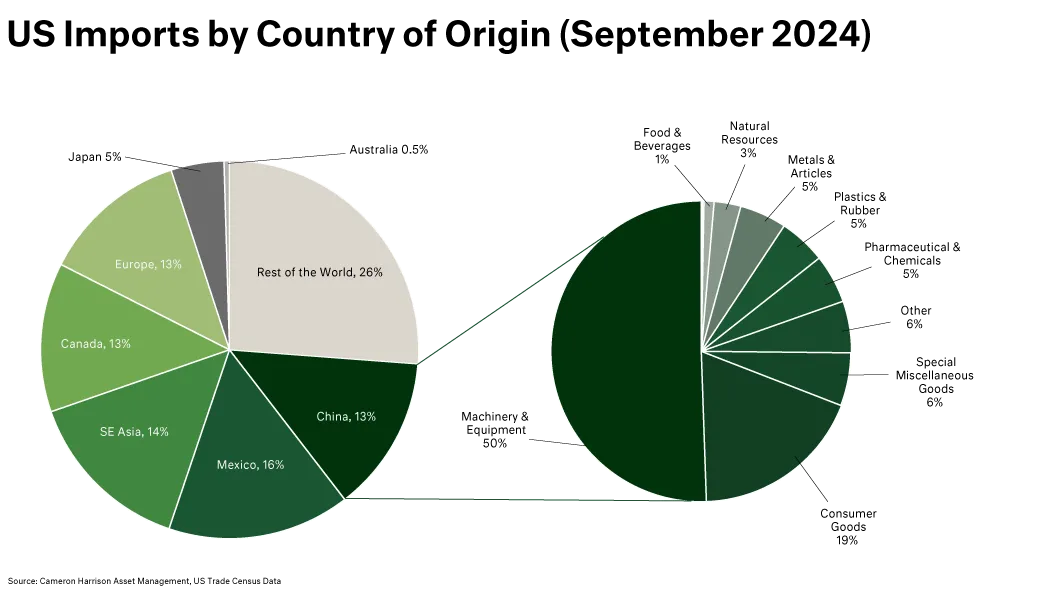

This month’s chart shows US Imports for calendar year 2024 (to end of September) split by country of origin as well as China’s imports on a goods basis. Mexico has recently overtaken China in terms of gross exports to the US. This was mostly a function of China’s zero-Covid policy induced supply chain dislocations leading to the US wanting a more reliable importer and favouring Mexico’s proximity.

US Tariffs: A Ripple Through the Global Economy

Market Insights |

Investment Solutions

Donald Trump’s proposed tariffs represent a fundamental shift in US trade policy, with profound implications for the global economy. While the immediate aim is to protect and strengthen American industries, the broader economic consequences extend far beyond US borders. From inflationary pressures to lower Chinese growth expectations – and the subsequent ripple effects on Australian exports – this policy shift underscores the interdependence of global trade networks.

Posted 21 November 2024

Trump’s proposed tariffs are designed to discourage imports in key sectors such as machinery, consumer goods, and energy, which collectively make up a significant portion of US imports. By raising the cost of foreign goods, the tariffs create a strong incentive to onshore production, bolstering domestic industries and reviving the US manufacturing base. This “America First” protectionist strategy aims to reestablish American dominance in industries deemed vital to national security and economic resilience. However, the transition is unlikely to be seamless. Reshoring supply chains will require significant capital investment, time, and a skilled labour force, presenting logistical and structural challenges in the short to medium term. This would likely put upward pressure (increased demand) on the US labour market, notwithstanding Trump’s other policy (deporting illegal immigrants) would reduce the labour supply. The perfect wage-fuelled inflationary storm.

At the same time, these tariffs will contribute to higher consumer prices in the US, resulting in structurally elevated inflation. For goods such as machinery, pharmaceuticals, and energy – where import reliance remains high – the increased costs will be swiftly passed on to consumers. This inflationary pressure complicates the Federal Reserve’s mandate, as rising prices could force less lenient monetary policy, and less willingness to reduce interest rates. Such measures risk curbing domestic consumption and investment, likely adding downward pressure to US economic growth. For capital markets, this inflation-exporting dynamic could create headwinds in trade-dependent regions.

The economic implications of these tariffs are particularly significant for China, one of the largest exporters to the US. Reduced US demand for Chinese goods – ranging from consumer electronics to industrial machinery – could slow Chinese economic growth, especially in export-dependent sectors. This poses a critical challenge for Australia, given its deep trade ties with China. Australia’s economy is heavily reliant on the export of commodities such as iron ore, coal, and liquefied natural gas, with China accounting for over 30% of Australian export revenues. A slowdown in Chinese growth would directly reduce demand for Australian exports, pressuring commodity prices, weaker job creation, slower real wage growth, and reduced government revenue. We would also expect dampening economic growth domestically.

Ultimately, while Trump’s tariffs aim to recalibrate the US economy, the ripple effects demonstrate the interconnectedness of global trade. For Australia, the policy is a stark reminder of its economic exposure to exogenous shocks – underscoring the need for resilience in an increasingly protectionist world.

Speak to one of our advisers to learn more:

david.clark@cameronharrison.com.au

Sourced from:

Photo by iStock