The post GFC period of falling interest rates created a tide that lifted all boats. It was a period of limited, gradual change, with it seemingly harder to fail than succeed. That changed in 2022 when interest rates rose, exposing the cracks in Australia’s economic facade.

The US is heading towards a higher growth, higher wage environment underpinned by improving labour productivity. Whereas, Australia appears to be drifting back to the moribund environment that existed before covid. With the economy reliant on population growth and government spending for mediocre growth.

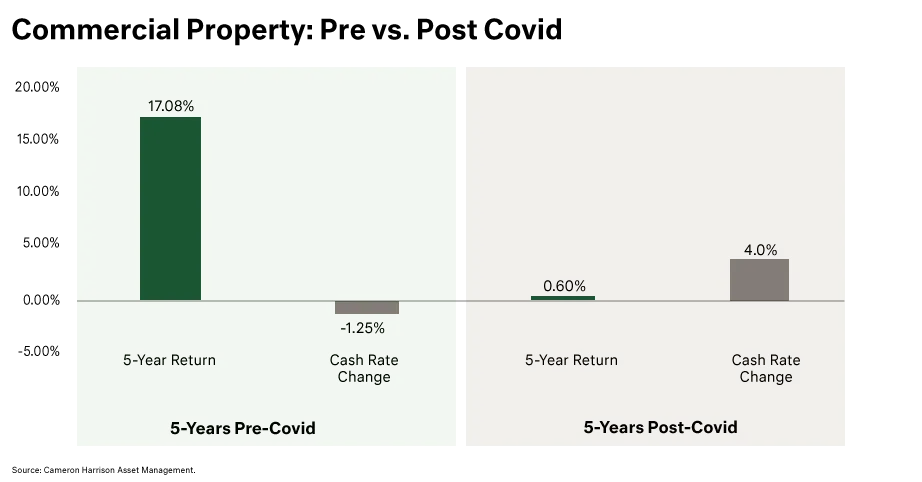

If Australia is to return to its pre-covid funk, it begs the question, what type of assets performed well during this period? The answer is commercial, and particularly, industrial property. In the five years leading into covid, listed property returned over 17% per annum in a period. In contrast, the 5-yr post covid, returns have been flat as the rising cash rate, which increased by 4%, weighed on valuations even as the underlying properties remained strongly tenanted and with sizeable rental growth.