For a while, the answer looked like yes. The slow and steady approach seemed to be delivering. But recent data releases have shifted the picture. Several indicators now point to a re-acceleration in inflation at the same time employment markets are tightening again.

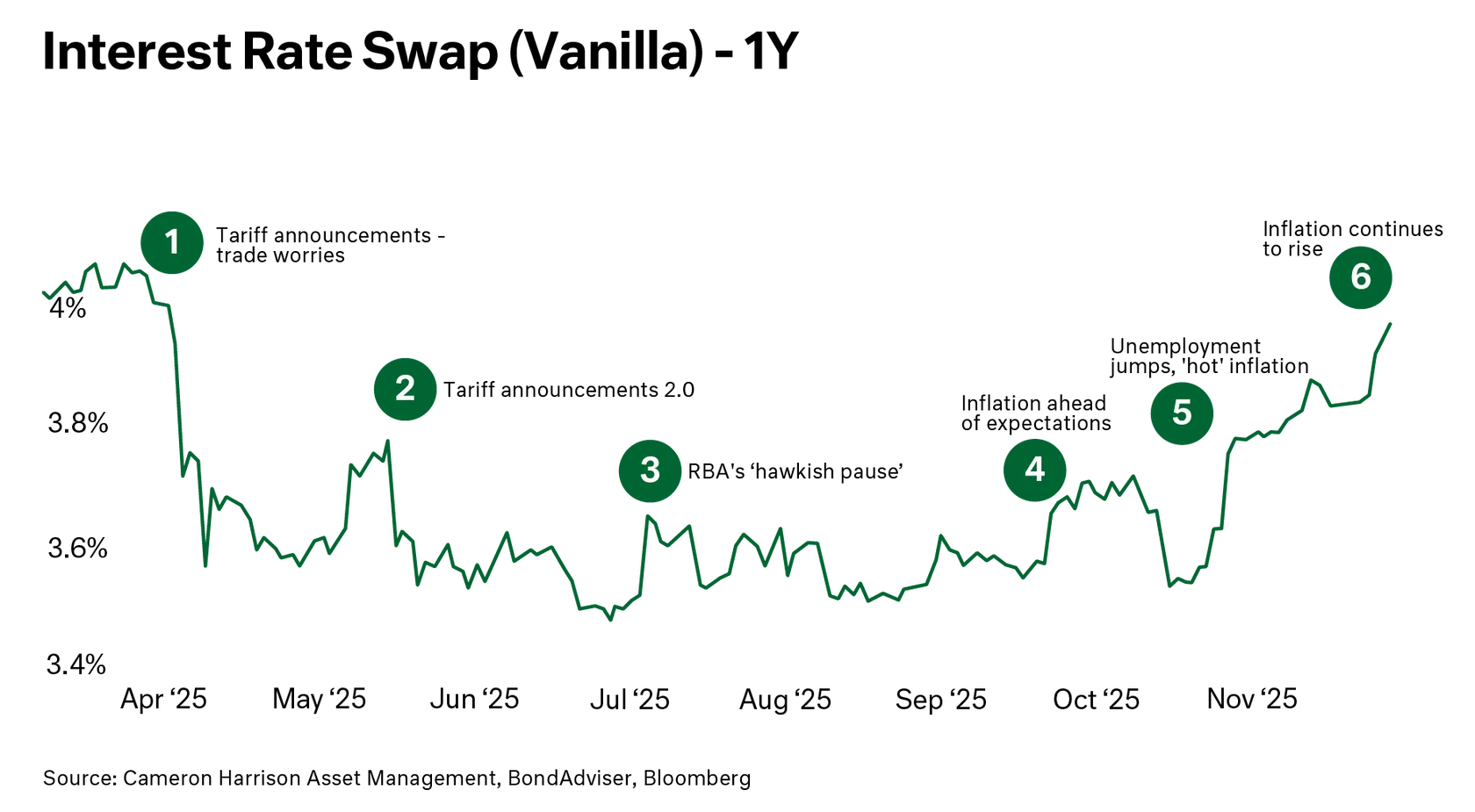

Through 2025, rate cut expectations oscillated; rate markets have reacted sharply to every data point. In April, markets priced in rate cuts to below 3% as Trump tweeted his way to tariff ‘victory’ and expectations of a global trade downturn emerged. In subsequent months, these fears abated, and local rate markets refocused on local data points.

By the end the year, the narrative had shifted away from rate cuts to the possibility of rate hikes in 2026. A flurry of inflation, labour market and housing data emerged in October and November, all pointing to an environment in which the supply side of the economy remains constrained. The consensus now is that the RBA’s next move will be up, not down.