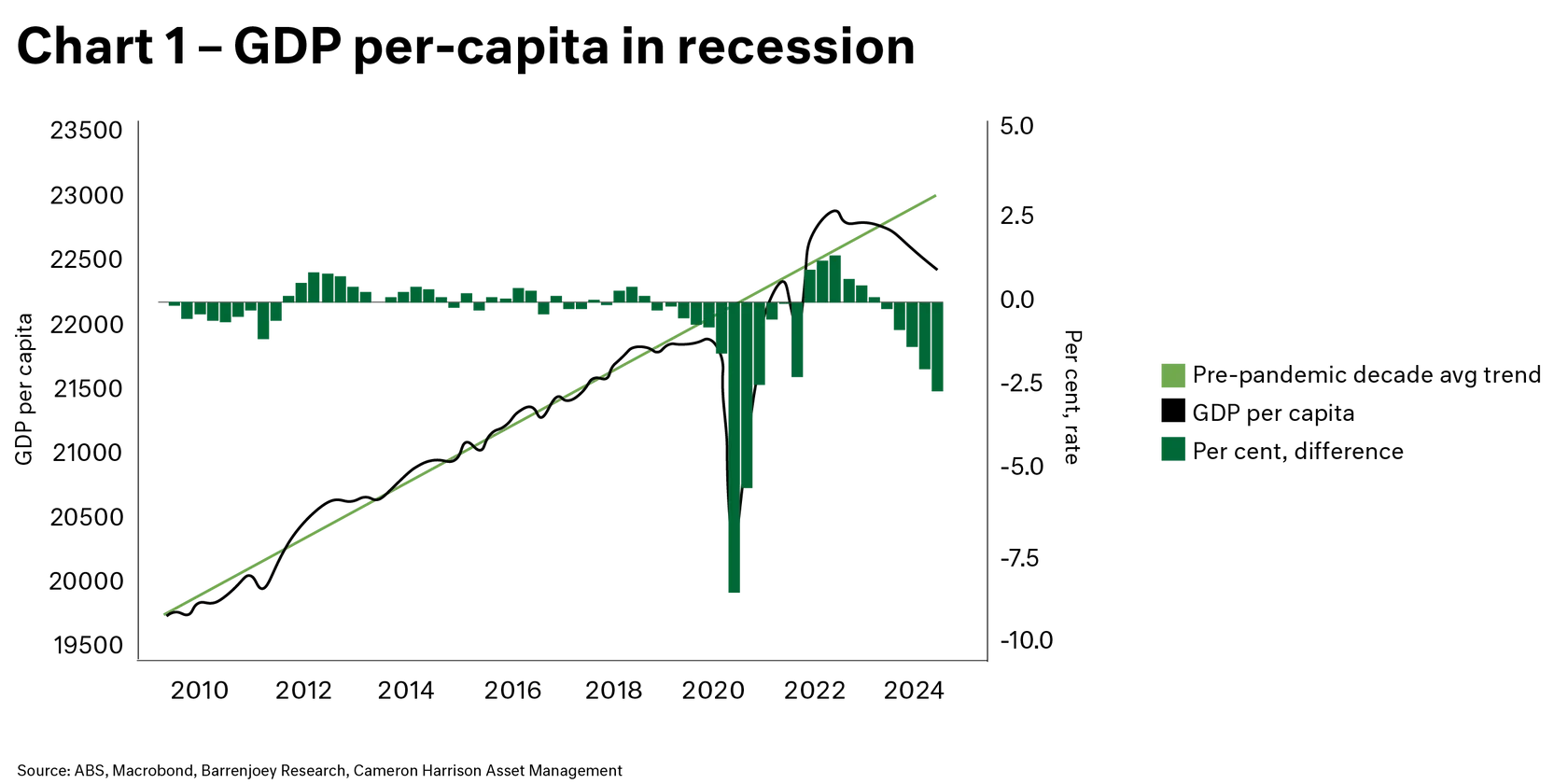

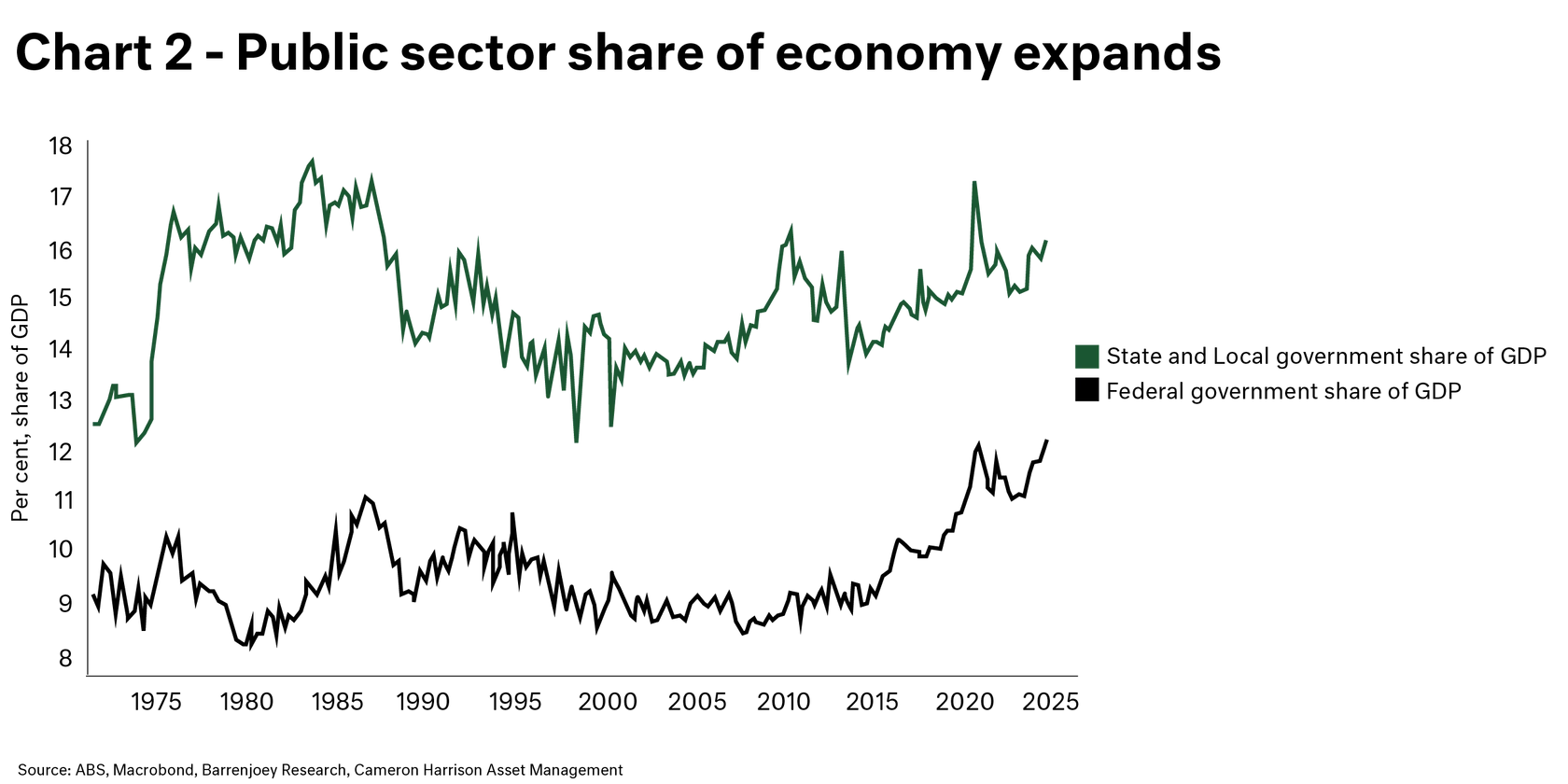

In a similar theme to our research note in August ('RBA - I say, therefore it is'), the Q2 Australian GDP figures show an economy that is basically 'stalled' at 0.2% for the quarter, with the two key engines completely divergent. The private domestic economy is contracting whereas the public sector contributed postively to growth. The RBA and Government are for all intensive purposes in significant policy conflict.

The RBA will be unswerving in its policy objective to bring inflation back within range of 2% to 3%. Whilst this very weak GDP result is data that helps the rate reduction argument, the RBA have been clear - it will not occur until 2025. We have argued for some time that the RBA's monetary policy stance is certainly sufficiently restrictive. We can see this in the capitulation in household consumption (which is of some concern), the savings rate at the lowest level in nearly 20 years, and an overall contraction in the private sector economy. Overall, this sees economic growth of 1% pa, a level last seen in the early 1990's (putting aside the COVID pandemic).