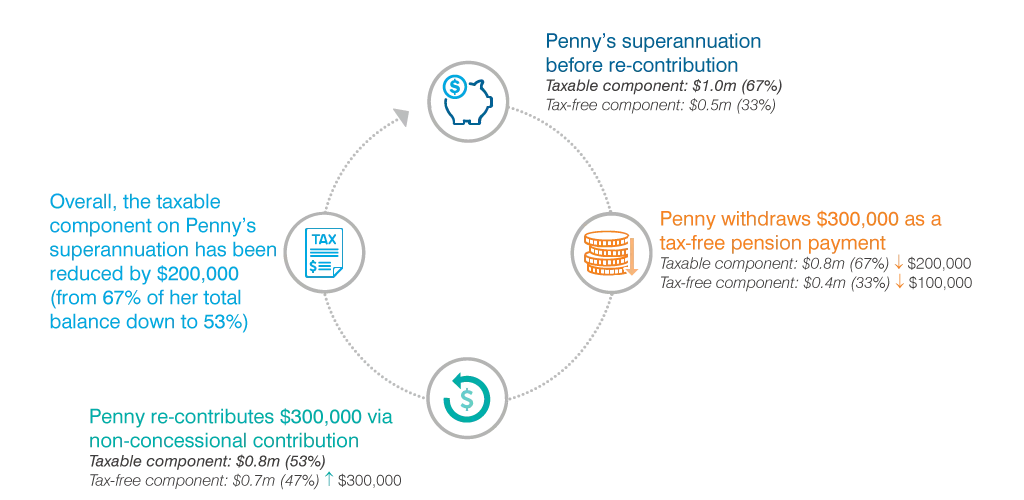

Penny is aged 62 years, a widow and has three adult children. She has superannuation of $1.5 million in an account-based pension and per her member statement, 33% of this sits within the tax-free component and 67% in the taxable component. Penny has in place a binding death benefit nomination in favour of her three children, equally.

On Penny’s passing (assuming no change in her final balance), the total taxable component at the time would amount to $1 million. As Penny’s beneficiaries are not tax dependants, the taxable component will give rise to tax of $170,000 (17%), reducing her death benefit from $1.5 million to $1.33 million.

What can Penny do now to improve the after-tax inheritance left for her children?

Following a review of her affairs and estate plan, Penny is advised to withdraw $300,000 from her pension and re-contribute the same amount back as a non-concessional contribution. In Penny’s case, this is permissible as she has an unrestricted pension and is under the age of 65 years; her withdrawal is also tax-free as she is above the age of 60 years.

The withdrawal of $300,000 is taken proportionally from both the taxable and tax-free components that is $200,000 from the taxable component and $100,000 from the tax-free component. However, non-concessional contributions are always treated as an increment to the tax-free component, therefore the contribution itself will increase her tax-free component by $300,000.

On a net basis, the re-contribution will have the effect of reducing Penny’s taxable component by $200,000 or 53% of her total balance (down from 67%), as illustrated below: