This article is a transcript of a webinar held by Cameron Harrison on 23th July 2020.

— Download the presentation here.

Over the medium term, COVID will eventually be addressed and managed - but probably not in a timeframe most hope for. Therefore, resolution will not be a smooth line but rather, messy, at times hopelessly uncoordinated, but with each step or misstep we learn a little more.

We note this not to dispel the significant short-term challenges ahead but to provide some realism to the medium-term path ahead. As for the magic bullet of a vaccine, we noted in our early May webinar on Investment and Economic Strategy Beyond COVID Suppression, our base case is that no effective vaccine is developed. Since then, our optimism has slightly improved but not sufficient for us to alter our base position. This means we need to live with this coronavirus and formulate effective, integrated policy which addresses and integrates economic, health and social policies.

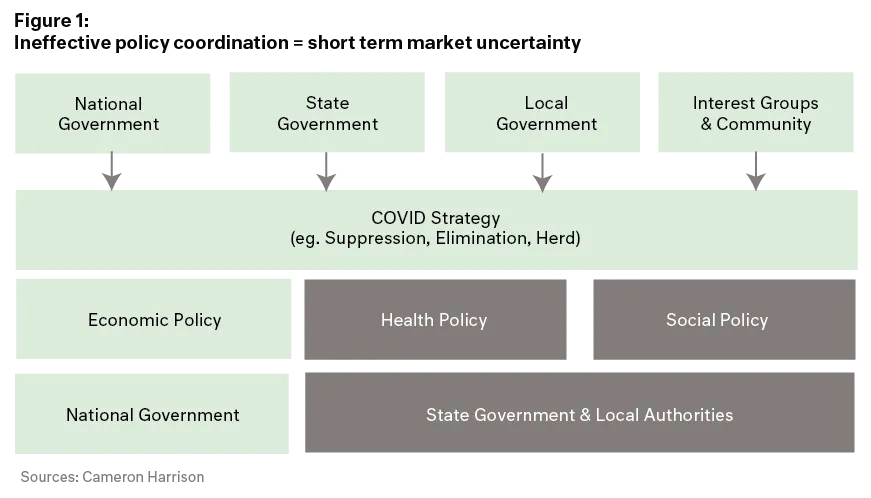

The ability of governments around the world and within individual countries to concurrently and effectively address pandemic responses across health, social and economic policies is proving to be problematic.

On the positive side, probably due to the experience of the GFC, leading western economies have responded impressively with their economic measures across monetary policy and fiscal policy. This demonstrates a learned policy response. We would contend that economic policy is easier to manage because the major levers of monetary policy and fiscal policy are controlled by a national government whereas to integrate health and social policy tends to be the responsibility of state and local governments. We see this strain playing out in Australia and the US and in contrast, is less evident in Sweden and Germany.