More than ever, parents are “chipping” in to help their children; this can be a significant amount to help buy a property, ongoing help for supplementing income or paying expenses such as school fees. What is colloquially known as "the bank of mum and dad" represents not merely an act of generosity but also a consequence of changing economic realities, shifting wealth dynamics, and most importantly, a need for strategic wealth planning.

No Branch Closures in Sight for the Bank of Mum and Dad

Market Insights |

Wealth Management Solutions

Intergenerational wealth transfer is not a new concept. It was traditionally used to describe the passing on of assets from one generation to the next in the form of inheritance. However, the modern-day definition is far broader, encapsulating wealth owners who wish (or feel compelled) to provide financial assistance to their children throughout their lifetime.

Posted 24 February 2025

For many parents, particularly Baby Boomers, the question is not whether to assist their children financially, but when and how. The traditional model of wealth transfer through inheritance upon death is being challenged by a preference for giving during one’s lifetime. This approach allows parents to witness the benefits of their support, helping children onto the property ladder, funding milestone events, or alleviating cost of living stress. In some cases, it may also be a tax-efficient strategy. For example, early wealth transfers can mitigate superannuation death benefits tax, thereby enhancing the after-tax legacy.

However, giving during your lifetime, is not without its pitfalls. Transferring part of your wealth to a child may expose the capital to risks it was otherwise not be exposed to during your lifetime, such as domestic relationship breakdowns, commercial liabilities and improper use of the capital. Furthermore, having capital bypass an estate (notably, testamentary trusts) may diminish longer-term tax efficiencies and asset protection. A bespoke, strategic approach is therefore essential, balancing the competing considerations of generosity, humility, security, and tax effectiveness.

Few trends illustrate the growing role of parental financial support more than housing affordability. Soaring property prices and an erosion of real wage growth have left many young people struggling to amass the necessary deposit to purchase a home, let alone cover transaction costs such as stamp duty. For those already on the ladder, no growth in real wages has added pressure to servicing debt. This is further exacerbated by higher interest rates, disproportionately affecting younger buyers with typically greater mortgage burdens while simultaneously benefiting unleveraged retirees through higher interest returns on their savings.

