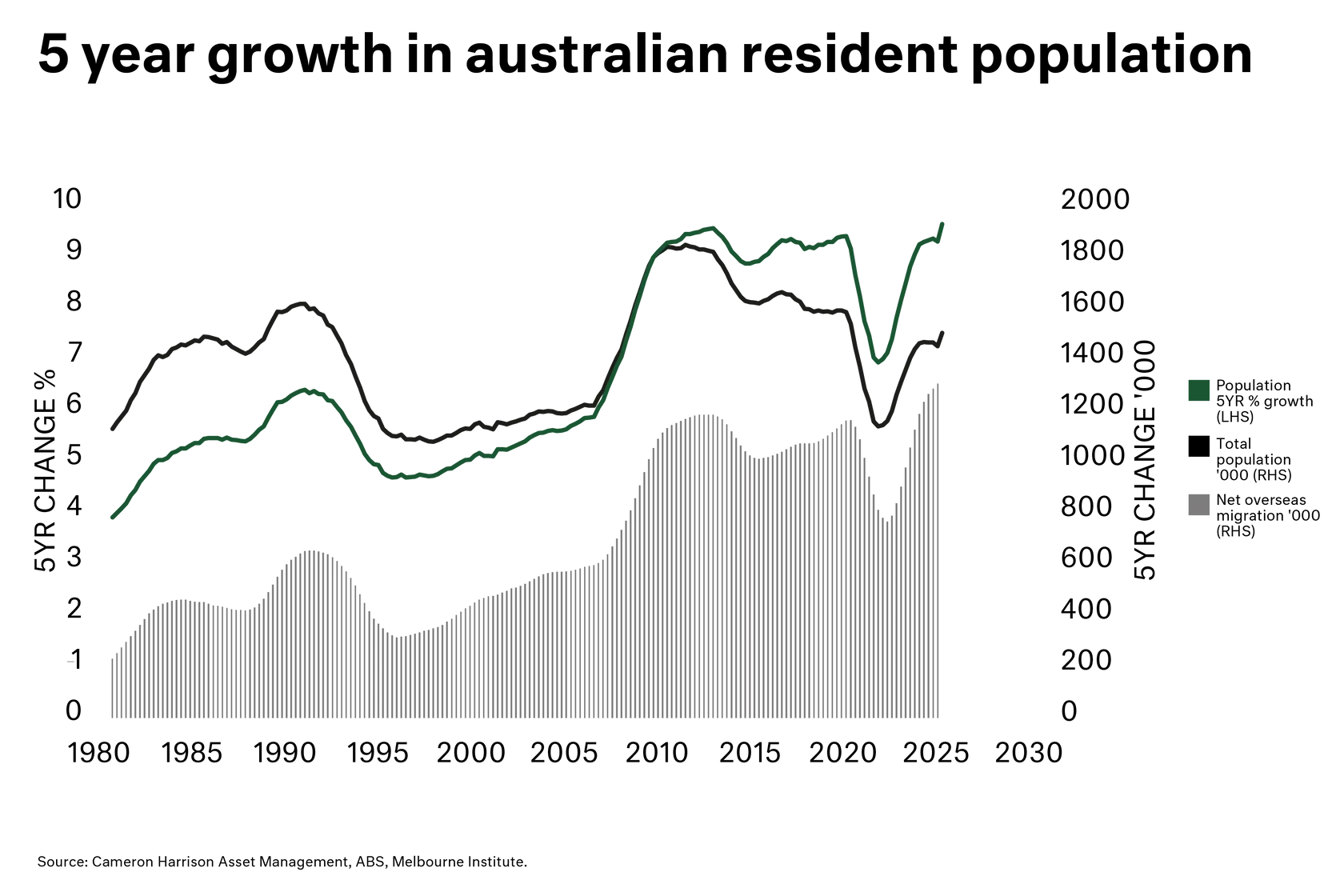

The macroeconomic backdrop for FY26 looks increasingly supportive: interest rates have begun to ease, bond yields are trending lower, and population growth continues to underpin occupier demand. These factors, combined with inflation-linked leases, result in income growth to drive valuations higher for industrial and retail property. As rents rise and capitalisation rates stabilise it appears the bottom of the valuation cycle is behind us.

Within this environment, we expect industrial, logistics, and essential-services property to deliver the most resilient, inflation-protected cash flows and outperform through the cycle. Data centres, while structurally attractive, remain priced for perfection and carry execution risk. Offices and retail will improve selectively, prime CBD assets and essential retail formats should stabilise – but structural challenges persist. Our positioning reflects this conviction: overweight industrial and healthcare, underweight office and discretionary retail, aligned with a house view that favours scarcity-driven sectors with strong fundamentals.