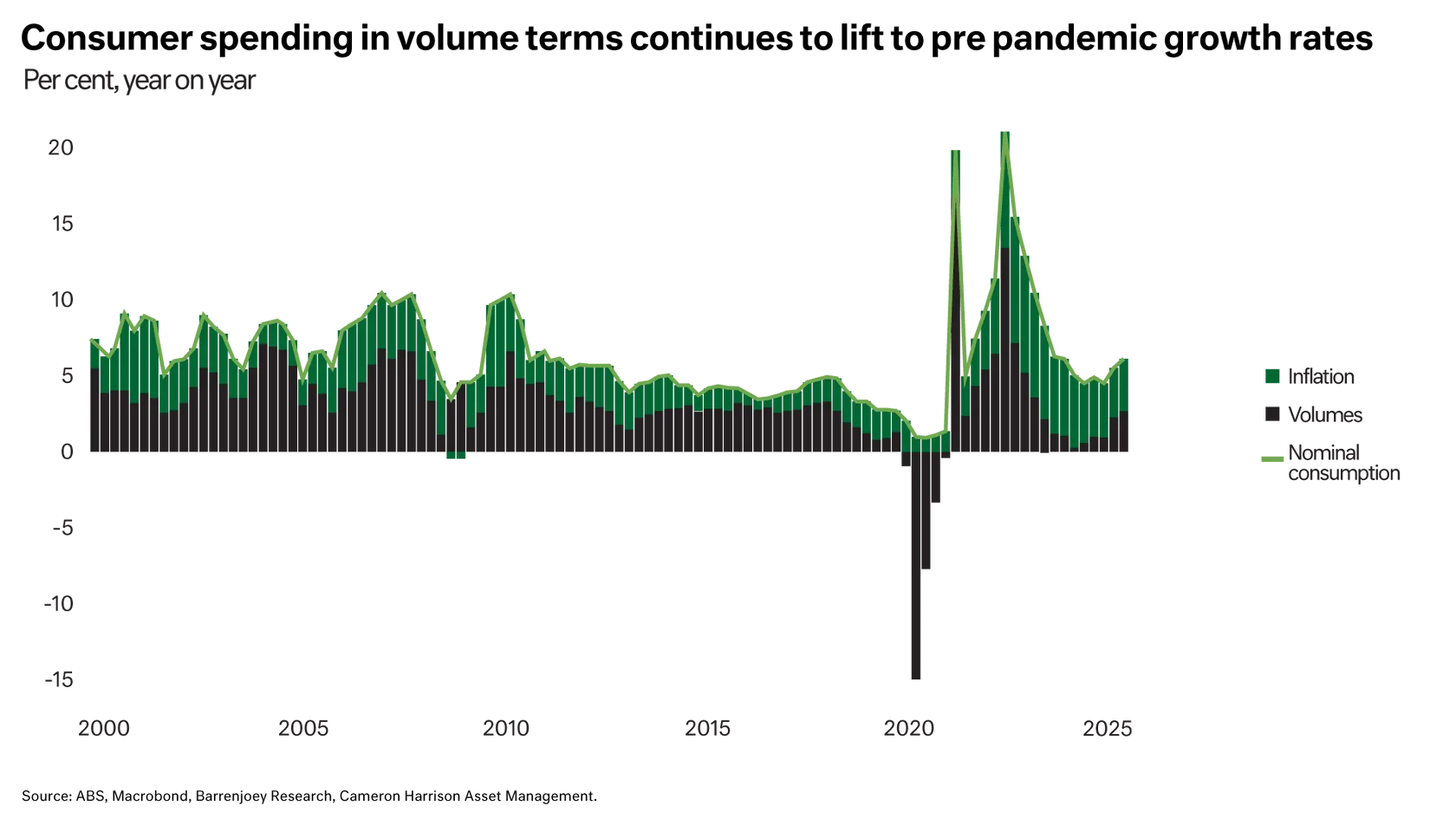

The consumer led the way in 2025. Three rate cuts from the RBA alleviated pressures, and solid wage growth saw rising disposable incomes (albeit from a low base) which boosted consumer confidence. These factors alongside a positive housing market (that added the wealth effect into the mix) resulted in a happier consumer. This saw the consumer spending volumes return after a period where real consumer spending (after inflation) has been declining. It was the first time in years consumers were buying more – not just paying more for the same level of goods.

Australian Equities: Riding on the Consumer’s Back

Investment Solutions

2025 was a mixed year in Australia. The ASX200 delivered 10.3% despite moments of elevated volatility in April and November. On a macro level, there are signs of green shoots and an uptick in growth but off a very low base. In the post-COVID years it has been an economy reliant on government spending with the public purse propping up growth. In fact, without the spending of government in 2024 Australia would’ve been in recession as the private economy faltered. The good news is in 2025 GDP growth accelerated on the back of the private sector returning to life.

Posted 27 January 2026

The back half of 2025 provided cause for optimism that looks increasingly likely to dissipate in 2026. The increase in consumer spending (particularly the spending on services) has the RBA on high alert due to the spike in inflation. Expectations of further rate cuts quickly evaporated which is likely to dampen both the housing market and consumer optimism. It looks unlikely inflation can moderate without some pullback from the consumer, especially as employment markets remain tight and wage growth resilient.

Government spending is also under pressure – softer commodity prices have taken away the ‘free win’ in budget settings. The Government is closely reviewing how it can improve its declining budget position via extra taxation and/or tightening of spending on the NDIS alongside the removal of energy bill rebates.

