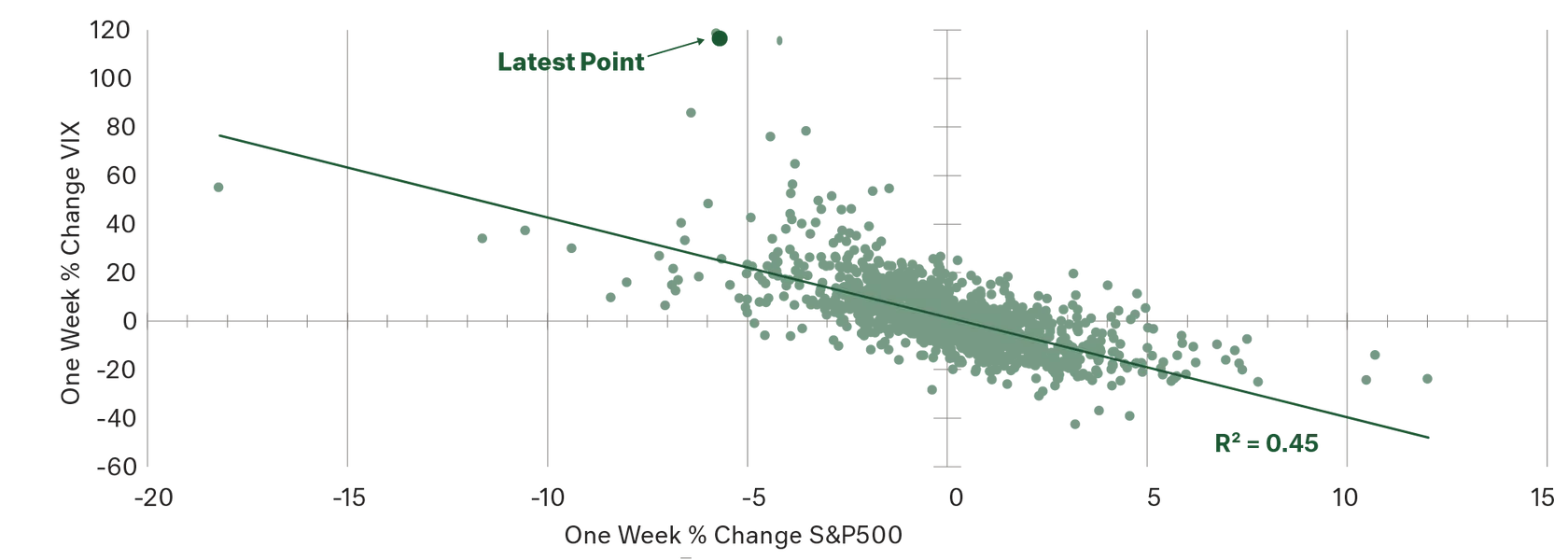

The recent equity market gyrations over the last 10 days heralds the end to Goldilocks equity volatility, of which the hallmark has been overly-benign volatility for the last five years. This market volatility has not been driven by weak company wide fundamentals or economic weakness. In fact, we are currently experiencing a US equity reporting season which has delivered robust earnings results and generally significant increases in dividends. That said, it would be naive to simply dismiss this extreme market volatility on short-term market factors.

Our core Cameron Harrison Economically Responsible Asset Allocation Strategy has been in a highly conservative setting for some time due to our assessment that markets had been poorly valuing forward risks. Markets overshoot and significantly undershoot; both scenarios afford good opportunities for disciplined, rule-based investors. Effective long-term investment management is ultimately about the transfer of wealth from the impatient to the patient.