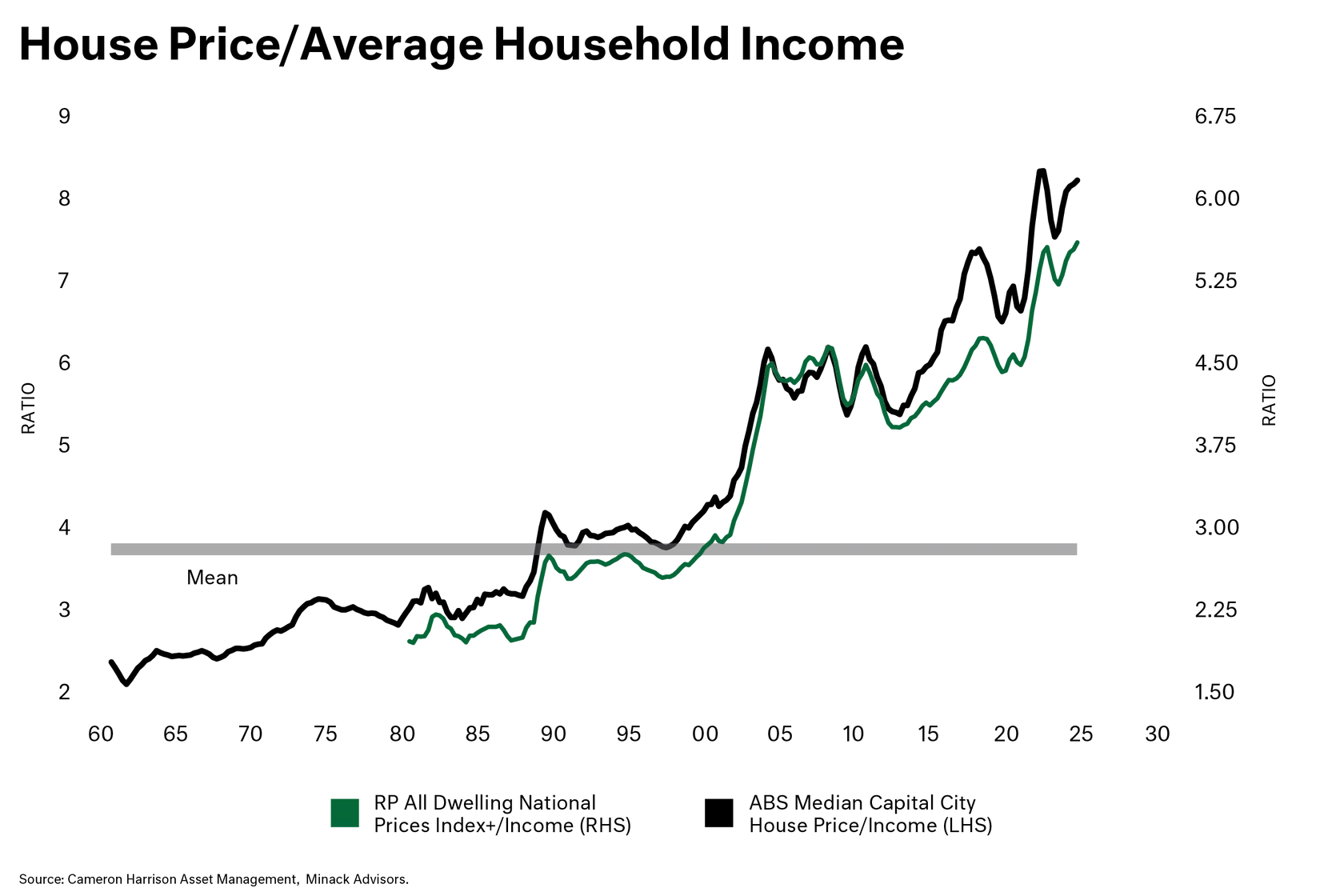

The below graph shows how house price increases (black line) have surpassed disposable income growth (green line), leading to an increase in housing unaffordability – particularly over the past 15 years.

Faced with these challenges, an increasing number of parents are volunteering or being asked to assist with home purchases. According to Australian Housing Monitor research, 40% of first home buyers receive support from their parents – an almost three-fold increase since the 80’s. While outright gifts are common, they are not always the optimal approach. Alternative forms such as secured loans, family trusts, or co-ownership arrangements can provide both the child and parent(s) with greater financial protection and/or flexibility.

The financial burden on younger generations is not limited to housing. Inflation has dramatically increased the cost of necessities and life events such as education and weddings. Independent school fees, for example, rose by 50% over the past decade to 2020 – more than double inflation (22%) and far exceeding wage growth (29%) over the same period. Witnessing their children buckle under this strain, parents are distributing some of their accumulated wealth and/or income to alleviate the pressure.

Yet, without proper financial modelling and long-term outcome assessments, parents risk jeopardising their own financial security. A well-intended act of generosity today may lead to unintended hardship tomorrow if it is not part of a sustainable financial strategy.

The financial reality that enables parents to provide support today may not persist indefinitely. Economic conditions fluctuate, and interest rates, investment returns, and inflation can shift dramatically (and quickly) over time. If parental giving becomes an expectation or even a dependency, turning off the tap can prove difficult – both financially and emotionally.

A disciplined, well-structured approach to intergenerational wealth transfer is therefore essential. The Partners at Cameron Harrison are well-versed in objectively assessing these delicate matters, even acting as counsellors at times to help parents reconcile the competing objectives of their own retirement security against the financial needs of their children. Moreover, our Plan for Peace of Mind process incorporates regular reviews and stress-testing of wealth plans, helping to guard against overcommitment and ensuring that generosity remains sustainable.

Cameron Harrison have been advising business owners and their families on asset allocation and intergenerational wealth management for over 50 years. We have demonstrated over a long period our ability to manage investments through both the good times and bad by keeping the client at the centre of our business.

For more information on our approach to wealth management or any other inquiries, please contact us on +61 3 9655 5000 or contact our experts here.

Speak to one of our advisers to learn more:

am.tassoni@cameronharrison.com.au

Sourced from:

Blueprint Institute Australia, Australian Housing Monitor, Minack Advisors;

Photo by Shutterstock