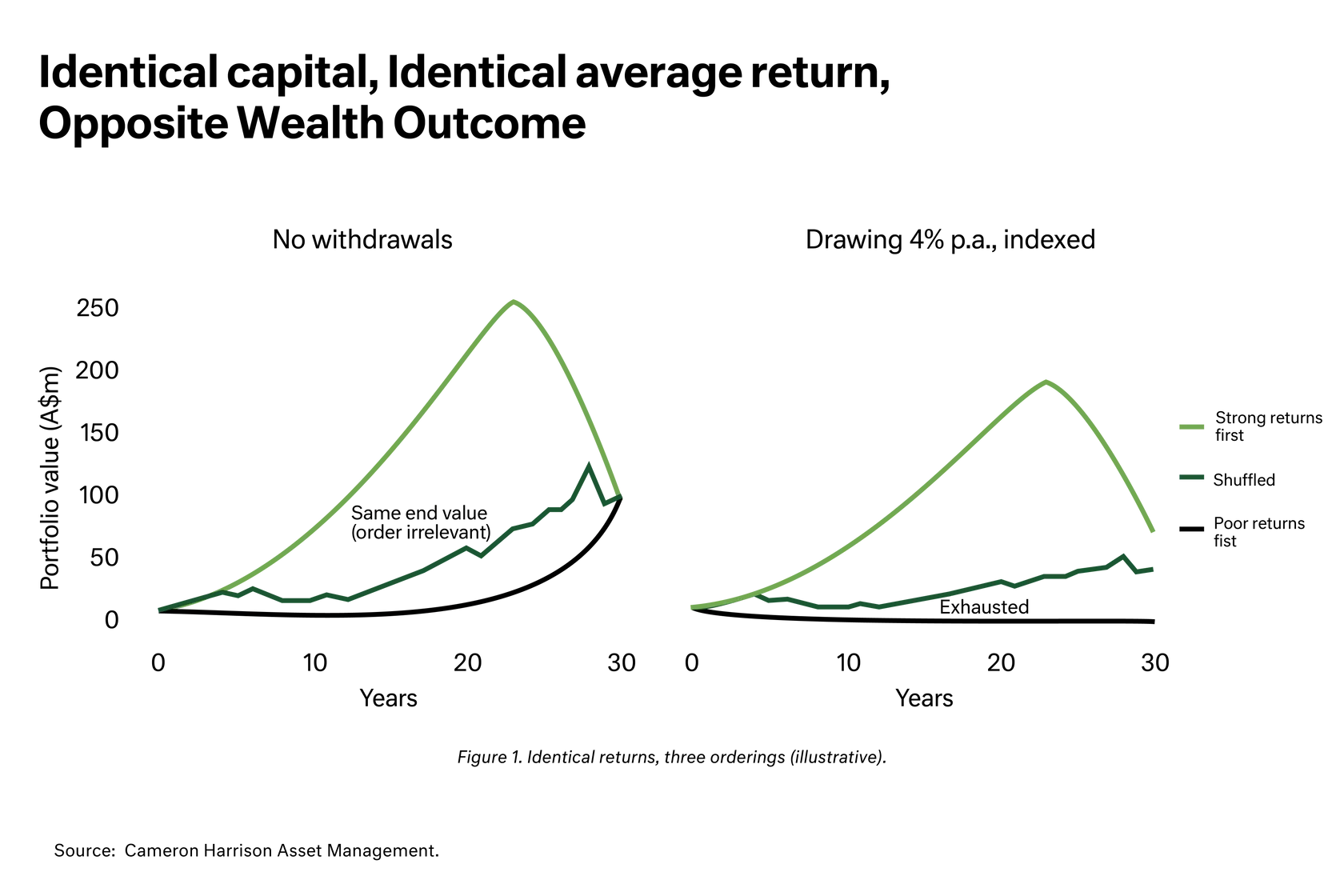

Average returns are not what determine outcomes – sequencing is.

Two families with identical wealth, spending, and long-run average returns can experience entirely different outcomes depending on when returns occur. Once withdrawals begin, early negative returns can permanently impair capital, as assets sold to fund spending cannot participate in future recovery.The critical question is how much risk, not what to own.

