There is more complexity in the RBA’s decision than past rate cut cycles and when compared with where the US Federal Reserve is positioned. This rate cycle also sees the Australian household debt burden (principal + interest relative to income) at all-time highs. Mortgaged households are acutely leveraged to the position of the cash rate over the next 12 months. Despite higher inflation eroding interest returns, investors in short-term fixed income securities have benefited from higher yields. The private economy is awfully weak and wanting to see its share of activity improve, particularly consumption.

Economic Strategy – Assessing the RBA’s next move on the Cash Rate

Investment Solutions |

Specialist Advice Solutions |

Wealth Management Solutions

The Reserve Bank of Australia (RBA) is faced with assessing and determining a possible rate cut cycle for the cash rate throughout 2025.

Posted 16 January 2025

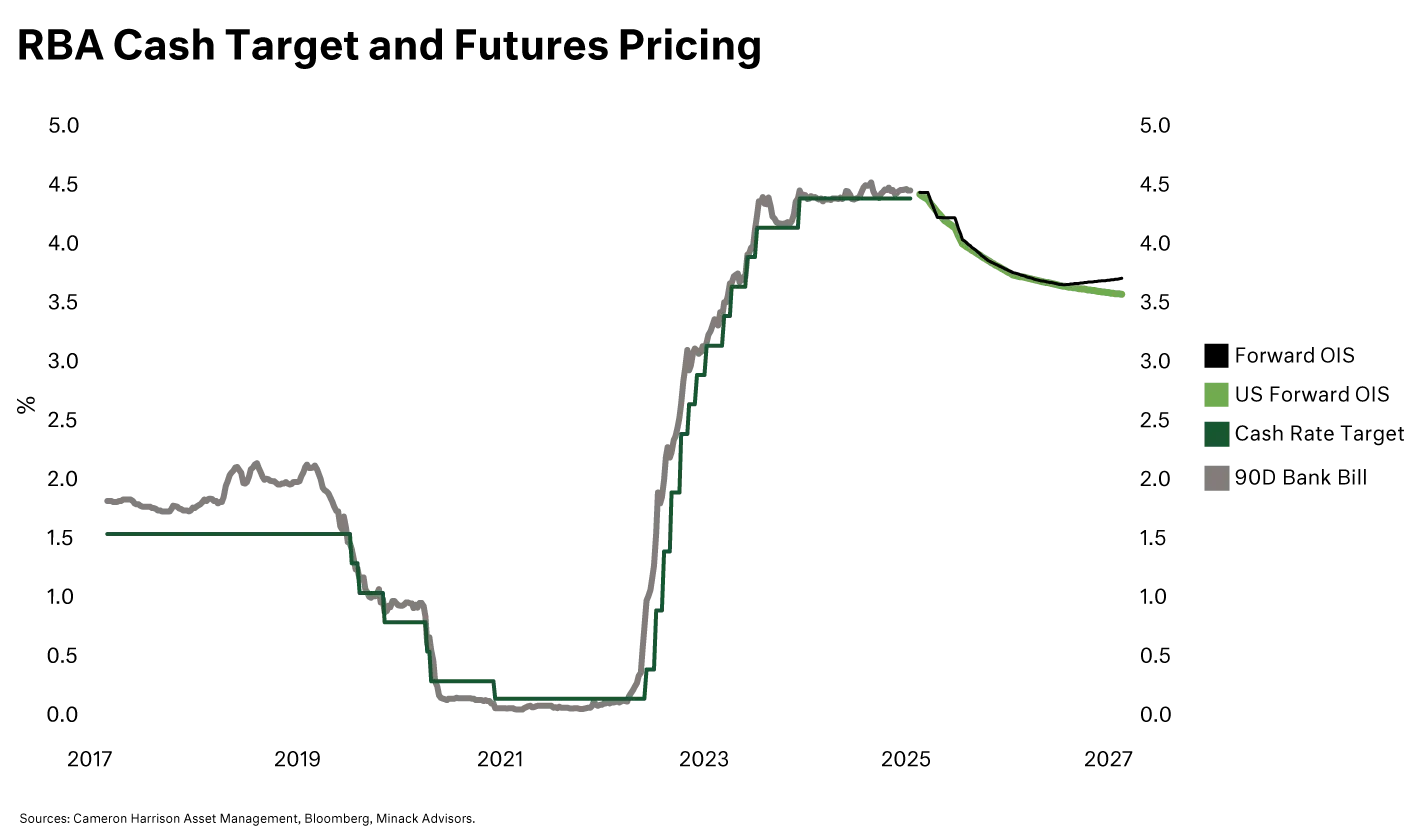

The current RBA Cash Rate is 4.35% p.a. The US Federal Funds Rate is targeting a range of 4.25% to 4.5% p.a.

The RBA was both slower and more moderate in its rate increase cycle than the US Federal Reserve. Similarly, the RBA has yet to cut the cash rate whereas the Fed has already initiated two rate cuts.

