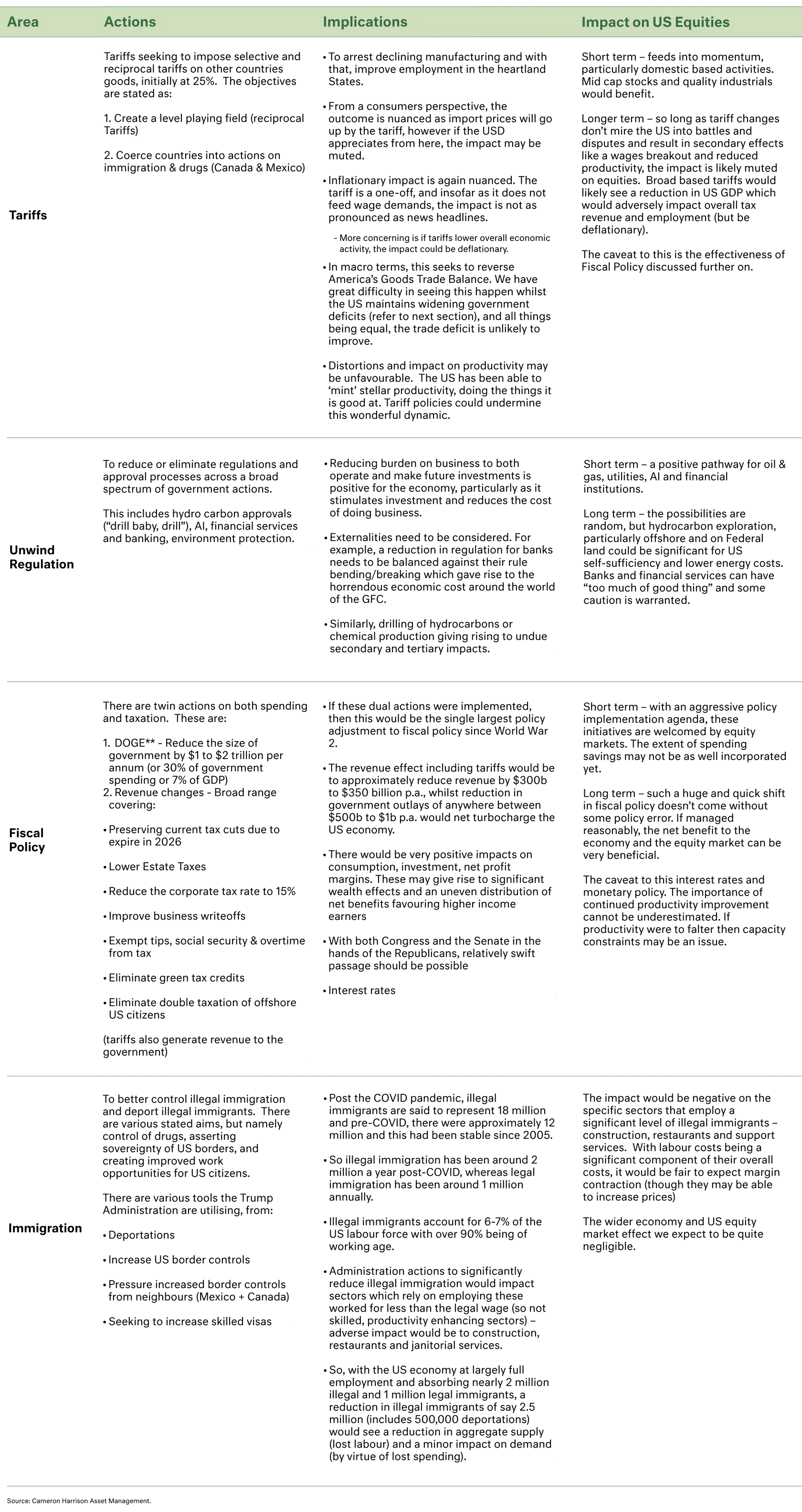

US Presidents are famous for their first 100 days and creating a momentum that will take them through the mid-term elections (in 2 years time) and then onto seeking a second term re-election. The Trump presidency is vastly different, because whilst a new president, there is no next term, having already served a term between 2016-2020. In legacy building terms, time is therefore of the essence, and this president is wasting no time. This begs the obvious. If the US economy is in such good shape, what are the implications of Trump’s economic policy on US equity markets? We think looking past the headlines and carefully examining, it is quite positive. That said, we do have significant reservations on the current level of equity market valuation, which to be fair, was present before Trump was elected. Trump’s policies as we now see them being implemented can grow the US economy and deliver significant wealth effect benefits. Our major reservation is the extent of economic policy change and business and households ability to absorb this generational change. (note – our analysis is only focused on the economic benefit, cost and flow-on effects to US equities)