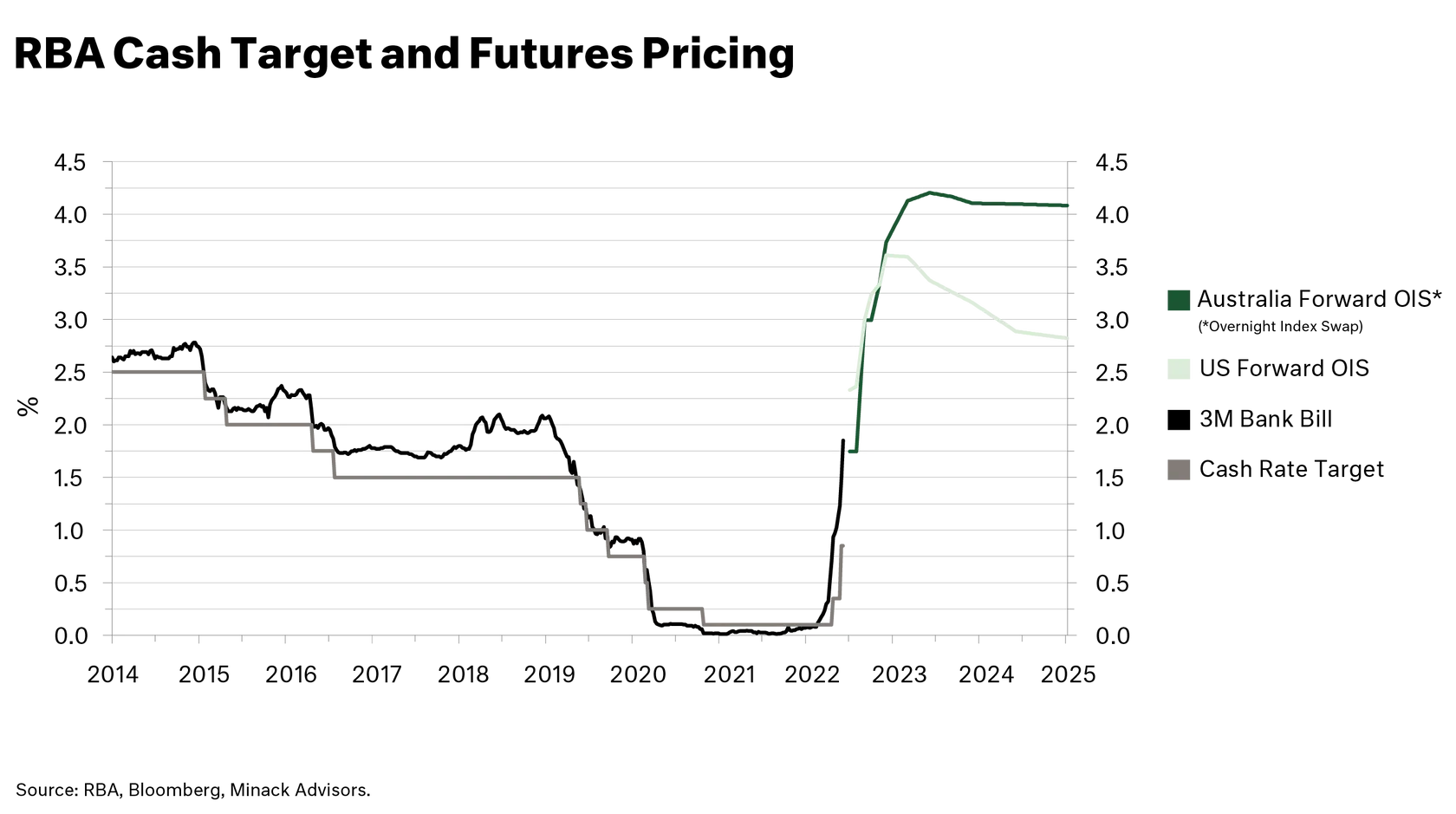

After keeping rates too low through the second half of 2021, Central Bankers have rapidly shifted into full-Volcker mode and can hardly be accused of not taking the inflation risk seriously.

In contrast to the 1970s, wage growth has been artificially accelerated (see factor below) and will slow as it returns to normal operation. Leading indicators of the labour market, such as the difficulty in filling jobs and the job quit rates, recently started to inflect.

Developed economies have experienced a supply shock. The restriction on the movement of people (immigration) resulted in the supply of cheaper labour drying up but this will rectify itself as borders reopen.

Job movement is elevated after being suppressed by the pandemic; higher switching of jobs is correlated to higher wage growth (why move unless you will get paid more?).

