Given the pace of credit growth more broadly in the economy and specifically in the non-bank sector, there has been a lot of media attention in 2024. Stories of deals gone bad and poor management have made headline news, but this ignores the broader asset class that is as well-diversified as any major bank lending book. Just like any asset class or superannuation fund manager, there are excellent, experienced risk managers, and then there are less experienced and less credible managers.

Private Credit

Investment Solutions

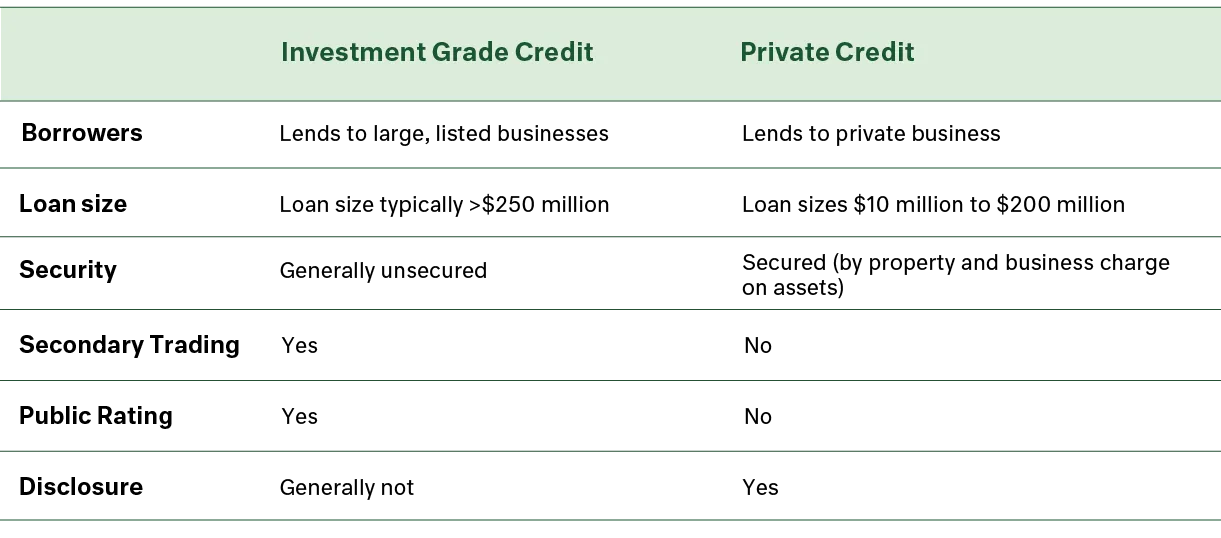

Private credit is the provision of non-bank finance. As such, credit is provided for various purposes; property and development funding, a multitude of business lending ventures, both direct or structured, which itself can fund personal and business risk.

Importantly, banks avail themselves to a range of funding and risk alternatives. As traditional banks have stepped back from lending other than to household mortgages (where regulatory risk capital requirements are more favourable), non-banks have been left to fill spaces where banks do not want to operate. Banks used to be the main intermediator of credit in the economy. In the United States, bank intermediation has undergone a sharp decline for over 20 years. This is now occurring at a quickening pace in Australia.

Posted 16 January 2025

The private credit asset class has been borne out of banks retreating from lending to businesses in preference of lending to household owner occupiers. Essentially, they are loans between non-bank financiers (ultimately private institutions and investors) and private business borrowers.

Compared to traditional investment grade credit, well-operated private credit lenders provide finance to smaller businesses or projects, usually with greater security terms, protections and diversification. Banks on the other hand, tend to lend to larger risks in larger amounts.

The asset class has become more popular as institutional and wholesale investors look for ways to increase risk-adjusted returns on secured investments.

Private credit lending in Australia has doubled in four years to close to $40 billion, according to RBA estimates, with most of this coming from the growth in size and number of private credit managed funds.

