"Indeed, some commentators continue to call for further tightening in monetary policy. But as I noted earlier, we have been trying to balance bringing inflation back down over a reasonable timeframe, without inflicting unnecessary damage on the labour market. And the Board’s judgement to date has been that policy is currently sufficiently restrictive to do that."

Australian Interest Rates

Market Insights |

Investment Solutions

The Reserve Bank Governor Michele Bullock has plainly stated that the cash rate in Australia will not be cut in the near term and at the earliest, in 2025. Some fixed income commentators, demanding the RBA increase the cash rate by 50 basis points, appear tone deaf to the RBA's position which has been unequivocally stated by the RBA Governor on 16 August 2024:

Posted 21 August 2024

Their approach is a clearly stated balance of risks assessment which is well spelled out in the August RBA board meeting minutes. Data could surprise on the upside, and the RBA has equally said it is prepared to act by raising rates if needed. This however is not their current base position. We see no valid basis to reject the RBA's current hold-for-longer approach.

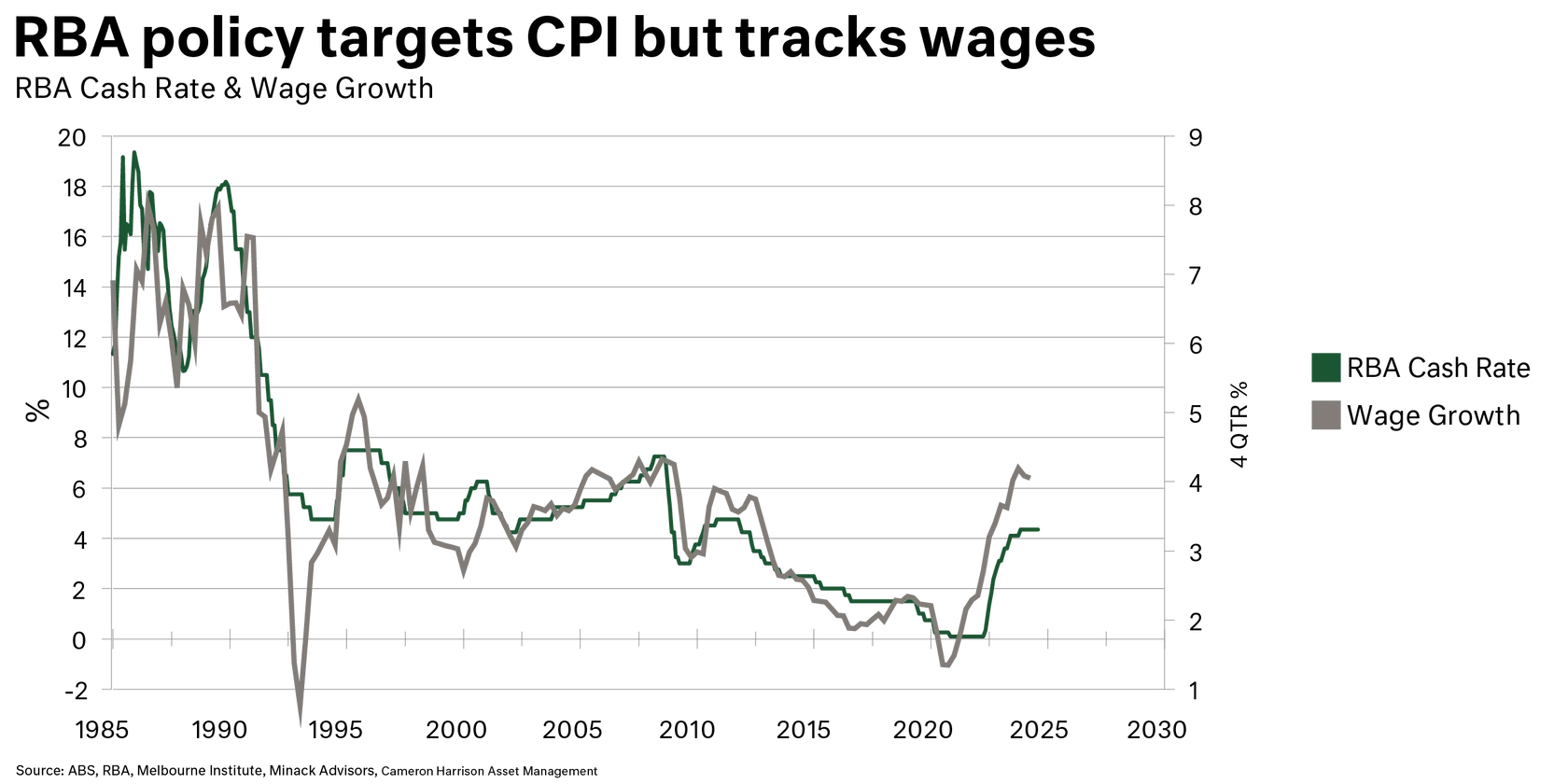

The RBA was slower than other central banks in raising cash rates, due to wages growth being stronger overseas. With other central banks now cutting their cash rate (Canada, UK, New Zealand), the RBA is somewhat more cautious in the balancing of its objectives of price stability (2% to 3% cycle range), full employment, and the economic prosperity and welfare of the Australian people. It is full employment and more specifically the level of wages growth which likely tests the RBA the most at present. Further moderation in wages growth is likely to be critical in the RBA's willingness to lower the cash rate in 2025.

As we can see below, wages growth (grey line), whilst modestly tapering, is still "highish" given the constraints on productive capacity in the Australian economy - more on that later.

The labour market is showing signs of loosening. This is observable with increased labour force growth (ie. more people looking for work) exceeding employment growth. Labour market underutilisation is also increasing. All are factors which assist the RBA in its narrow path, hold-and-wait policy to the cash rate.

External factors are increasingly impacting the RBA's assessment, particularly the Chinese economy and weakness in its property development sector. Since the beginning of 2024, the spot iron ore price (USD) is down 30%. This significantly impacts Australian National Income and in turn royalties and corporate tax receipts (the Federal Government having low-balled a $USD60 a tonne budget forecast which is still well under the current price of $USD97 a tonne). This is a 'downdraft' for the Australian economy which will support the RBA's hold-and-wait approach to interest rates.

