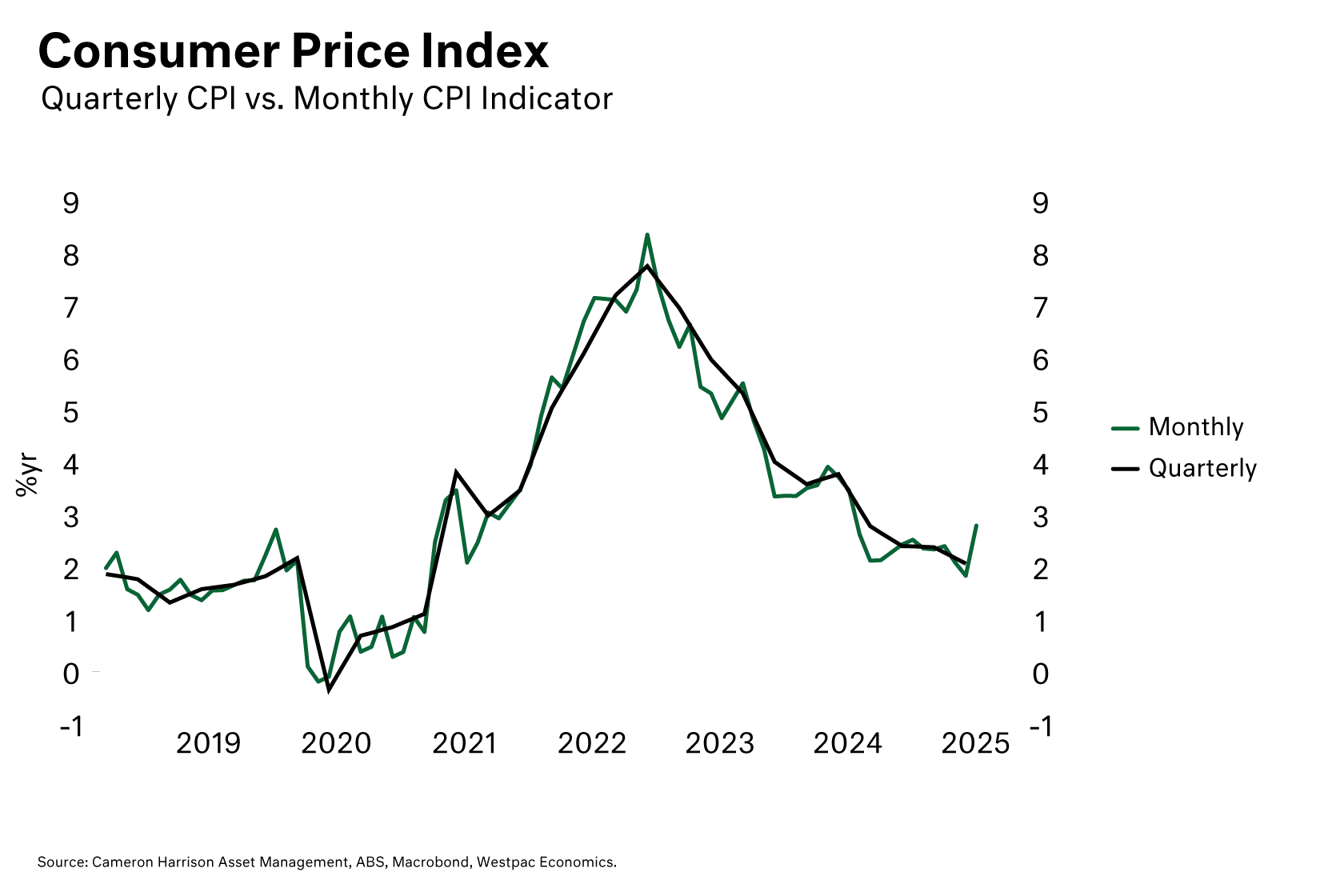

Australia’s July Monthly Consumer Price Index (CPI) came in stronger than expected, rising 2.8% year-on-year – well above the market’s expectations of 2.3%. The market was expecting higher inflation than the 1.9% print in June due to the expiration of the electricity rebates but underestimated the impact.

It wasn’t just electricity as the culprit - the underlying measures of inflation also accelerated. Even excluding volatile items such as fuel, fresh food and holiday travel, inflation jumped to 3.2%, the fastest pace in more than a year. This suggests that price pressures are not only higher than expected, but also more broad-based.