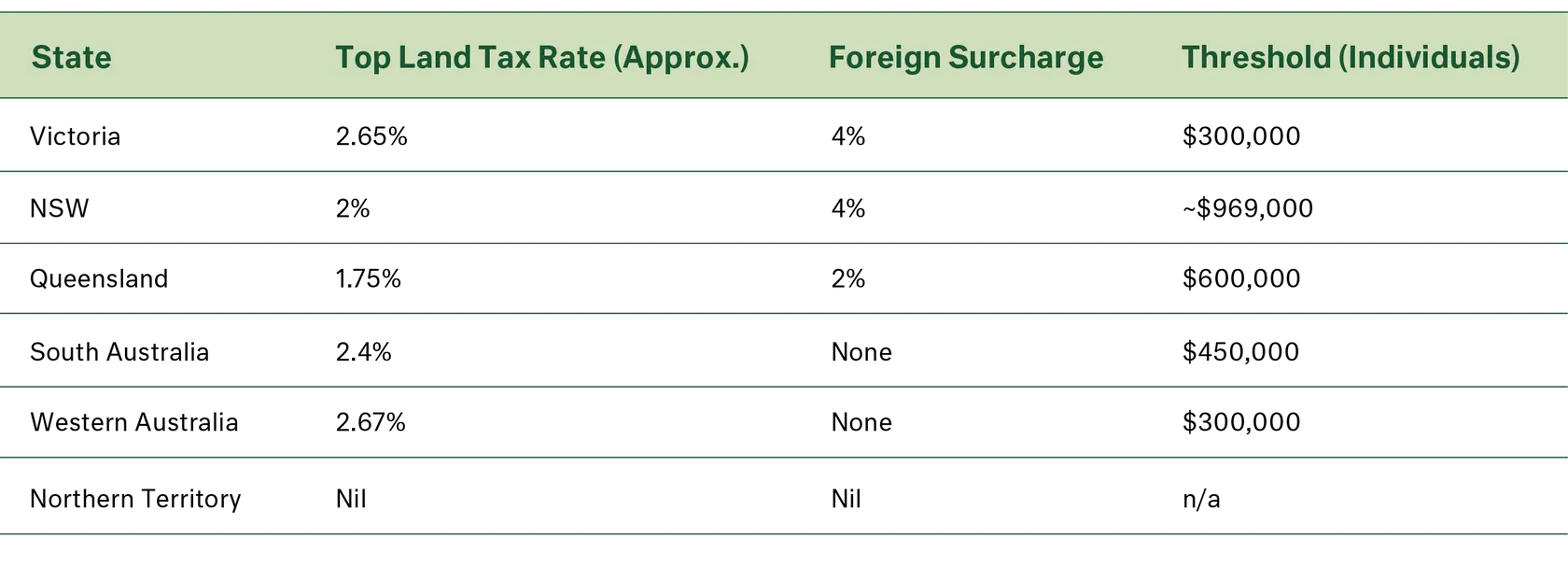

In principle, state taxation of property is entirely reasonable. Land is immobile, difficult to offshore and benefits directly from public infrastructure. Property taxes can therefore provide a stable and equitable revenue base for state governments. The issue is not the existence of these taxes, but their increasing scale and breadth, cumulative burden and constant evolution.

Across Australia, property has become the tax base of first and last resort. Stamp duties, land taxes, foreign purchaser surcharges, rezoning levies and infrastructure charges are not only growing in quantum, but changing frequently. This creates a moving minefield for investors - one that does little to support the patient capital required to address Australia’s housing shortage.