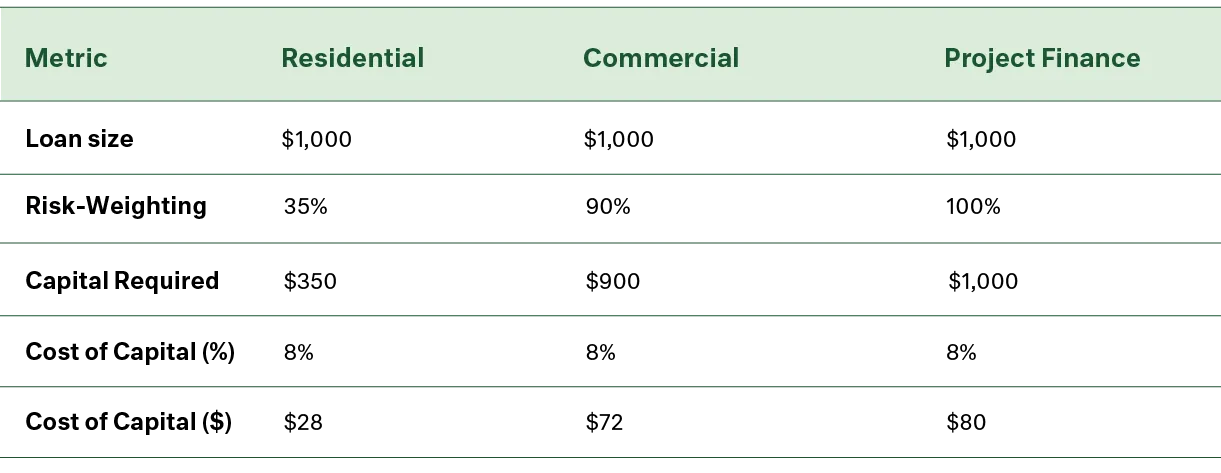

A big driver of this is bank regulation. Banks are moving away from business lending and becoming more focused on residential lending, largely due to lending standards and capital requirements for Australian banks. In short, banks are required to hold more capital (equity, hybrids, subordinated debt) against business, commercial and project finance loans, as opposed to residential loans. This creates a bias to residential lending as it becomes cheaper to finance, as illustrated in the example below.

APRA requires banks to hold minimum amounts of capital against the loans they make, and those loans are risk-weighted according to a standardised formula. If a 10% capital ratio is required, the bank will have to hold $100 of capital for every $1,000 of loans made. However, loans are ‘risk-weighted’ based on their type.

An owner-occupier loan with an 80% loan-to-valuation ratio (LVR) attracts a 35% risk-weighting, so the bank only has to hold $350 of capital for a $1,000 loan. A similar commercial property would attract a 90% risk-weighting and a project finance loan may attract a 100% risk-weighting, meaning the bank needs more capital to fund these loans.

Let’s assume a cost of capital of 8%. We can see the impact of risk-weighted capital requirements on the cost to the bank.

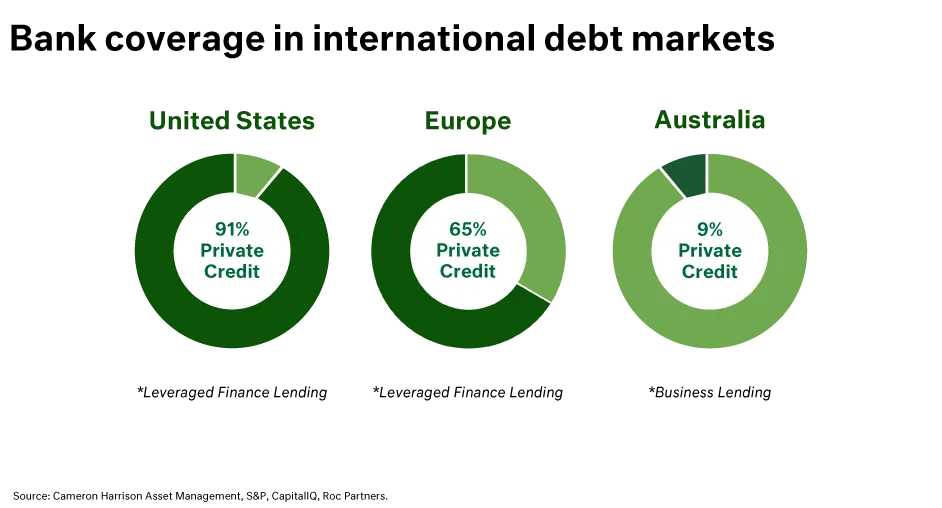

Despite the recent growth in private credit in Australia, by international standards the amount of business lending by banks compared to private credit is still minimal, allowing for further growth in this sector. Only 9% of business lending in Australia is provided by private credit, meaning 91% of business lending is still done through banks. In contrast, 91% of business lending in the US is provided through private credit lenders.

