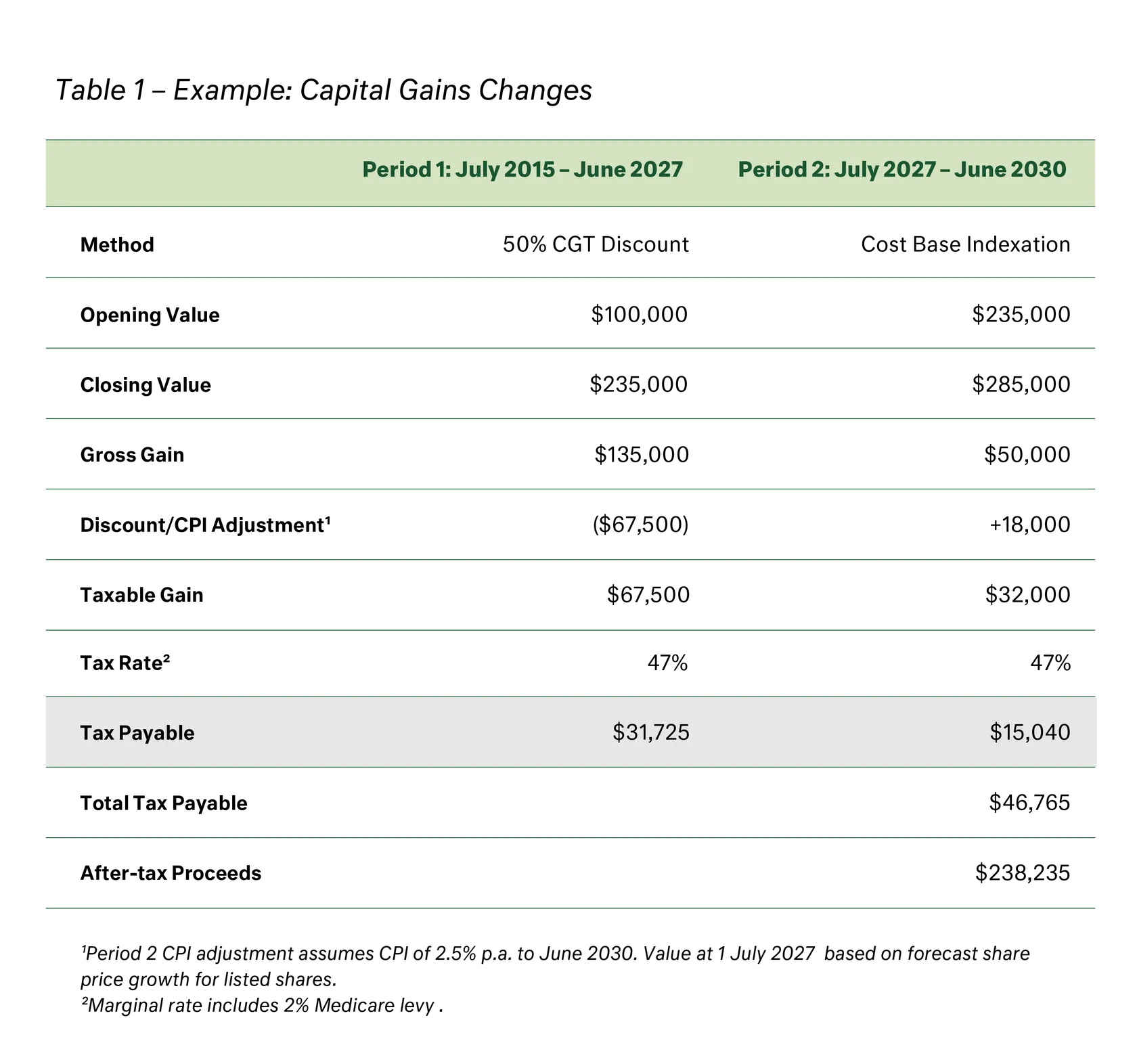

The budget introduces major changes to capital gains tax, negative gearing and family trusts. Together, these represent a significant structural shift in the tax system, with a focus on intergenerational fairness and increased taxation on capital.