At its simplest, it is described as not having all your eggs in one basket. It is one of the only guaranteed ‘free lunches’ in investment. This is especially the case for an investor seeking long-term returns with well-defined risk and return characteristics. Cameron Harrison’s investment philosophy has embraced diversification benefits for over 30 years. For long term portfolio investors, it is indeed a “free lunch” to enhance risk-adjusted returns.

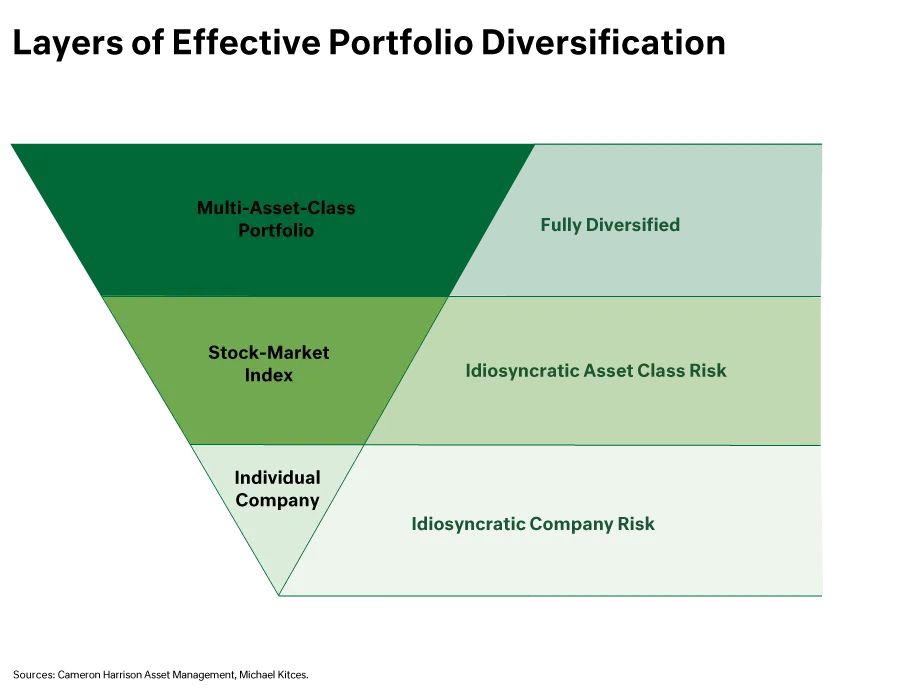

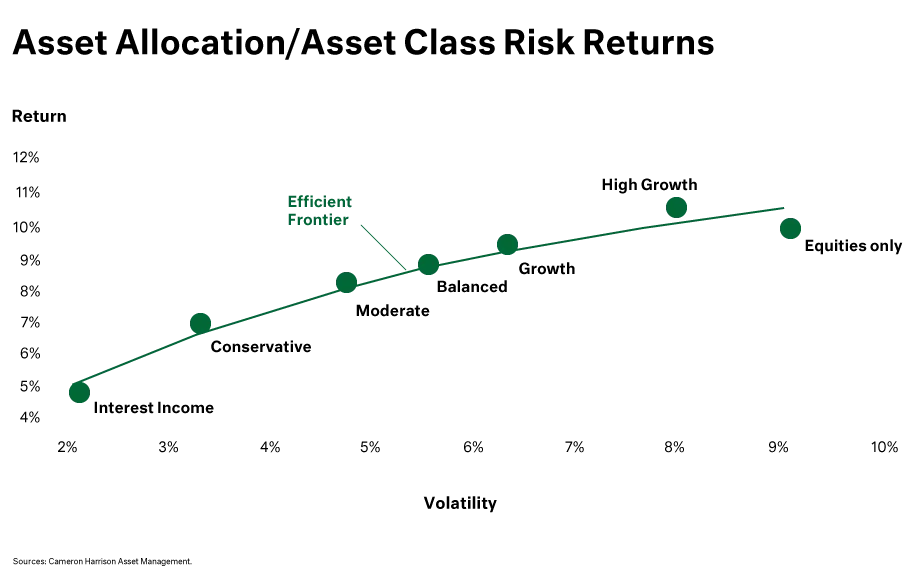

Diversification is about achieving optimum risk outcomes for given desired returns over time. Owning multiple shares spreads risk across multiple companies, achieving superior risk outcomes than holding a single company. Better again is investing in multiple securities across asset classes. The image below shows the layers to achieving diversification. The mathematical foundation for diversification in investing is rooted in Modern Portfolio Theory – one of the most significant financial studies – that proves an investor can achieve a more efficient, superior portfolio by combining assets. Importantly, the typical stock in the market has twice the volatility (risk) than a diversified portfolio, yet the same average return.