As the Australian private credit market matures, we expect to see more growth in the amount of business lending being done through private credit lenders compared to traditional banks, who continue to move towards providing only residential mortgages.

To get an idea of what is happening at the coal face of the private credit economy, we spoke with Drew Bowie (MA Financial) and Bob Sahota (Revolution Asset Management), two portfolio managers of their respective private credit funds. MA Financial focus on real estate credit through their Secured Loan Series, whilst Revolution diversifies across business, stabilised real estate and asset-backed lending.

The residential market will remain a focal point for MA Financial in the first half of 2025. Bowie notes “The opportunity for well-constructed first mortgage positions remains very strong and provides excellent returns.”

An increase in viable residential development transactions is expected, supported by normalising construction costs and supportive government planning. “Governments are mobilising to improve efficiencies around planning and are keenly focused on vastly increasing construction starts for new supply,” Bowie explains. This progress is expected to reduce lead times, lower holding costs, and make residential development projects more viable.

Whilst residential real estate is attractive, opportunities in the industrial sector remain limited. Bowie cautions, “we are not expecting an abundance of opportunities in the industrial sector, which remains tightly held.” However, maintaining some exposure to industrial assets within a diversified portfolio remains a prudent move for investors.

The office market demands a nuanced approach. “The pure work-from-home impact appears to have stabilised, and a hybrid model is increasing in importance, whilst total demand for professional services is increasing—and with that, demand for office accommodation,” Bowie observes. The shift to remote and hybrid work models appears to have stabilised, creating a more predictable environment.

According to Sahota, equipment and auto finance stands out as a good risk-adjusted opportunity for Revolution. “We continue to see the equipment finance subsector as a strong opportunity with banks pulling out and focusing predominantly on vanilla prime mortgages because it’s the largest overall market and the capital rules are very favourable for them,” he notes. With banks narrowing their focus, private lenders are well-positioned to step in and address this gap in the market.

In business lending, Sahota notes Revolution is “focusing on the more traditional bank-style deals, characterised by moderate leverage levels, and the presence of at least one covenant, while concentrating on market-leading businesses in non-cyclical industries.” This strategy prioritises stability, leveraging strong equity buffers and covenants to ensure downside protection. By focusing on non-cyclical industries, Revolution aims to provide more predictable performance, a critical consideration in uncertain times.

In an environment of economic uncertainty, Bowie emphasises the importance of maintaining a disciplined and cautious approach to private credit investments. “We remain cautious and expect to only compete on a small fraction of the opportunities we see (historically 5-10%),” he says. This measured strategy includes focusing on quality over quantity and ensuring conservative loan-to-value ratios, particularly in the residential sector, which remains a cornerstone of the strategy.

Revolution takes a similarly measured approach in its business lending positions through leveraged buyouts (LBO). “Overall, Revolution remains focused on the more conservative end of the LBO spectrum, preferring to give up some yield for the benefit of lending to stable, market-leading businesses in non-cyclical sectors with moderate leverage, large equity buffers, and covenant protection,” Sahota explains. This positioning reflects a commitment to sustainable performance and reduced volatility, driving robust risk-adjusted returns even in a challenging market environment.

The lender landscape remains distinctly bifurcated, with some lenders adopting a more aggressive stance. Sahota points out that “other lenders are being more aggressive in the capital structures they are willing to provide, whilst foregoing covenants.” This trend is particularly evident in the rise of covenant-lite transactions, which feature higher leverage levels and no covenant protection. While these deals may offer higher yields, they expose investors to significantly greater risk.

The private credit market is becoming more competitive with overseas lenders becoming more active, but retaining quality is key to protecting downside. Sahota notes “we are very cautious not to let our guard down and maintain very strict credit discipline in an environment where there are large international players who are aggressive on terms and pricing.”

