This article is a transcript of a webinar held by Cameron Harrison on 27th May 2020.

— Watch the recorded session here.

— Download the presentation here.

Fixed Income Strategy: Demystifying Bonds & Fixed Income Strategy Moving Forward

We navigate with analysis, combined with 50 years of balance of risks perspective. It ensures we see the woods from the trees.

Posted 27 May 2020

Yields, Back to Basic

Going back to basics for a second, the yield of a bond is the annual coupon or interest payments as a percentage of the price of a bond. If a bond pays a coupon of $3 per annum and it costs $100 to buy the bond, then the yield is 3%.

In simple terms, the yield is set by the market with reference to a number of economic and market factors. If the yield goes down, the capital price goes up. Conversely, if the yield goes up, the capital price goes down. This is important because it highlights that the value of fixed income assets move up and down every day like other securities, and that there is some volatility though no-where near the levels of equity volatility.

For Cameron Harrison, we purchase for a total yield on acquisition, not for capital gains during our holding period. Accordingly, we operate a hold to maturity strategy subject to the ongoing suitability of the issuer. We do this by managing our assessment of the yield curve.

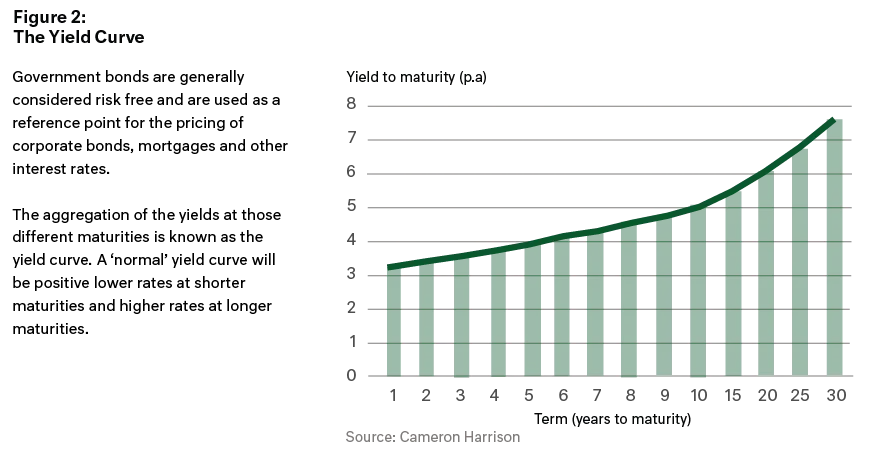

What is the yield curve?

A Yield Curve represents interest rates on debt for a range of maturities from overnight cash through to 30-year bonds. The yield curve shows the yield an investor can expect to earn if they lend money for a given period of time for a constant level of risk. Figure 2 below displays a bond’s yield on the vertical axis and the time to maturity across the horizontal axis.

Ultimately the yield curve will determine the compensation for taking a longer exposure to debt and whether you wish to invest in a fixed rate of interest or a floating rate. This is driven by inflation and inflationary expectations.

The factors that impact short-term rates and longer-term interest rates and therefore the shape of the yield curve are:

First, Macroeconomic forces (demand):

‒ Economic prospects

‒ Volatility

‒ Asset allocation movements

Second, Fiscal policy (supply):

‒ Government raising debt

‒ Increased / decreased supply of bonds due to budget deficit / surplus position

Third, Monetary policy:

‒ Short term interest rates RBA Cash Rate

‒ Quantitative easing: central banks buying bonds on market

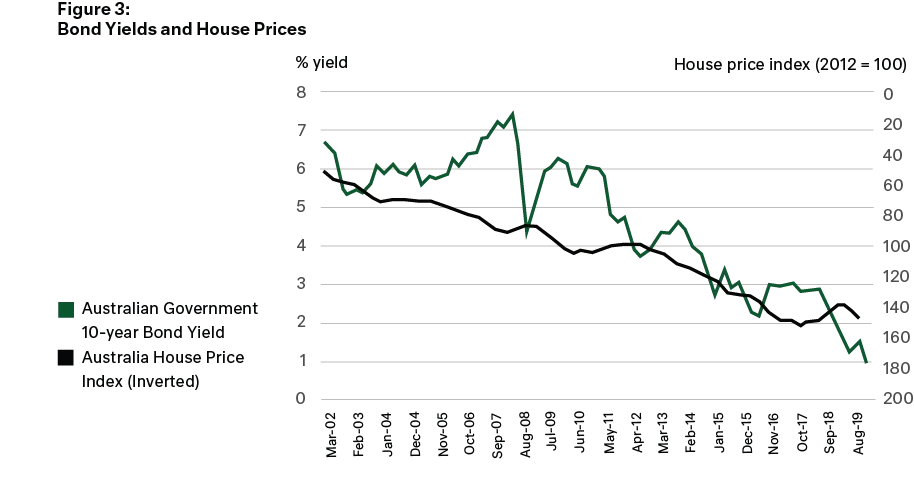

Asset prices and yields are inversely related. If the price of an asset increases, the yield decreases. Likewise, if the cost of funding decreases the price of an asset will increase, all things being equal.