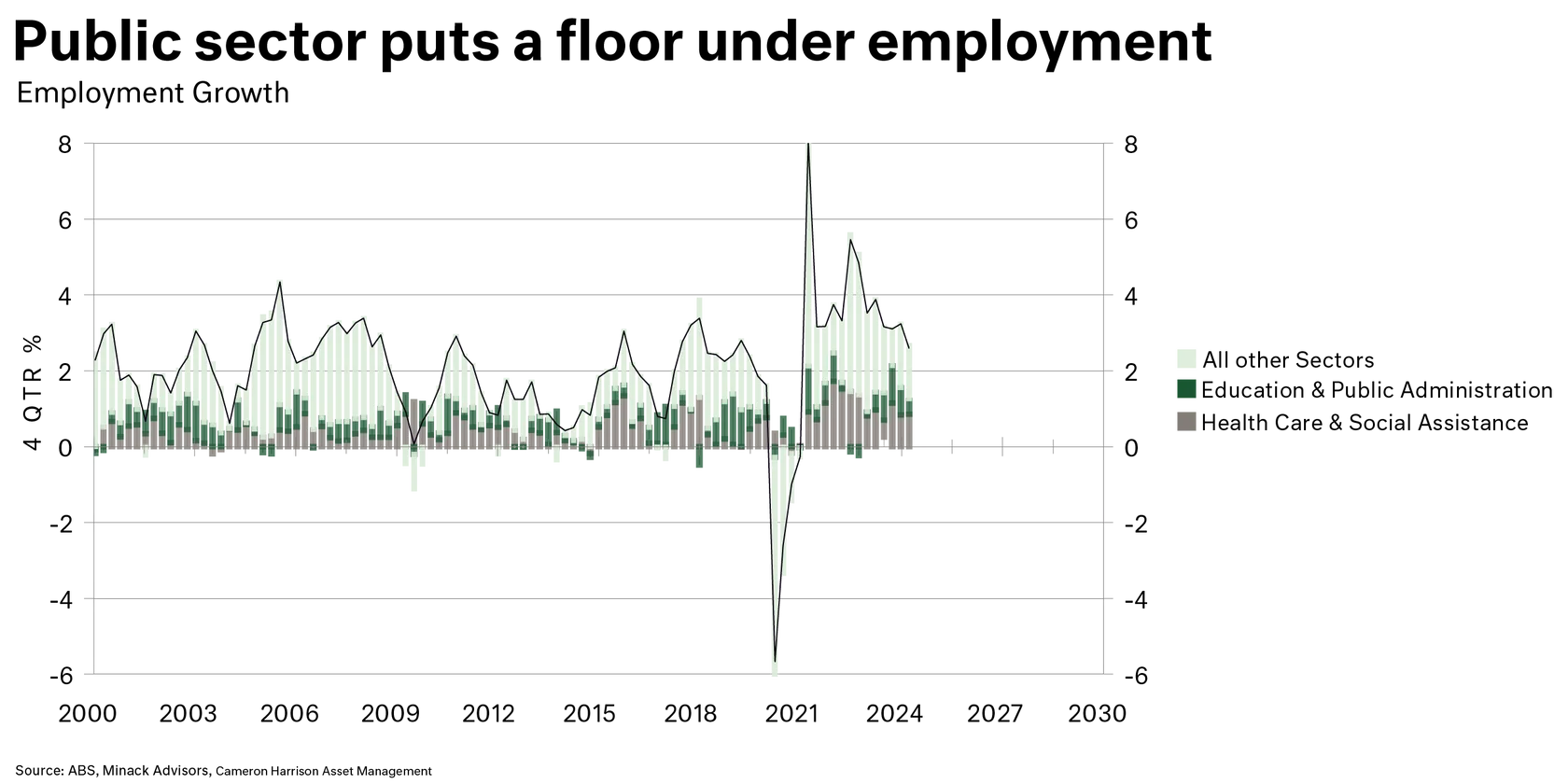

What has become more stark is the demand and employment dichotomy between the private economy and the public economy (government). We have recently commented on this. Where monetary policy is actively seeking to restrict economic activity. State and Federal Governments are stimulating economic activity. Monetary and fiscal policy are at odds and somewhat uncoordinated in bringing inflation back to target range. We can see above that government sectors (education health, NDIS) account for half of employment growth. In fact, more if we include government funded infrastructure projects. The Federal Government is somewhat more aware that it needs to constrain programs like the NDIS, but States remain completely belligerent and enthralled to their respective election cycles and willingness to spend (on their capital accounts), and in the process move their State finances to the economic precipice. On balance though, public stimulus should modestly moderate which again would support the RBA's current pathway for interest rates.

We consider the interest rate outlook for Australia and the United States to be somewhat different.

The US is producing reasonable economic & employment growth, even with a restrictive Fed Funds Rate of 5.35% pa. With scope for the Funds Rate to be cut by 1.5% to 3.85% pa, and assuming a positive yield curve, then US 10 Year Bond rates at 5% or more (currently 3.88% pa) seem both probable and problematic for equity and bond markets. Higher bond rates are something the market has almost fully discounted and unwisely so.

