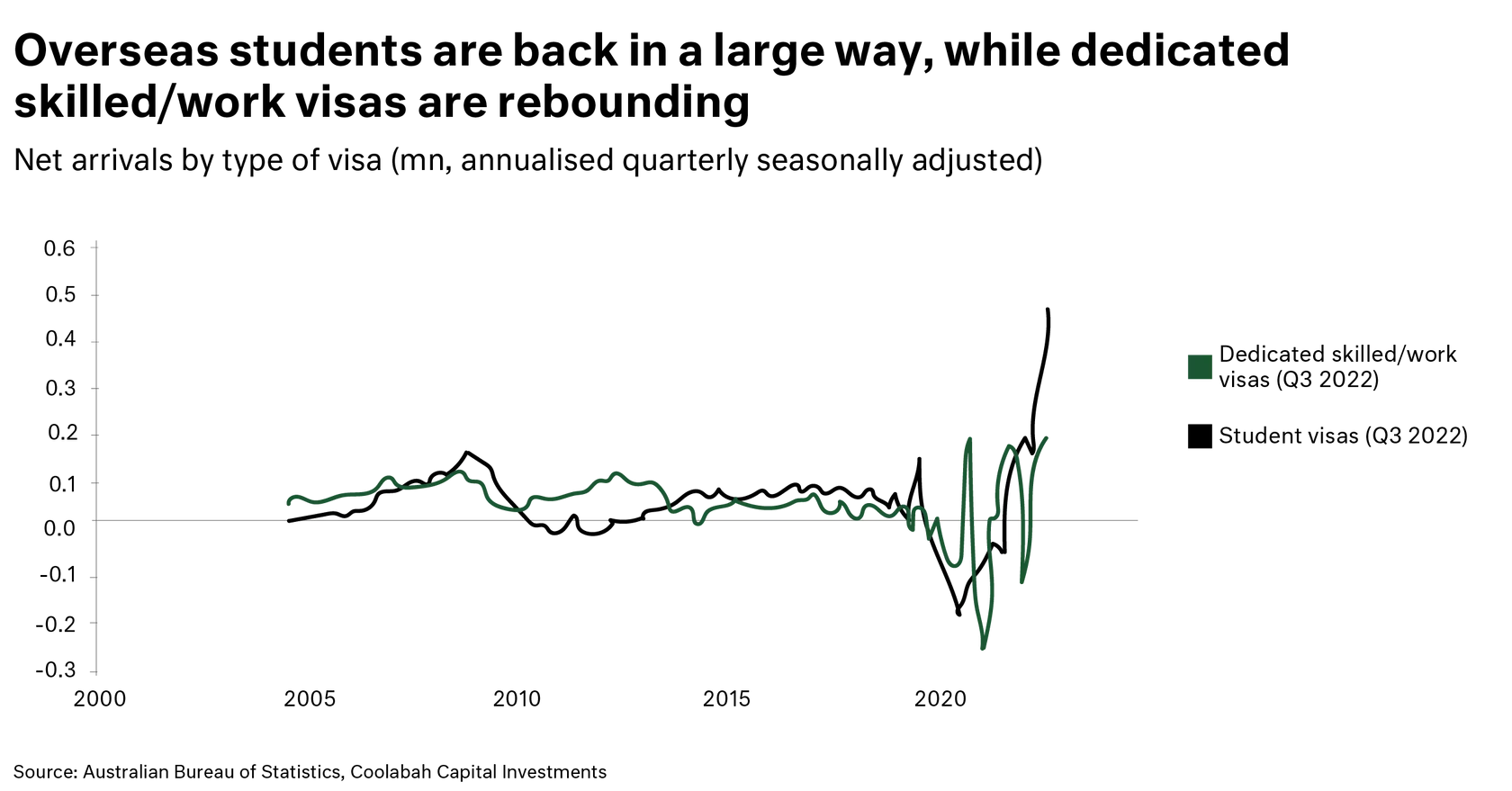

Australian inflation is due to overseas factors (war, energy prices, supply chains) and not by wage growth-driven services inflation. Based on the visa issuance data (below) we expect to see a surge in immigration, approaching 400,000 to 500,000 over the next 12 months.

Government policy still likes (loves) immigration. State and Federal Budgets need the population growth 'sugar fix'. The cost is low real wages growth, low per capita growth, and strained public services, but the upside is lower interest rates and increased tax revenue.

If immigration does significantly materialise, then inflation will be a rear-vision issue and the economy will look & feel like pre-Covid. We would expect to see a pivot in monetary policy to falling rates with significant (positive) implications for property, rents, and valuations.