Since the onset of the pandemic, we have speculated that monetary policy will give way to fiscal excess as the main means of controlling the economic cycle (and reversing secular stagnation). Last night confirmed that this is indeed true. It also points to the end of the lower-for-longer interest rate environment that has dominated since the GFC.

Budget 2022 - Economic and Fiscal Implications

Investment Solutions |

Wealth Management Solutions |

Specialist Advice Solutions

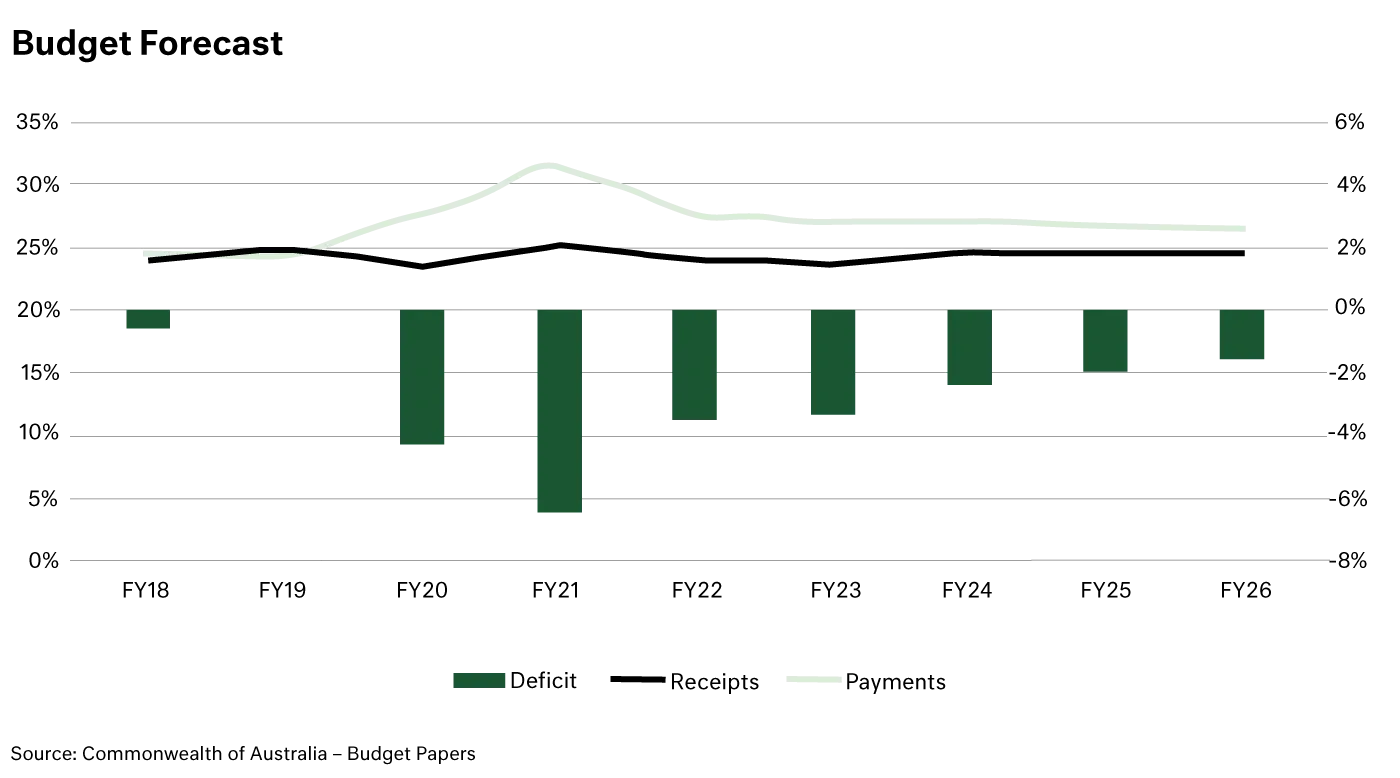

Against a backdrop of record low unemployment, high commodity prices, strong corporate profits and rising inflation concerns, the Government did not forecast a surplus, instead opting for a $78 billion (3.4% of GDP) deficit. This is the debt ‘floodgates’ fully open, the death-knell for fiscal restraint and the end of hope for surplus, in this decade at least. The obvious implication of this policy approach is that it leaves Australia with less policy flexibility for future crises.

