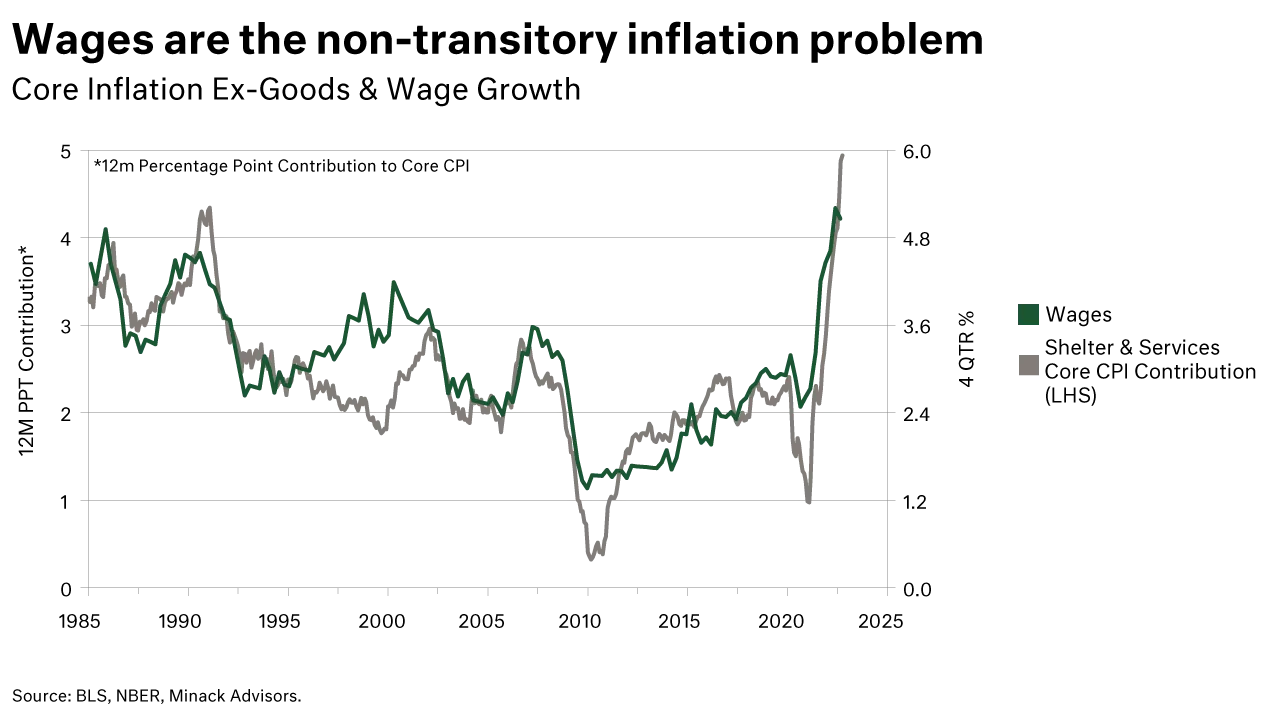

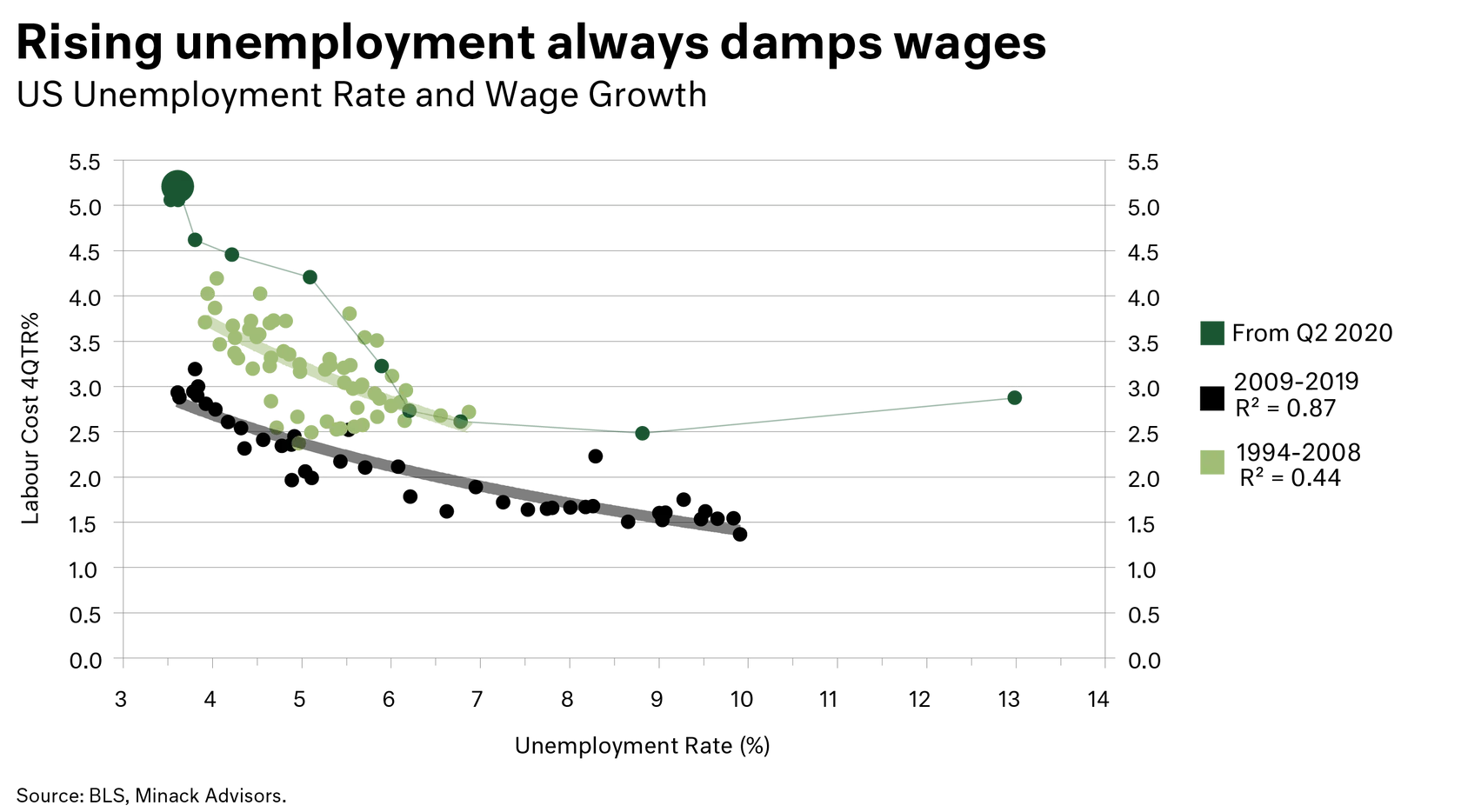

The US economy needs to generate unemployment of at least 1.5%, if not 2.0%, to generate a wage growth outcome of 3.5% to 4.0%, which would get the Fed moving down towards its target inflation zone. This matters because US Core CPI is being driven by shelter and services inflation. If goods inflation today were contributing zero to core CPI, then core CPI would still be 5% by virtue of Shelter and Services Inflation. In this respect, wage growth matters and getting to a satisfactory level will require higher unemployment.

To hear Paul's thoughts, watch the interview below. A summary follows.