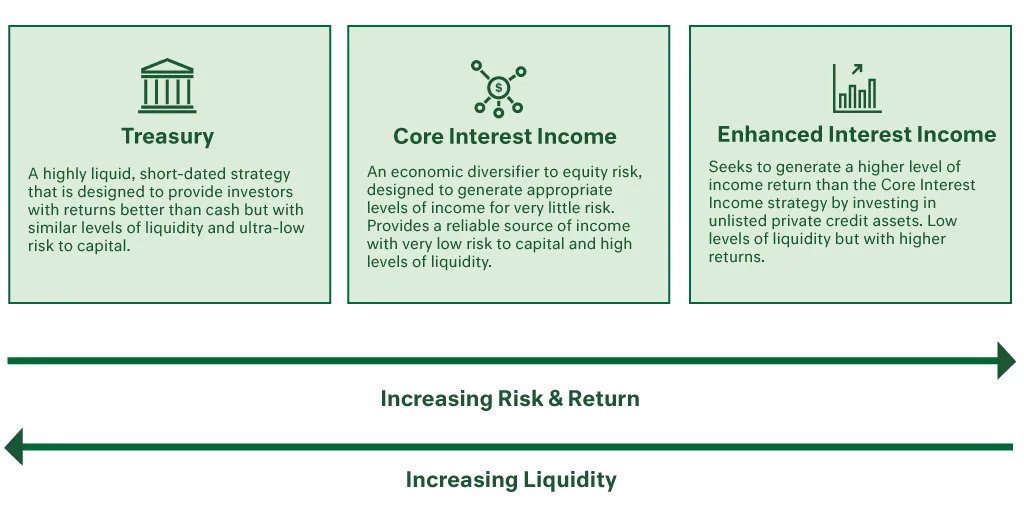

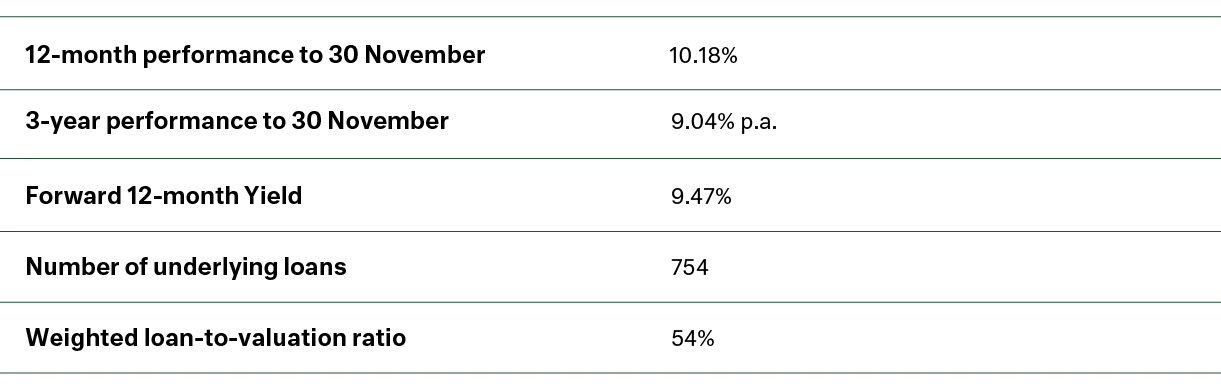

Our Enhanced Interest Income Strategy seeks to generate a higher level of income by investing in unlisted, private credit assets and unlisted managed funds. It is a supplementary strategy to our Core Interest Income Strategy, part of our Interest Income Strategies (illustrated below). Typically, the yield is 2% to 3% greater than our 'Core Interest Income Strategy.' Being invested in unlisted, private debt, this strategy has less liquidity than the Core Interest Income Strategy (which has extremely high levels of liquidity).

The ultimate purpose of the Enhanced Interest Income Strategy is to provide an additional yield to a client’s portfolio through investing in appropriate secured debt investments with some reduction in liquidity. We seek returns for defined and consistently managed risk, what we describe as optimal returns. Our risk parameters management is our primary focus when managing our various strategies. It is fundamental to long term capital preservation. We review managers and opportunities through our strict due diligence criteria, resulting in a highly diversified exposure to loans.

Our due diligence framework for our Enhanced Interest Income Strategy procures the very focused and highest quality participants. This ensures our strategy constituents clearly demonstrate appropriate diversification, expert risk management, sufficient legal protection and experienced management teams.

Should you wish to know more about our Enhanced Interest Income Strategy, please please contact us on +613 9655 5000 or contact our experts here.

Paul Ashworth, Managing Partner

Anne-Marie Tassoni, Partner

David Clark, Partner

Tristan Bowman, Partner

Speak to one of our advisers to learn more:

tristan.bowman@cameronharrison.com.au

Sourced from:

Photo by iStock