Posted 30 March 2022

We discuss the investment and economic implications of this new environment in our webinar next week. Our keynote presenter is Gerard Minack of Minack Advisors.

In the aftermath of the GFC, governments opted for fiscal restraint and austerity. This magnified the demographic-driven lack of investment, resulted in ultra-low economic and wage growth and applied downwards pressure on interest rates. In the post-pandemic world, western governments are not intent on following the same playbook, instead we will see structural budget deficits in place for the rest of the decade and likely longer. This combines with a political trend in western, liberal democracies to underwrite utopian nirvana where moral hazard shifts to government away from private actors in the economy.

It should be noted that the structural deficit is not due to a weak underlying economy, with government receipts (taxes) totalling $557 billion, which is $71 billion larger than the pre-pandemic 4.7% per annum growth rate. Instead, the Government has a (massive) spending problem.

Since the pandemic, there has been a step-change in spending to over 26% of GDP from closer to 24%. This level of spending is forecast to continue for the rest of the decade, while government receipts remain stubbornly at 23.9% – the Coalition’s self-imposed tax limit. This outcome is the result of an embedded increase in spending on Defence, Healthcare (NDIS), Aged Care, Infrastructure and Energy / Climate mitigation that will not be unwound. Key measures are listed below:

– NDIS of $35.8 billion next year, forecast to double over the next ten years; a 7% per annum growth rate (double GDP growth) with total spending to exceed the total cost of Medicare.

– Turbocharged defence spending with a $10 billion increase in cybersecurity over the next ten years and $38 billion over 20 years to expand the number of defence personnel.

– Aged Care spending to rise by 9.4% in real terms in the next four years.

– $120 billion ten-year infrastructure pipeline, an increase of $17.9 billion with much of this directed to the regions in return for the Nations support on a 2050 net zero carbon target.

Yes and no.

From an economic theory standpoint, it is reasonable to target a constant debt-to-GDP level. Balancing higher debt against a larger economy in this way is commonplace in developed economies. There are however two issues with this approach:

It reduces the capacity for the Government to respond to future economic crises.

Spending is often focused on propping current consumption rather than productive measures that lead to higher real GDP.

The risk for Australia is this additional spending feeds directly into higher inflation without improving productivity. Wage growth without productivity growth, as we are currently experiencing, is unsustainable and risks leaving Australian labour uncompetitively expensive on a global basis.

At the onset of the pandemic the key measures of success for the Federal Government’s economic management was to avoid a rise in the long-term unemployed and to return to pre-crisis growth rates through improved economic productivity.

The Government has achieved the first measure with unemployment heading below 4%, an impressive achievement. It will take time to see if the supersized spending delivers improved productivity, but we see little to instil confidence that this will be achieved given the political motivations at play.

For investors, this budget is further confirmation that we are no longer operating in the low-growth, low-rate environment of the pre-pandemic decade. The future will see higher inflation, higher interest rates and higher nominal growth with implications across all asset classes.

For more information on how this new economic environment will impact your investments, register here for our investment and economic strategy webinar, presented on Wednesday, 6 April 2022 at 11.30am.

As partners in your investment journey, we monitor, examine, and navigate change. The Federal Budget is one such factor in our highly considered investment strategy and wealth management process.

This article is one part of our 2022 Budget series. To read more of our Budget commentary, click the links below:

– Individuals and Families

– Small and Medium Business

For more information on our approach to wealth and asset protection, please contact us on +613 9655 5000.

Speak to one of our advisers to learn more:

david.clark@cameronharrison.com.au

Sourced from:

Commonwealth of Australia – Budget

Photo by Unsplash