Taking residential property as an example, the correlation between bond yields and house prices over the past 20 years has been very strong. As bond yields decrease, so does the cost of debt. The cheaper the debt, the more debt a household can take on. This all flows into higher property prices.

Likewise, when bond yields increase, it can be expected that asset prices will decrease unless there are increased earnings to support the higher yield demanded.

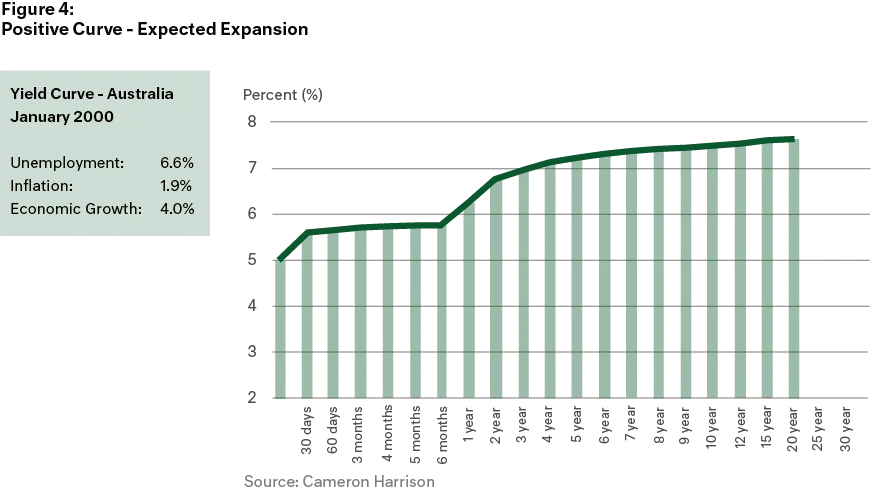

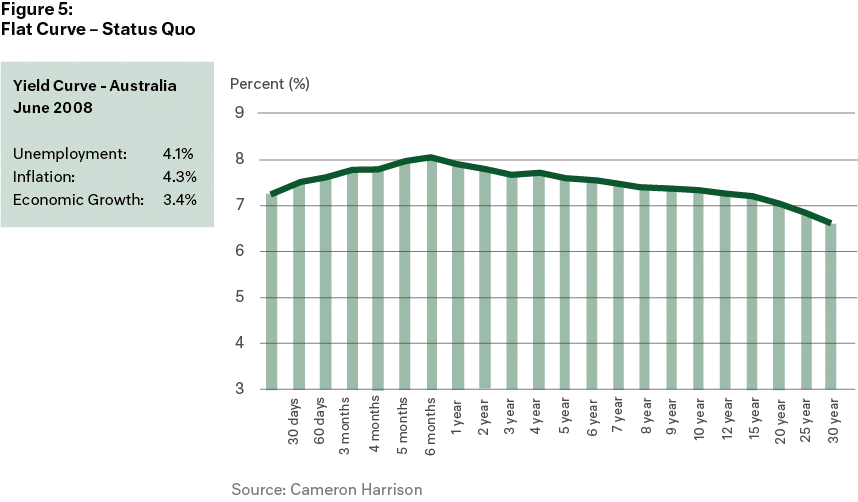

Figure 5, 6 and 7 below show how yield curves can look like based on different economic outlooks. We use historical Australian Government yield curves as an illustration, so we can relate with those past economic environments.

In general, there are three types of yield curves.

Interest rates are expected to increase

The general expectation is that future economic growth (and inflation) will be higher than the current environment. In 2000, the economy was starting to build momentum following a mixed decade of growth in the 1990’s. We can see higher unemployment at 6.6% but it was improving, productivity was increasing, and importantly some inflation was present but well-contained. At the time it was described as a ‘goldilocks’ period.

Interest rates are expected to remain the same

June 2008 witnessed the half-way mark of the global financial crisis, with Lehmann Brothers collapsing shortly thereafter. Despite the turmoil occurring in Europe and the US, the local economy was buoyed by then-record iron ore prices.

This left the RBA cash rate at 7.25% with bond yields across the spectrum of maturities being fairly consistent – an indication of the uncertainty at the time.

Economic Environment:

‒ Relatively high short-end rates

‒ High iron ore prices generating national income boost for Australia

‒ Asset prices elevated

‒ Low unemployment, capacity constrained

‒ Heated economy with inflation risk

Interest rates are expected to decline

1990 saw the recession we “had to have” and locally we saw extremely high short-end rates at around 17%. The market, quite rightly, saw this as unsustainable and priced in several rate cuts.

