They say never make the same mistake twice – Labor’s main learning from the 2019 election failure appears to be it’s better to ask for forgiveness than permission. In this year’s Federal Budget, the Treasurer has recycled the key policies from the Shorten years (ex. Franking Credits) and ignited the fuse on generational warfare. It is a calculated political gamble from a government that is banking on appealing to a growing cohort of disillusioned younger voters and hoping that the rest of the electorate will not have long memories come the next federal election, which is not until 2028.

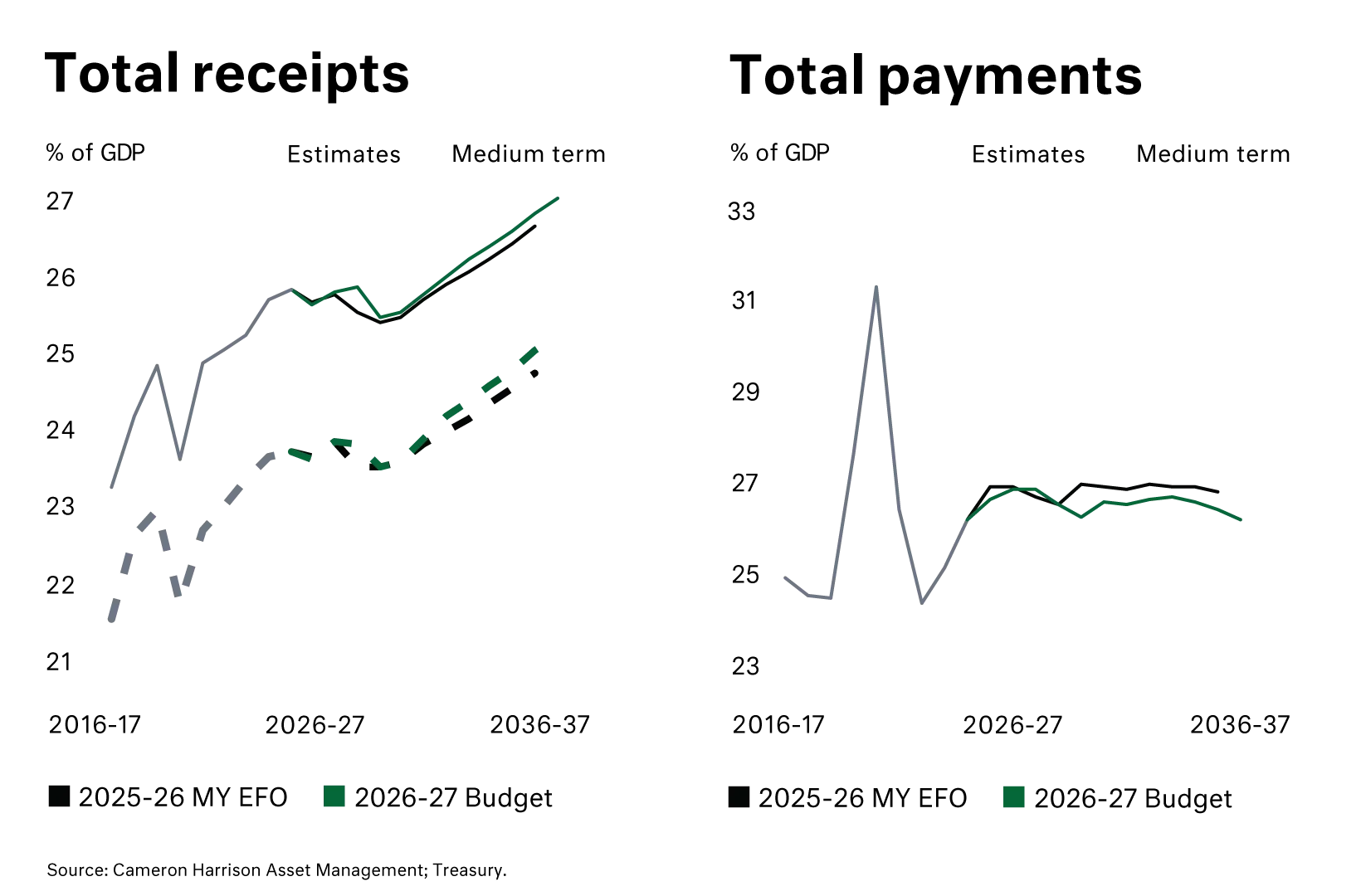

A surplus is not forecast until 2035. Without another commodity windfall, that looks unlikely, with the government more likely to focus on keeping debt-to-GDP stable rather than paying debt down.