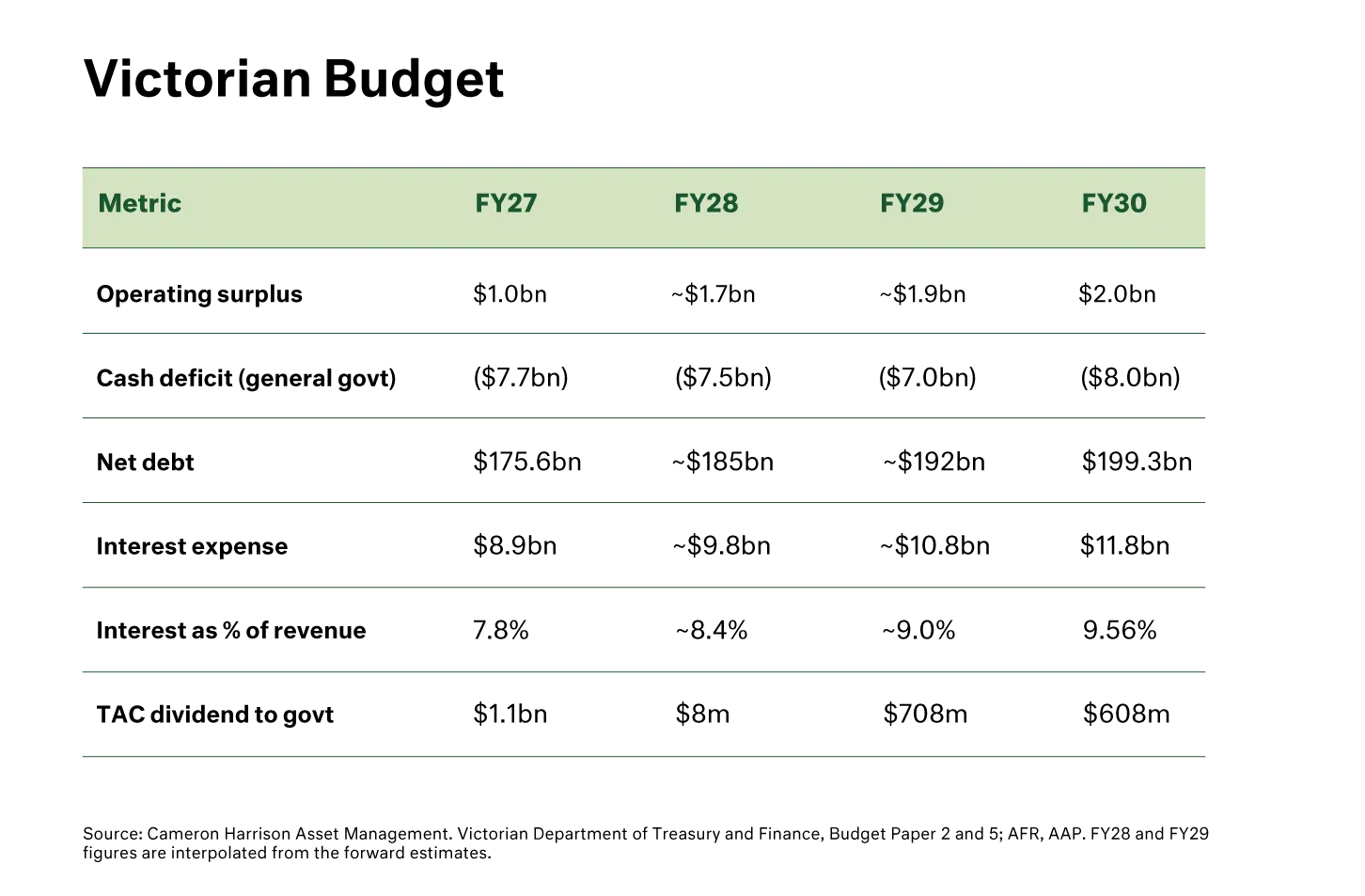

The Victorian Budget 2026/27 reports an operating surplus of $1 billion, but this is the headline number, not the cash position. Once debt-funded capital spending is included, Victoria is forecast to record more than $30 billion in cumulative cash deficits over the next four years, with net debt rising from $165 billion to $199.3 billion by mid-2030 and the annual interest bill climbing from $8.9 billion to $11.8 billion. The budget relies on a $1.1 billion dividend from the Transport Accident Commission (TAC) and optimistic growth forecasts to hold the surplus together. For investors, the implications are real: state-government credit risk, property tax burden, and inflation pressures all remain elevated.

We continue to favour shorter to medium-duration credit issued by quality issuers — the major banks, well-capitalised corporates that locked in low-cost debt, and selected government agency paper. Long-dated state-government debt is less attractive: the spread to Commonwealth bonds is not adequately compensating investors for prolonged structural deficits, and refinancing pressure across the states will remain a feature for some years.