The proposition is that without a return to a significant degree of social interaction and movement of people, economies cannot harness their fall and optimal capacity to produce goods and services and in turn, the equity markets abundant enthusiasm will have been misplaced To be sure, I think this is less of an issue for Europe, the UK and US, but for Australia, we see real risks that the governments have failed to grasp and comprehend how to normalise movements between significant vaccination with commensurate adverse economic impacts, which both Gerard and I will touch on. We view the prospects for social interaction normalisation is significantly diverged between Australia and the increasingly vaccinated regions such as Europe, the UK and US.

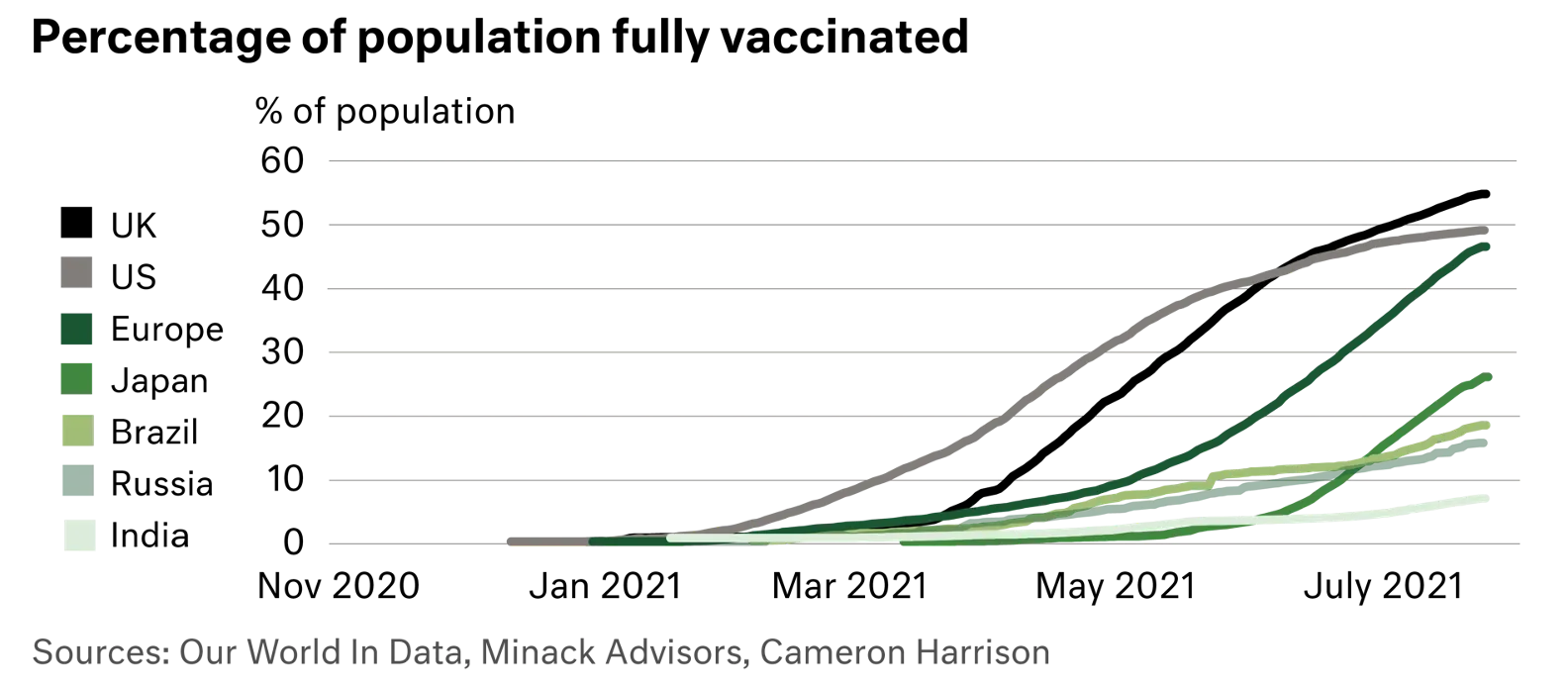

As matters stand, the UK provides the most optimistic path for developed economies and Australia, but we would be first to admit that the UK’s path for getting to this point was horrible and littered with policy blunders. In the UK, the adult population is now approximately 90% first dose vaccinated and 77% double dosed and 1-in-5 of the population estimated to have contracted COVID. Whilst herd immunity may no longer be possible nor the objective, such levels of vaccination and antibody, based on the available data, provides the necessary combination of immunity and protection from serious illness and hospitalisation. This confronts the reality that once vaccination rates reach > 70%, the policy objective could move to substantially protecting the community. Vaccines are of course not complete protection from hospitalization, delivering a 90% to 93% efficacy rate. In the UK, that would leave 4 million double vaccinated adults susceptible out of 41 million, but sensible mitigation such as booster shots, social distancing and masks substantially reduces this further. The difference in policy objectives of protection of community versus suppression to zero is stark. The economic outcomes even starker. Regions such as Europe, the UK and US have largely crossed the Rubicon into protection through vaccination. Australia is still firmly in the very small camp with New Zealand of suppression to zero.