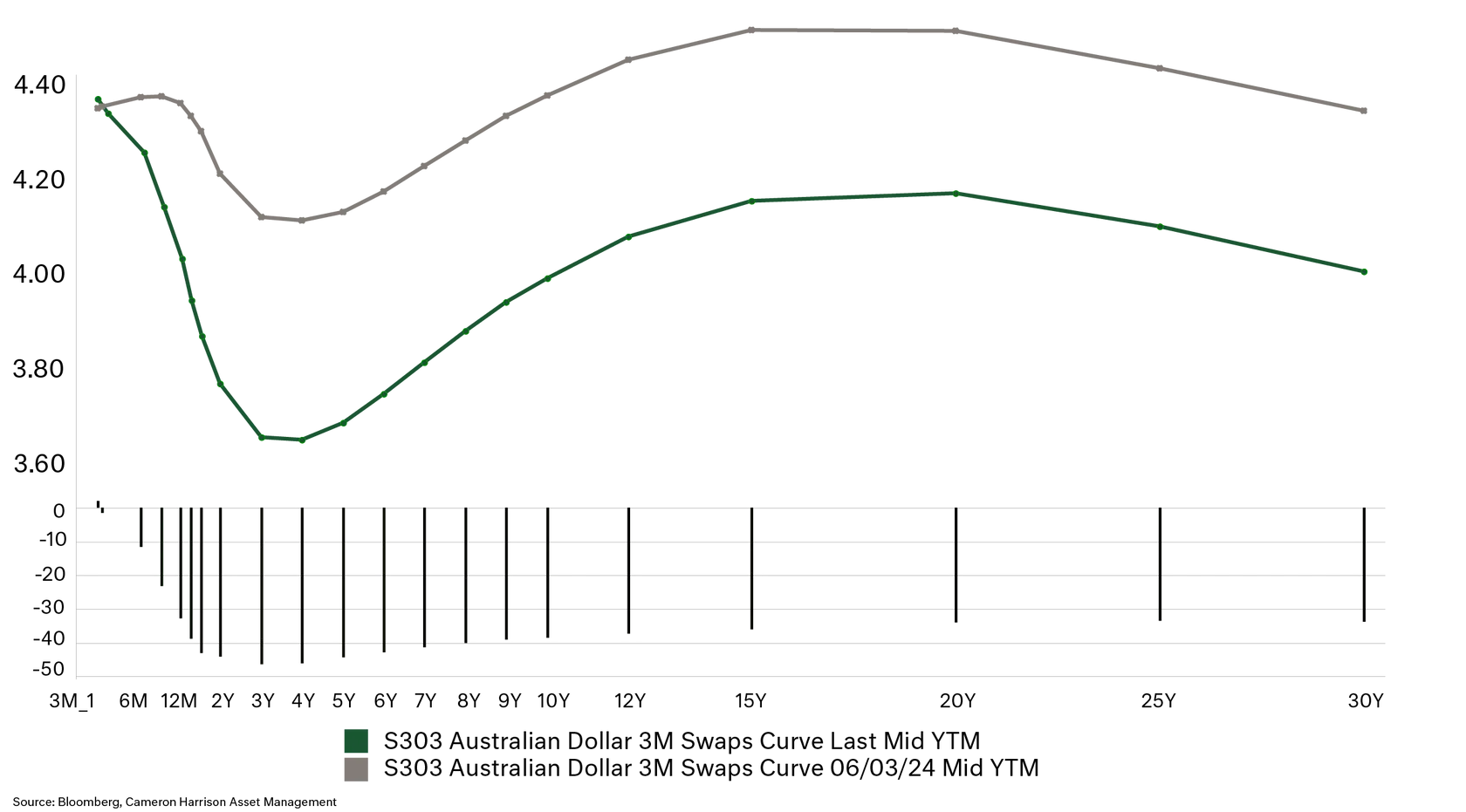

In Australia, we observe little evidence to suggest that our neutral cash rate is much different from pre-COVID; around 2% to 3% pa. Compared with 2019, the Australian economy is less productive, just as reliant on nominal growth through immigration (which conversely sees us with low per per capita GDP growth) and in turn low wages. The consequence for Australia may well be lower than expected cash and bond rates. In the chart below we can see (green line) that bond markets are now reflecting a more moderate bond rate view (3 to 10 years) compared with just June (grey line). These curves and hence bond rates may be headed lower again through 2025. This would be positive for bond markets and mixed for corporate earnings (reflecting anaemic growth). It would most likely underpin and restart Australia's long boom in residential house prices and further exacerbate the housing crisis in Australia.

Cameron Harrison have been advising business owners and their families on asset allocation and intergenerational wealth management for over 50 years. We have demonstrated over a long period our ability to manage investments through both the good times and bad by keeping the client at the centre of our business.

To discuss our approach to investment management or any other inquiries, please contact us on +613 9655 5000 or contact our experts here.

Speak to one of our advisers to learn more:

paul.ashworth@cameronharrison.com.au

Sourced from:

Photo by iStock