The Federal Reserve System was established by Congress in 1913. Prior to its establishment in 1913, the US had experienced a number of significant financial crises1, most which were almost single handedly managed by a single private man and banker, John Pierpont Morgan (J P Morgan). There was assessed to be a need for government to put in place a permanent system for continuous monetary system oversight – financial crises, of which there had been many, could not be solved by a single man (Morgan himself died in 1913) and the United States had become the world’s largest economy around 1890.

The idea of establishing a central monetary system was highly contentious and many argued an overreach for a government body. Some 111 years later, similar sentiments abound as to whether the Federal Reserve (the Fed) should be accountable not just to Congress (legislature) but also directly to the President (executive). If answerable to both the Congress for its mandate and to the President, the argument is how can the Fed dispassionately and in a non-partisan manner perform its independent mandate if answerable to the politics of the day?

Whilst far from perfect, western central banks are largely independent of short-term political direction, instead focussed on medium term price stability (inflation), employment and financial system stability. Since the early 1980’s and the inflation fighting stewardship of Fed Chairman Paul Volcker, central banks have broadly met their mandates.

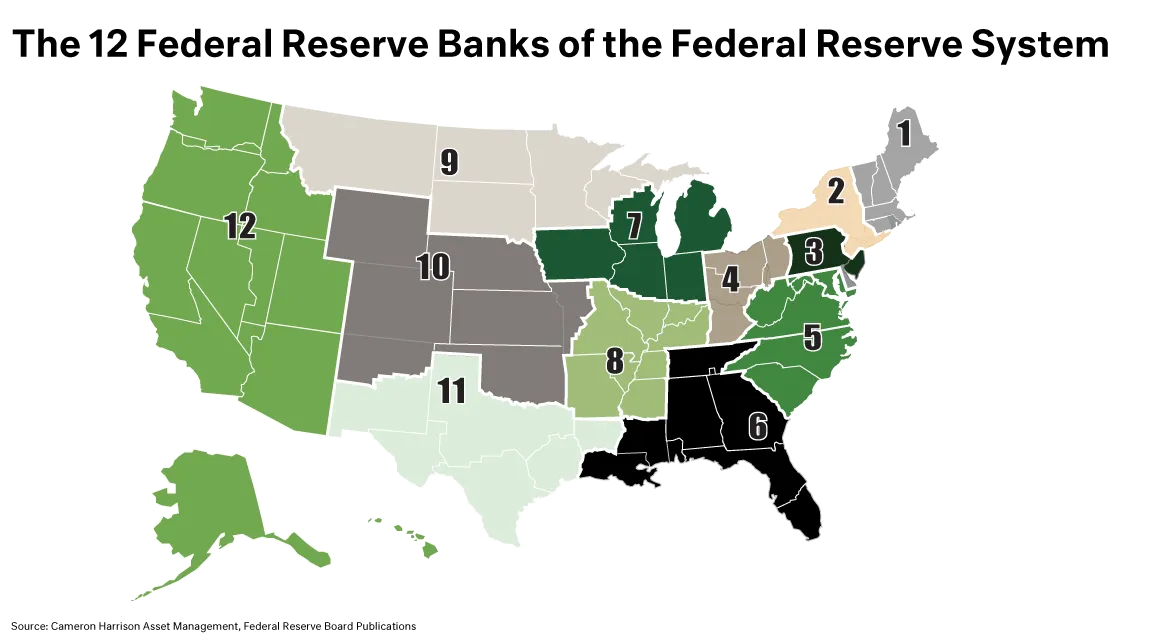

So, what is the Federal Reserve System of the United States of America?