To hear David's thoughts, watch the interview below. A summary follows.

The Rate Cut Paradox

Investment Solutions |

Market Insights

A bullish sentiment continues to creep into the market. The story goes that GDP growth will fall enough to allow the central banks to cut rates, supporting current high valuations, and simultaneously, GDP growth will be high enough to enable strong corporate earnings per share growth (EPS). Clearly, these two scenarios are contradictory, a case of the Equity markets wanting to eat their cake and have it too, or as we refer to it, the rate cut paradox.

Posted 21 February 2024

Thus far in the tightening cycle, corporate earnings have surprised to the upside. This is in large part due to the savings buffer accumulated from government payments combined with the lack of spending options during lockdowns. The market is assuming that this situation will continue. Yet, there is much conjecture surrounding how much of these savings remain.

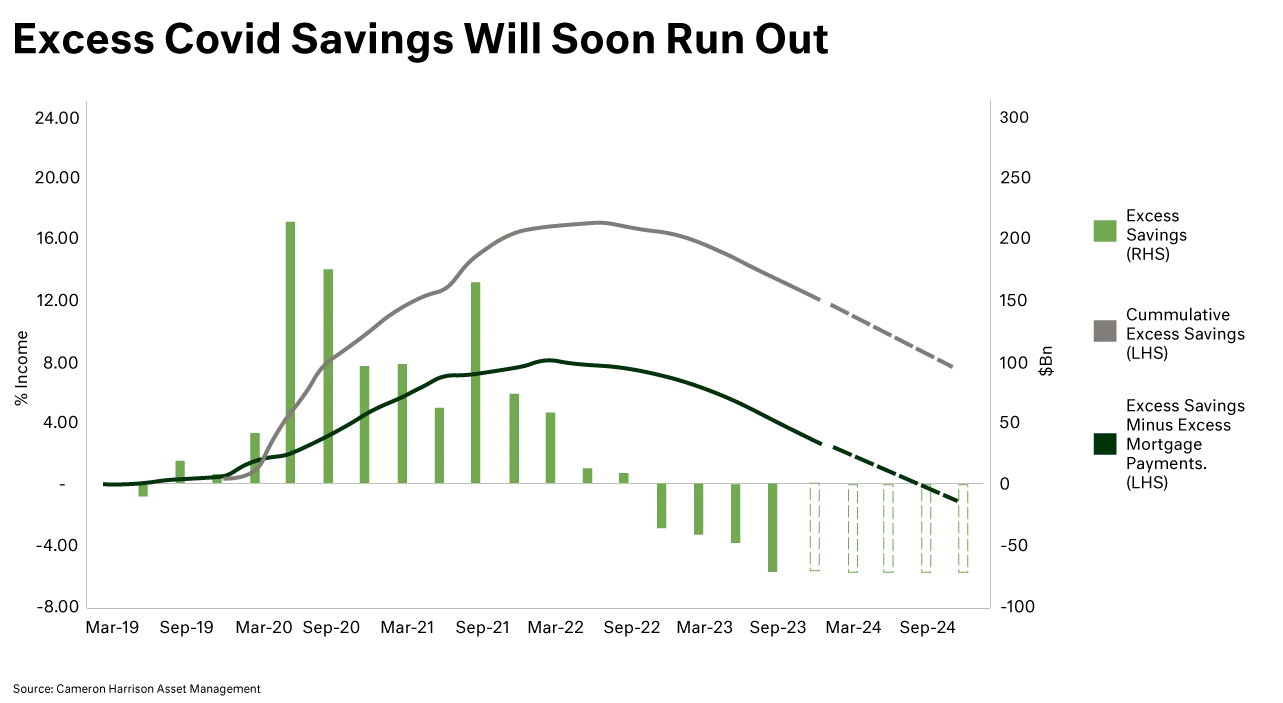

Looking at the chart below; at face value, the piggybank remains enormous (grey line) and could support another year of spending in the face of weak real income growth. However, much of the pandemic ‘cash splash’ was used to pay down mortgages. Accounting for this (green line) indicates this cash is due to run out in the middle of 2024. In our view, this will be a notable headwind for consumer spending and EPS.

The second assumption is that Central Banks will switch to a loosening stance as inflation inflects, to preserve economic activity. We believe this is optimistic and ignores the value hierarchy of central banks. The banks would certainly like to have economic growth, low unemployment, and price stability; however, when push comes to shove, they will always choose price stability, even if it means sacrificing economic growth.

Rather than Central Bankers perfectly timing rate cuts to support consumer spending in the economy and drive down long-term rates, we think it is just as likely they will resist cutting rates until convinced beyond reasonable doubt that inflation has been slayed.

In our view, prevailing valuations and earnings projections are pricing in a ~90% chance of a soft landing in 2024. However, we see the likelihood of this scenario as evenly split, a 50/50 chance.

If a soft landing does materialise, we anticipate potential gains in sectors like reasonably valued industrials and non-cyclicals. Conversely, in the event of a hard landing, those companies with higher valuations and greater earnings growth expectations, notably the Magnificent 7 (Apple, Amazon, Meta, Alphabet, Microsoft, Nvidia, Tesla), are likely to be most affected.

Our overall stance is to maintain a conservative allocation in equities, at the bottom of our strategic range, with a preference for more secure, interest-bearing investments.

Speak to one of our advisers to learn more:

david.clark@cameronharrison.com.au

Sourced from:

Photo by iStock