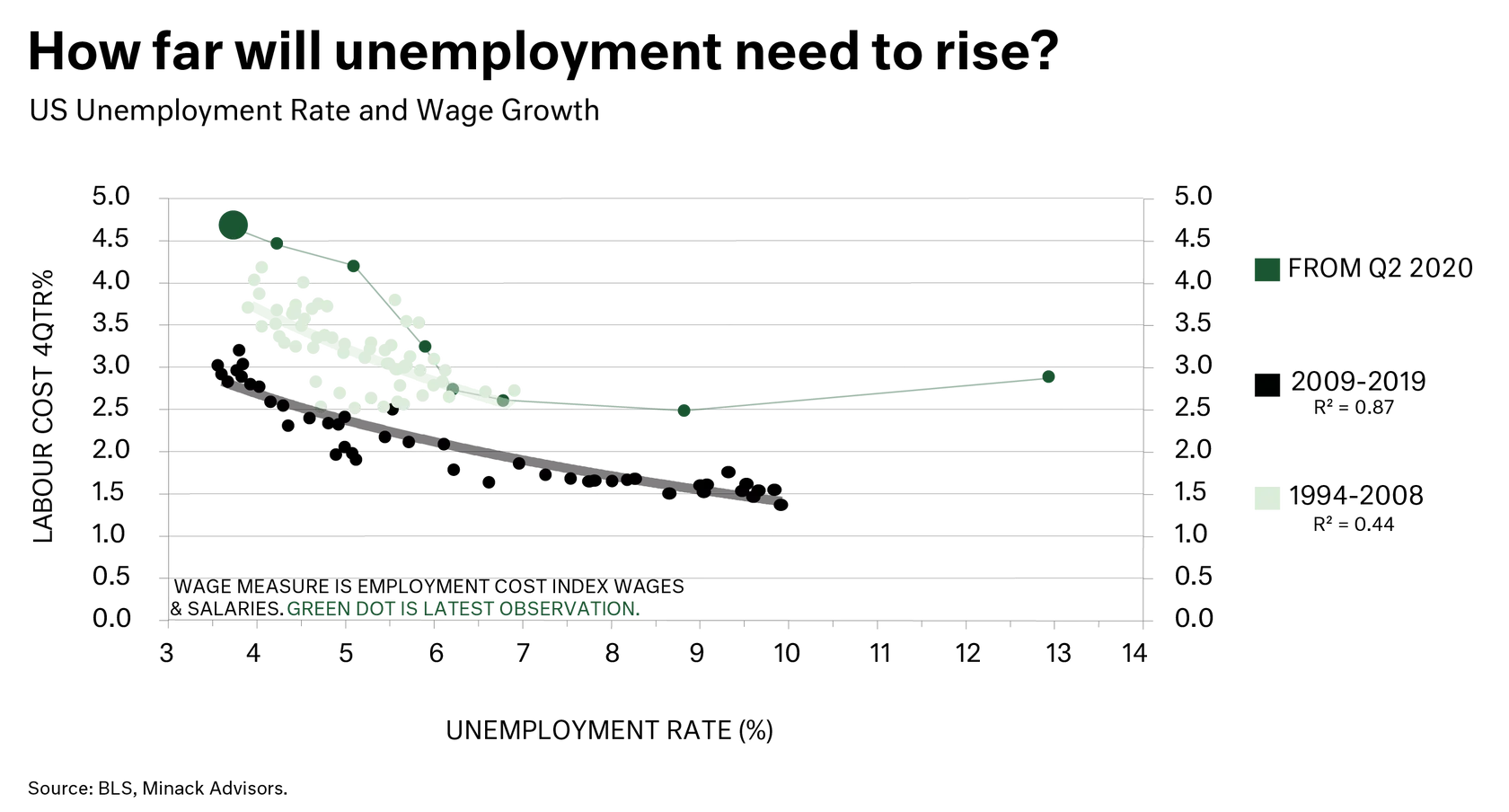

To deal and manage inflation expectations, wages growth needs to moderate from current elevated levels. For that to occur, unemployment levels will need to rise. This is predicated on a current stable participation rate of 62.3%, where pre COVID it had been over 63%. This is likely a reasonable assumption, though the key swing segment of over 55 year old's may start to return to some gainful employment (though the evidence suggests this is not occurring, but recent losses on wealth may see over 55's come back into employment). The recent observations in the green line with the green dot being now, indicate that to get back to 3.5% wages growth, the US will need unemployment at least 1% higher. Putting aside an increase in the participation rate, this leaves slowing the economy and increasing unemployment. Historical precedence says to achieve such an outcome would require a recession. The Volker shock.

As inflation invariably moderates through 2H2022, the residual risk of inflationary expectations is what needs to be curtailed. In Australia, we are less sure that the RBA’s mooted neutral cash rate of 2.5% is in fact correct, and it is in fact lower. At a 2.5% cash rate, a 25% to 30% fall in peak property prices would be catastrophic, and we think on balance, such a level of interest rate is more unlikely than not. Notwithstanding, the next few months will be hugely volatile for bond and equity markets as the blunt Volcker-like monetary policy measures are implemented. The lag effects of reduced economic activity will bite in 1H2023 and we think bond market yields will be forced lower and cash rates in late 2023 will need to be reduced.

Such movements are extreme but not unusual, but are disconcerting in the short run. Listed equity markets and bond markets are highly liquid and therefore reflect the short-term emotions and peculiarities of participants. For example, equity markets have been awoken to inflation and inflation expectations. Money markets and bond markets have been more a tuned to these risks, whereas equity markets operate with both over optimism and pessimism, and we are seeing this play out. All investment categories are adversely impacted, whether listed or unlisted. Listed markets just happen to be a liquid, live theatre where liquidity provides exits to ill-prepared and we assess, over leveraged investors. This is what exaggerates short-term movements, and needs to be looked through to first hold and then, in turn, rebalance upwards into the portfolio's high quality investments that are marked down due to this short term exaggeration (though whose fundamental causes we agree with and reflect in our strategy positions). Over the medium to long term, wealth transfers from the impatient to the patient. For over 35 years of managing our strategies, we are certainly the patient, but will assess risk and opportunity on its merits.