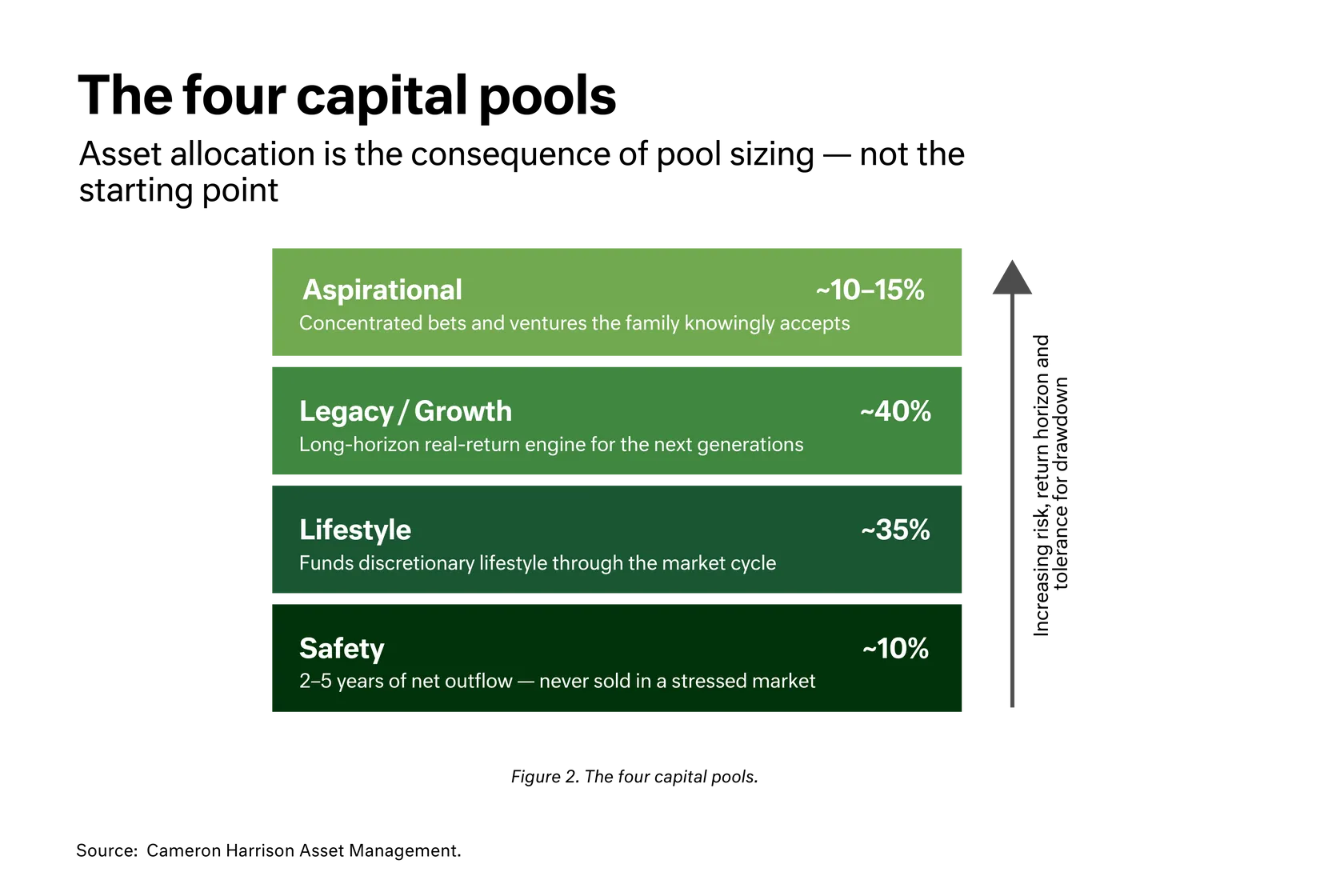

Investment outcomes are driven more by the sizing of risk relative to a family’s spending, obligations and tolerance for loss than by asset selection. Poor risk sizing, particularly in the presence of withdrawals, is the mechanism through which sequencing risk turns volatility into permanent loss of capital.Significant wealth amplifies, rather than reduces, sequencing risk.

Larger and more structured outflows, longer time horizons, illiquid assets, concentration, and governance pressures increase exposure to poor return sequences. For Australian families in particular, tax settings and drawdown rules further intensify the impact, making sequencing risk a central, and often under-managed, threat to long-term wealth.

It is the risk that the order of returns, not their long-run average, determines a portfolio’s outcome once a family is drawing income. A poor run early in drawdown causes damage later recoveries cannot fully undo, because the assets sold to fund spending no longer share in the rebound.