Many older workers failed to return to the labour market in 2021; given older employees typically have slower wage growth, this further elevated wage growth. Recent data suggests the unretirement rate has shifted from a pre-pandemic rate of 1.0-1.5% to over 2% as rising wages, high inflation and lower asset prices drive over 55s back to work.

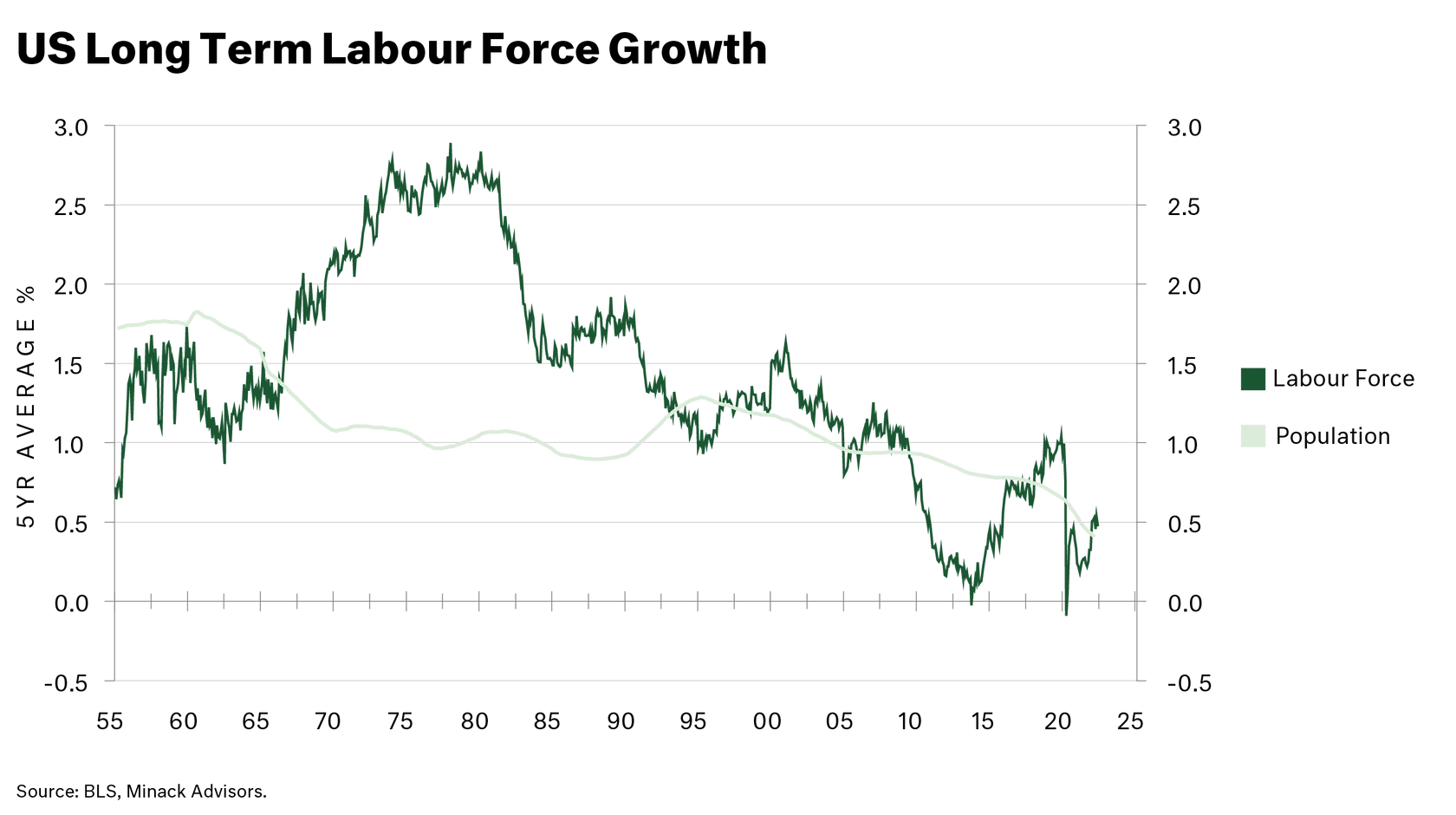

Finally, and potentially most importantly, the demographic-driven inflationary forces that drove the labour force growth rate above 2.5% per annum have gone. The forecast for the coming decade is a measly 0.5% p.a. - a disinflationary force rather than inflationary.

The chart following shows long-term US labour force growth against the total population and working-age population.