Most people view things in the context of today; their wealth, spending requirements, according to what they see and understand today. In determining spending, there can be a bias for a fixed dollar amount per annum and often then an inflation adjustment. There are other factors to incorporate, such as risk preference, utility preference, life expectancy and importantly, variability in returns. Here we explore how investees can approach this question with confidence.

Messrs Haghani and White1 have recently considered and analysed this subject (amongst an array of others) in their seminal book “The Missing Billionaires – A Guide to Better Financial Decisions”. In simple terms, they demonstrate through proper analysis that ignoring investment returns from year to year (together with your risk and utility preference) and drawing fixed annual spending sums potentially puts you on the road to wealth oblivion. Ignoring your portfolio performance from year to year and with it your individual preferences, is likely a recipe to prematurely exhaust your retirement pool. This need not be the case.

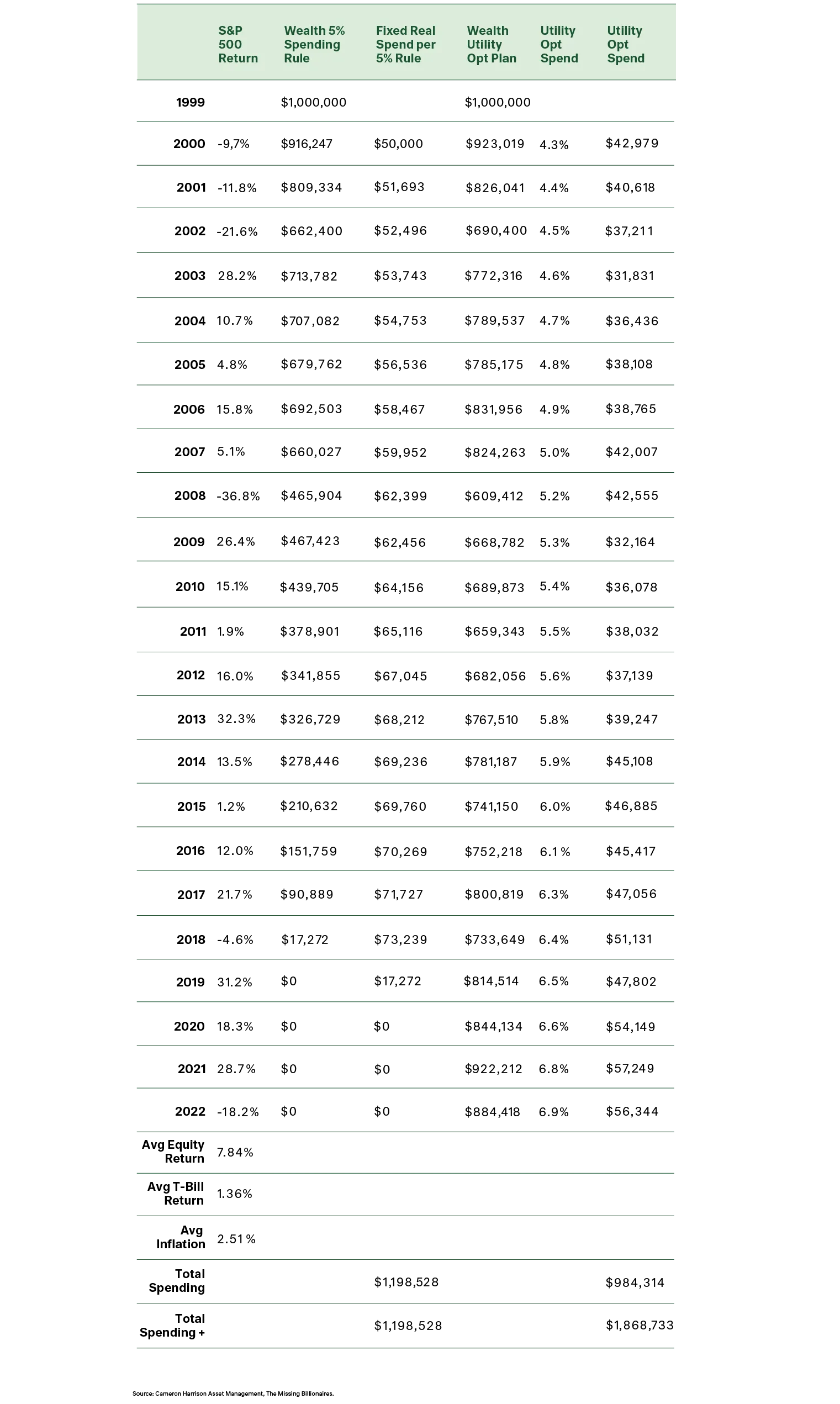

For example, lets say you had a 60% exposure to market risk equities (expected return = 9% pa) and 40% exposure to short term government debt (expected return = 4% pa). Your time horizon is 20 years and your average tax rate is 20% with a moderate risk tolerance. Based on different approaches to spending, the outcomes would be:

Spend fixed 5% per annum adjusted for inflation: this would likely see capital exhausted at the end of 19 years.

Set spending each year by reference to the value of your portfolio based on risk and utility preference: this would see surplus capital and confidence that your capital wouldn’t be exhausted, whilst ensuring your spending would match your risk appetite.

We can see this tabled below.