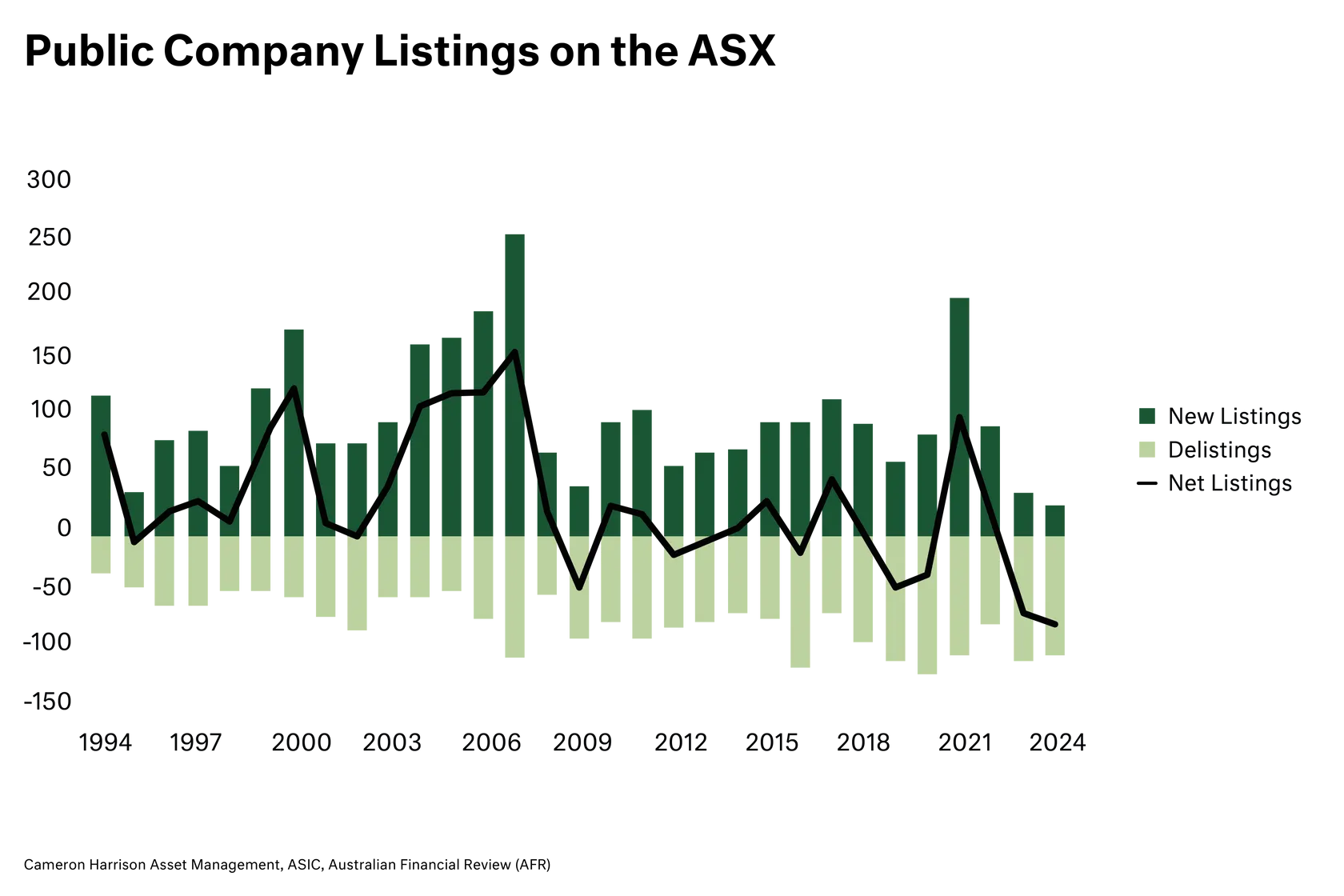

On one hand, maybe not. Newly listed companies (IPOs) have long been shown to underperform comparable, well-established companies in their first three years on the market (the ‘pain period’) after their first trading day. Exceptions are possible; Guzman y Gomez continues to defy rationale valuation metrics, however the weight of evidence points to poor outcomes, with an average underperformance of ~17% over the first three years (Ritter, 1991).

On the other hand, it does. As we noted in our recent article, the composition of the ASX has hardly changed in the past 30+ years. Without companies listing in the market and benefiting from the transparency and scrutiny that comes with an IPO, the public market will continue to stagnate, and Australians will be worse off for it.

Given the mixed history of IPOs, Cameron Harrison avoids fresh listings in its equity strategies. Instead, we prefer to closely watch new companies of interest, and then look to invest after the initial ‘pain period’ of three years – once insiders have exited and management have built the required systems/structures needed as a public company. A recent example is Lovisa Holdings, which was added to our portfolio after meeting our Business Success Framework. Lovisa is an outstanding business that has demonstrated reliable earnings and scalable growth alongside cost-effective management.

Ultimately, indications of an uptick in IPO activity are a good sign for investors and the long-term health of the ASX. We continue to monitor current and new listings (where they exist) but, as always, IPOs are a case of buyer beware.