The game plan for Australia looks much the same, which in our view is not a recipe for success at the headline level. Immigration is likely to remain above trend, but unmatched investment will continue to pressure living standards and per-capita growth.

Labour productivity is falling and will continue to come under pressure with above average growth in the size of the public sector. The implication is that real wages cannot rise without creating inflation pressures, as seen in the recent CPI data, creating an air of macro stagnation.

The end of rate cuts and a potential rise could dampen the consumer’s optimism and flow through to limiting the growth of corporate earnings.

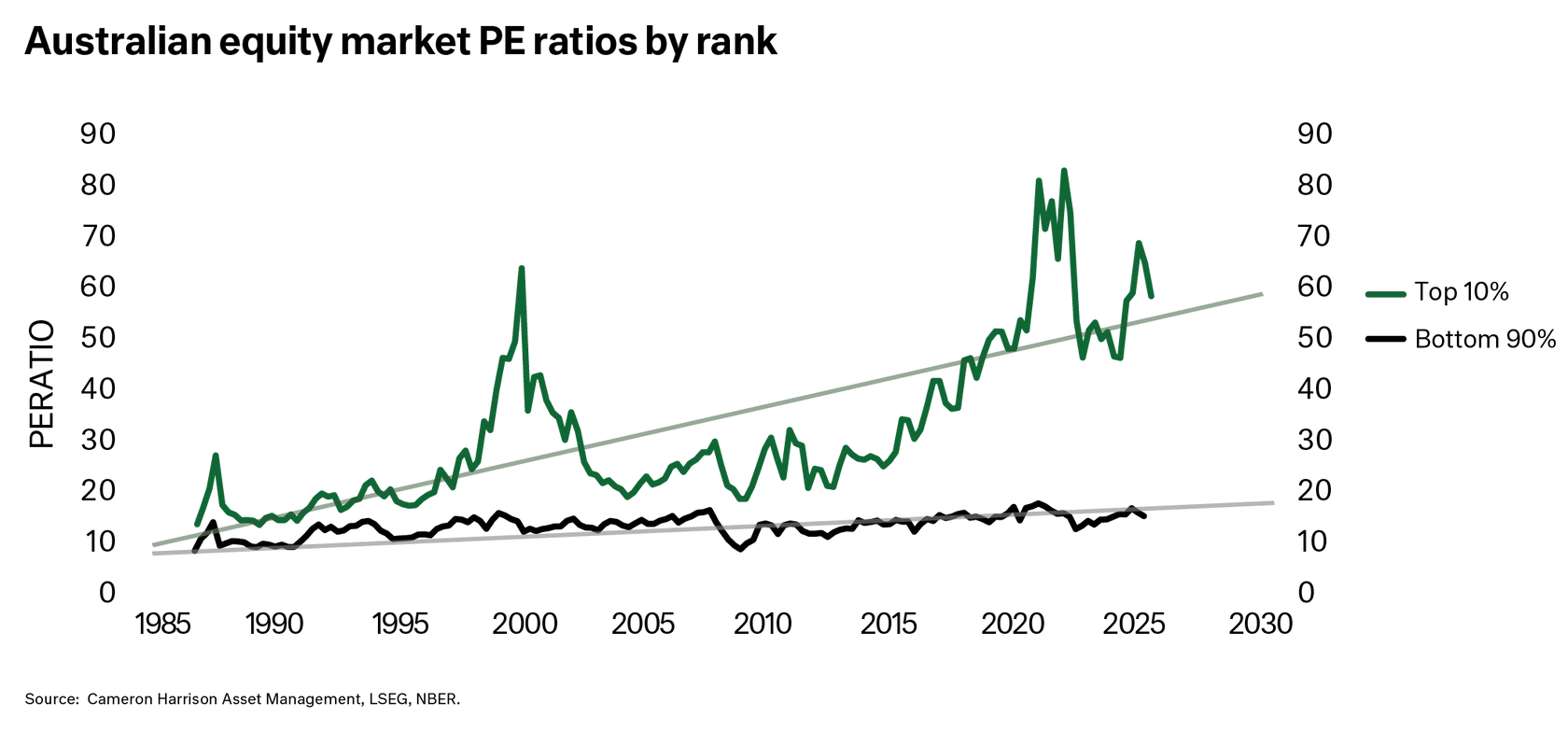

The ASX is now trading on a forecast PE ratio of over 20x, nearly 30% above the average valuation since the turn of the century. Yet the forecast earnings growth over 2026 is just 5%, less than half the developed market average.

The rise in valuations has been relatively narrow, with the most expensive 10% of the market becoming more and more expensive (see chart above), to levels rivalling valuations prior to the dotcom bubble, and the 2022 inflation selloff.

This concentration and crowding in expensive investments is symptomatic of a market dominated by flows of passive investment and benchmark hugging superannuation funds, driving buying against the backdrop of average fundamentals. As previous examples have shown in 2000 and 2022, should economic data disappoint these companies will be hardest hit.

We see an increasing environment that will reward disciplined investors who are able to spot the ‘rose among the thorns’ of the other 90% of the market. Valuations can stray for periods but the recipe for long-term success remains the same, buying quality businesses at fair prices and allowing them time to prosper.

Watch Will's video below:

Speak to one of our advisers to learn more:

william.fisher@cameronharrison.com.au

Sourced from:

Photo by iStock