Australian economic growth and employment is almost solely being led by public demand in the form of Federal spending (NDIS, other health related expenditures, new programs and increase in the public service), as well as State spending (infrastructure and burgeoning public service).

Chinese demand for our key bulk exports is weakening which is largely a national income effect (and tax revenue hit). That said, the AUD/USD depreciation is cushioning the impact.

The Federal Budget Cash Deficit is expected to be -$27 billion in 2024/25 and average $35 billion over the forward estimates. Taxation receipts have grown substantially by up to $24 billion p.a., but the Federal Government has increased spending by over $40 billion p.a. Where the RBA have tightened financial conditions (with negative real rates), the Federal Government and certain State Governments have loosened financial conditions – monetary and fiscal policy contradict one another.

The labour market is tight with unemployment trending lower to 3.9%, with public sector employment growth almost solely the contributor to employment growth. The private economy is stagnant and in recession.

Wages growth is moderating in an environment of strong employment. The economy may be able to generate lower inflation with a lower unemployment rate. Weak household income is also a drag on consumption and economic growth. This is supportive of lower cash rates, but the RBA may wish to see further data releases to gain greater confidence that the economy does in fact have this spare capacity.

Inflation, as measured to the trimmed mean has been falling, and the December quarter result will likely sit around 2.6%, annualised for the last six months. This is supportive of lower cash rates.

Headline inflation will appear a bit messy with government electricity subsidies and State Government reliefs ‘washing’ out of the data. Fuel prices are likely to add to headline inflation. The further depreciation of the Australian dollar will add to price pressure. A cut in the cash rate might put further downward pressure on the dollar which whilst potentially viewed as unhelpful in the context of inflation, is otherwise beneficial to our competitiveness.

In summary, the RBA is precariously placed given the opposing policy approaches between the government (big spending, stimulate) and the RBA, who are endeavouring to reduce inflation expectations and increase real incomes for households.

There are two key watchpoints as follows:

Trimmed mean inflation is under 3% p.a. for at least 6 months – this is likely to be satisfied for the December quarter.

That the economy does not operate in excess of its capacity, largely evidenced by unemployment being nearer 4.6% (currently 3.9%) – this appears the major difficulty and is contrary to the RBA’s modelling on demand and capacity.

This is further complicated by significant government spending mudding-the-waters. Were it not for this government spending and public related employment, the rate of unemployment would likely be increasing. The problem is, the government is not stepping back. This may see a reticent and further wait and see approach by the RBA.

By virtue of raising later and by not as high as the US, the RBA probably views that it has capacity to wait and see more data. This means waiting until the March quarter inflation, wages growth and employment data. Inflation data is supportive, and the private economy’s weakness could materialise into an unnecessary deep contraction of economic activity. Unemployment is certainly not at the (higher) levels where the RBA would be comfortable to cut rates (though government employment largely explains this).

The ”animal spirits” of the private economy are precariously positioned. Business confidence is improving with the prospect of a rate cut cycle, higher prices and revenue being met by solid employment outcomes and higher incomes for non-mortgaged households, alongside a desire to invest. On the other hand, consumer confidence is again weakening, with mortgage stress and cost of living pressures continuing.

This is a fine line to balance. All things equal, we think the RBA can afford a 25 basis point cut in February and then a review at the May meeting. It would be an “insurance policy rate cut” to stabilise the private sector “animal spirits”. With policy rates for cuts in the US and UK not as assured nor on a sequential monthly regime, the RBA can follow a similar approach. Even if the RBA does cut in February, the further cut trajectory is less than certain, and the bottom of the cycle may be 3.75% from a current 4.35%. We would also note that the pass through to borrowers of any rate cut is impacted by a lag in pass through by institutions who in addition are passing through less than the cut in the cash rate. However, we cannot lose sight of the menacing effects of sustained higher than range inflation on households and living standards.

In Australia, we view inflation taming as a serious threat and issue. We have arrived at this unenviable position through past policy failure and current government fiscal policy at both the Federal and State level further fuelling and exacerbating the price index. It has never been truer about there being “no free lunches”. Whilst it would be harmful to the private economy with moderate impact to employment outcomes, the RBA should probably wait to May to assess conditions. This decision largely turns on the December quarter CPI data release on 29 January 2025.

We also note that the new RBA Monetary Policy Board comes into effect on 1 March 2025. A Federal Election needs to be held no later than 17 May 2025. The RBA Monetary Policy Board are set to meet on 19-20 May 2025.

Cameron Harrison have been advising business owners and their families on asset allocation and intergenerational wealth management for over 50 years. We have demonstrated over a long period our ability to manage investments through both the good times and bad by keeping the client at the centre of our business.

To discuss our approach to investment management or any other inquiries, please contact us on +613 9655 5000 or contact our experts here.

Paul Ashworth, Managing Partner

Anne-Marie Tassoni, Partner

David Clark, Partner

Tristan Bowman, Partner

Speak to one of our advisers to learn more:

paul.ashworth@cameronharrison.com.au

Sourced from:

Photo by iStock