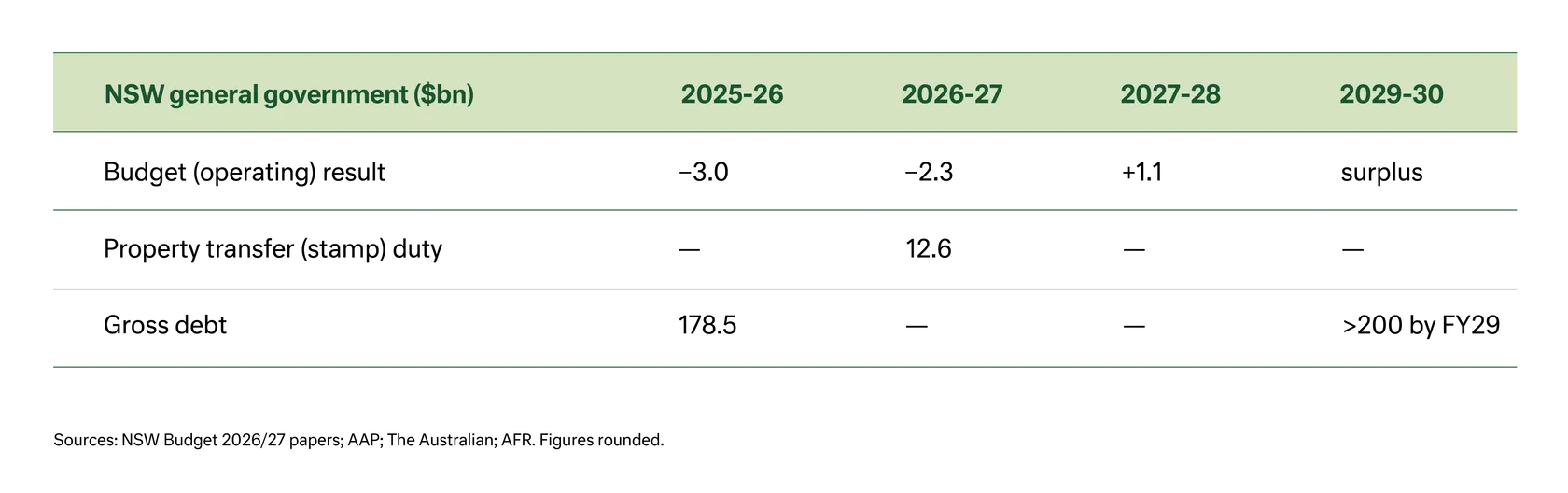

The NSW Budget 2026/27, handed down on Tuesday by Treasurer Daniel Mookhey, is the most fiscally disciplined of the mainland states: over three years NSW has held average expense growth to 3.6 per cent a year, less than half the 8.3 per cent average of the other eight governments. But discipline is not a surplus. Deficits of about $3 billion (2025-26) and $2.3 billion (2026-27) precede the first surplus, a forecast $1.1 billion in 2027-28, beyond the March 2027 election, while net debt climbs toward $196.9 billion by mid-2030. NSW is the better managed balance sheet in the federation, but the result is restraint deferred rather than repair delivered.

Against our analysis of the Victorian Budget 2026, the contrast is striking. Where Victoria leaned on a dividend from its motor accident insurer to underwrite a token surplus, NSW has done the harder work on spending, and Barrenjoey rates it “best placed” among the states to deliver. We do not want to diminish that. But three things temper the picture: the deficit persists, the surplus sits beyond an election, and the budget still reaches for the same lever we flagged in our Victorian Budget analysis - a billion dollar plus uplift in dividends from a state investment fund.

The discipline is real; the surplus is deferred.