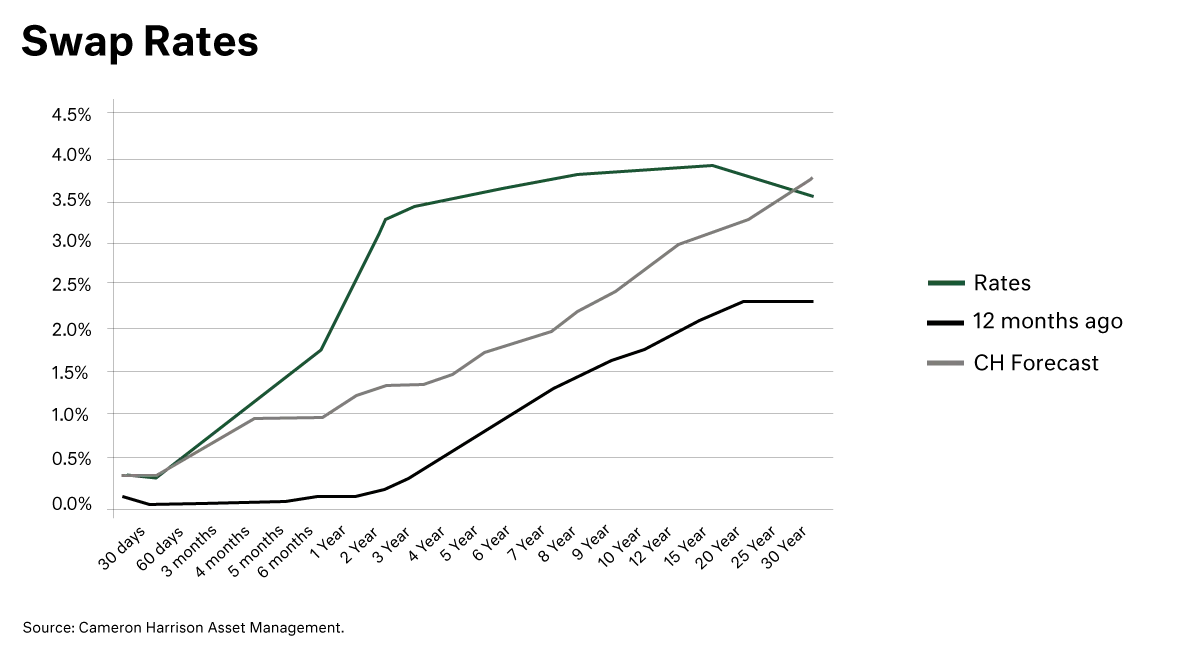

The scale of the inflation overshoot and central bank policy undershoot has provided ‘kerosene’ to valuation correction across all asset classes. Bond markets in particular have acted aggressively on the forward curve to mark up their yield expectations very rapidly. If this forward curve becomes a reality, then indeed it will continue to be brutal for valuations, with a ‘take no prisoners’ result for all asset classes.

Markets have reactively swung aggressively to the very worst. Now is a good time to pause and work through the paths ahead and their probability.

Watch the interview and read the summary, below: