What makes a soft landing?

Market Insights |

Investment Solutions

The problem in the US can be simply summarised as too much economic activity for too few workers. This has driven wage growth above 5% per annum, a level that is too high for the US Federal Reserve’s mandated 2% inflation target, forcing tighter monetary policy (higher interest rates) to reduce job creation and lower inflation. Given the size and speed of this rapid tightening cycle, a recession in the US is likely in 2023.

Posted 11 January 2023

Energy prices go up and down, but wages only go up. The solution to the economic woes in the US might sound simple – lower wage growth by 1.5% – but history has shown that wage growth tends to be sticky and monetary policy a blunt instrument akin to cracking a walnut with a sledgehammer.

If the Fed can engineer a steady uplift in unemployment and a slowing of wage growth without causing a recession (a so-called soft landing) then US Equities will rally strongly in 2023. Conversely, a steep increase in unemployment coupled with a recession (hard landing) will likely result in a second consecutive year of negative returns.

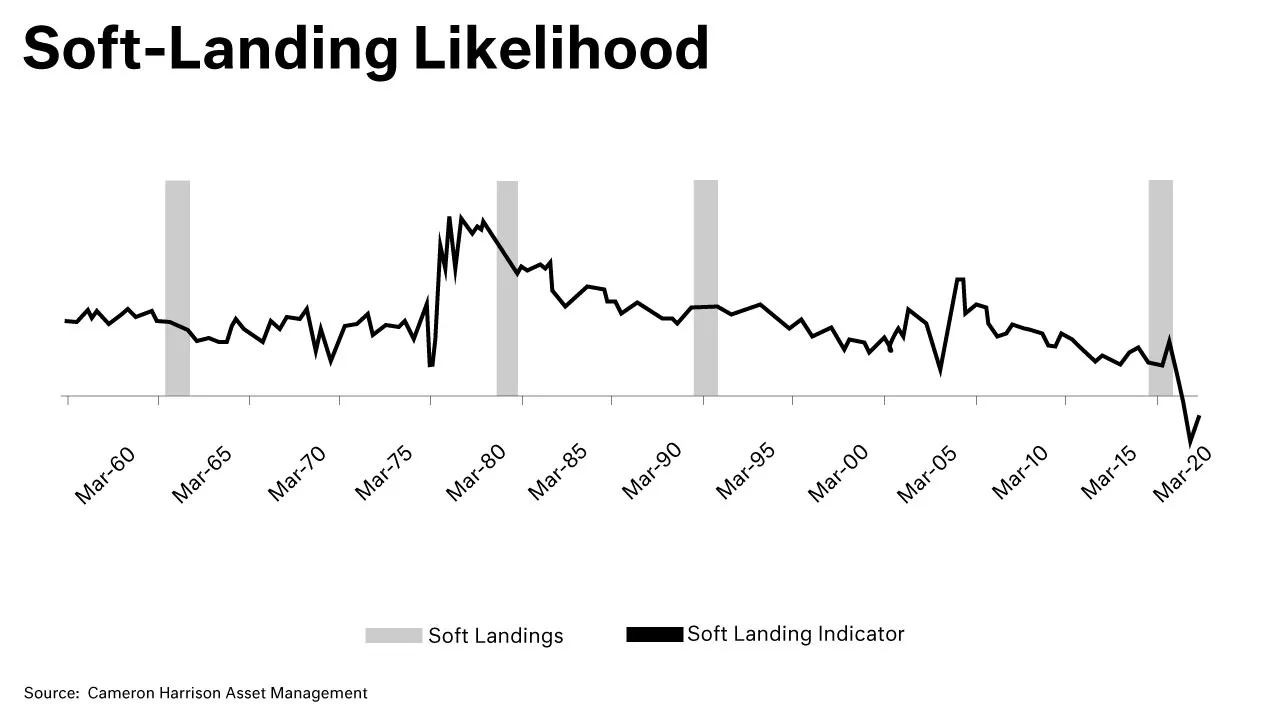

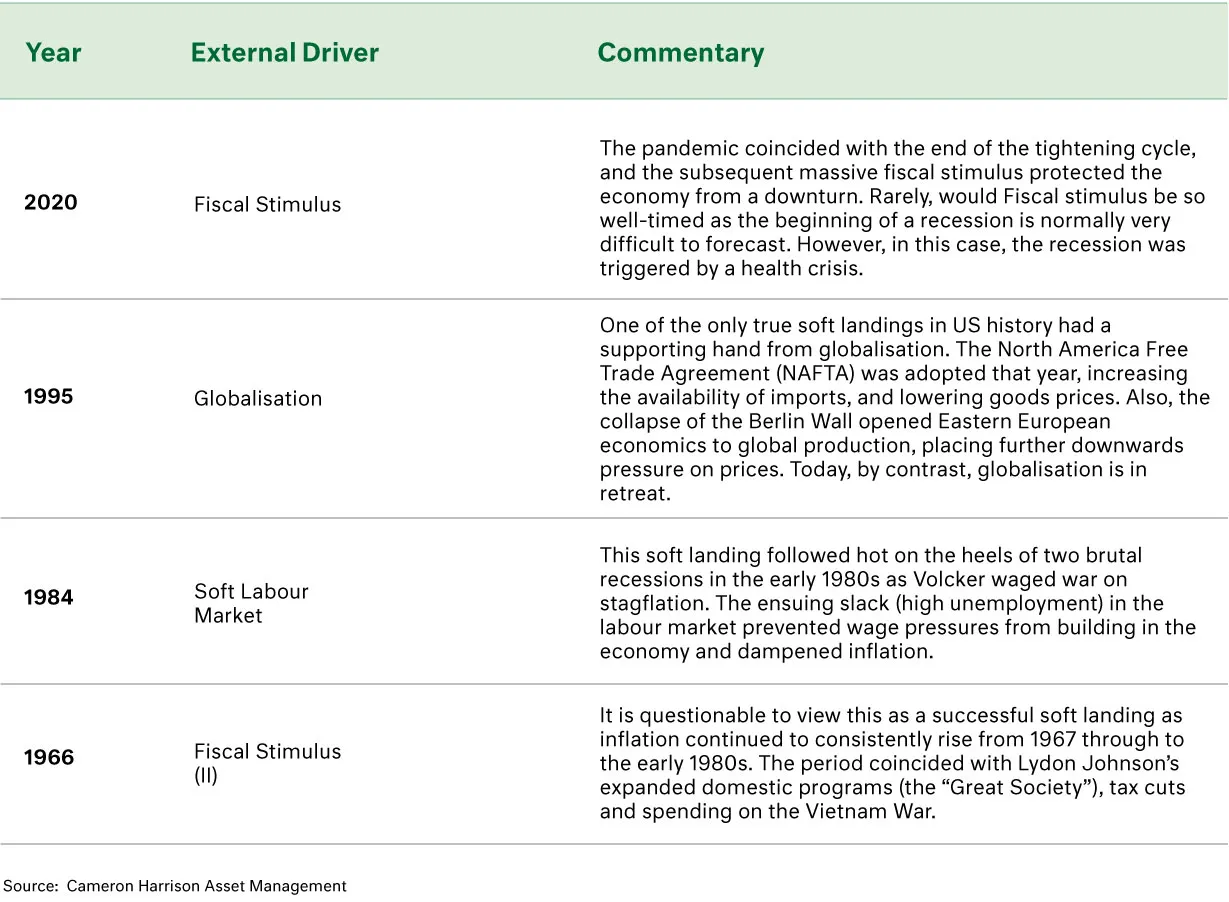

Looking at history, a soft landing is an exception rather than the rule, with only 4 of the last 11 rate hike cycles avoiding an eventual recession. Taking each of the four successful soft landings in turn (in the table below), we see that they required both favourable macroeconomic conditions and a supporting hand from an external party.

Typically, a soft landing has tended to occur when: inflation was relatively low at the onset, unemployment was high (and didn’t rise significantly), and rate hikes were small to moderate in size. Intuitively this makes sense, a smaller inflation breakout requires less onerous monetary policy tightening, and higher slack in the employment market reduces services inflation pressures.

Using this information, we can establish a simple indicator of the likelihood of a soft landing based on the unemployment rate, the Fed Funds rate and the inflation rate. The higher the index the greater the chance of a soft landing. Based on this, the current macroeconomic conditions of very high inflation, a tight labour market and a starting position of ultra-low rates indicate that this is the lowest likelihood of a soft landing in history.

Further, the Fed has never successfully managed a soft landing when the unemployment rate has risen by more than 0.5%; we forecast that a 1-1.5% increase in unemployment is required to dull wage-driven inflation pressures. Overall, the current environment conditions point to a difficult environment to manage a soft landing by the Fed in the year ahead.

A recession in the United States in 2023 is the consensus view of the market, and probably the most widely anticipated recession in history. Does this mean that the downside is fully priced into markets?... Sadly, no.

The global market declines in 2022 are due to falls in the price-multiple (PE ratio) for equities from their historically high starting point in January, as interest rates (and bond yields) have risen. The change in EPS has so far been inconsequential however, should a recession occur in the year ahead, history suggests that EPS would fall a further 20-30% at a minimum.

The potential fall in EPS would be mirrored by the S&P500 Index, given its high weighting to expensive growth/long-duration sectors (i.e. Tech).

This uncertainty however, is creating opportunities in other parts of the market. We favour a balanced approach between defensive investments in Staples and Healthcare, with an allocation to well-managed, industrial companies at favourable valuations that can benefit in the decade ahead in a higher inflation, higher interest rate, and higher fiscal spending environment.

Speak to one of our advisers to learn more:

david.clark@cameronharrison.com.au

Sourced from:

Photo by Unsplash