Inverted yield curves are particularly troublesome for banks as they borrow at short-end rates and lend at long-end rates, reducing net interest margins. At the same time, ANZ and Westpac were on the verge of collapse.

Economic Environment:

‒ Excessive money supply growth post 87 stock market crash

‒ Financial deregulation unleashed irresponsible credit growth

‒ Inflation expectations had become unhinged and govt couldn’t manage high inflation

‒ High short-end interest rates

‒ The ‘recession we had to have’

Interest rates ...get down

Figure 7 (below) is our current yield curve in Australia compared to earlier in the year.

It is behaving normally for where the economic cycle is – unfortunately, that is with economic activity at unparalleled lows. We need to go back to the end of WW2 when war production ceased for something comparable. Whilst today's circumstances are very different to 1945, the comparisons with how economies dealt with the ‘hangover’ effects of war spending and deficits are quite illustrative of where we find ourselves now and moving forward and more specifically where we see the path for interest rates over the next 3 years and then beyond.

On Figure 8, we can see that we approach the future pursuit of economic growth, modest inflation and an eventual reduction in debt from a very awkward position. With both short-term and long-term interest rates at below 1%, traditional interest rate-setting policy tools are exhausted leaving novel, new policy tools which potentially represent a seismic change for fixed income investment.

In Australia:

‒ Likely to remain at 0.25%

‒ Low risk of negative interest rates

‒ Support households given high household debt

‒ Remain very low going into 2022

‒ This is traditional policy, setting interest rates in support of the inflation target of 2% to 3% pa

In the US:

‒ To remain at 0.25%

‒ Very similar settings to Australia with traditional policy objectives, but clear policy now in place to provide short term liquidity to the short-term commercial debt paper market

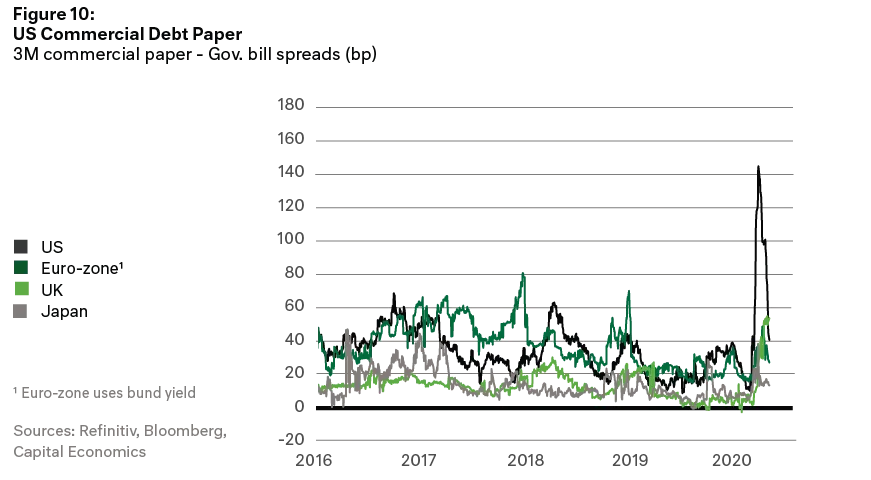

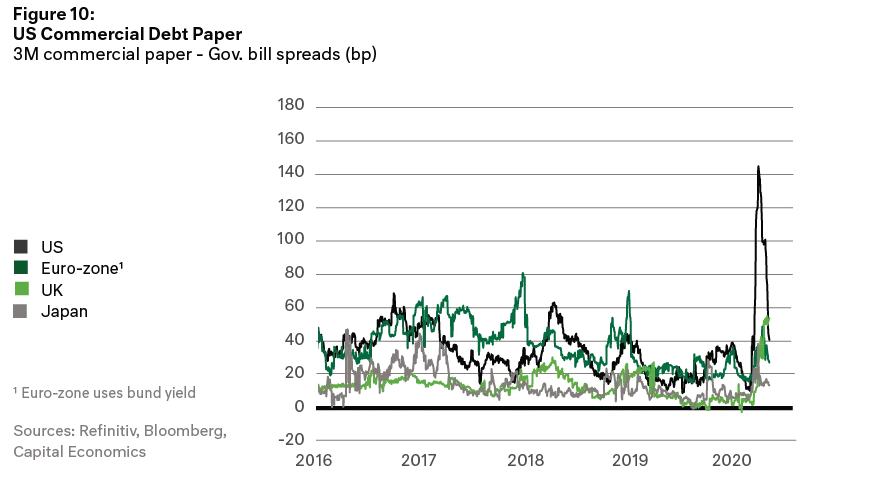

In the US, the Federal Reserve has employed some significant unorthodox liquidity tools which demonstrate Jerome Powell’s stated commitment that they will act ‘forcefully’ and decisively to ensure the key cogs and wheels of the US economy remain greased and operational. It is equivalent to ‘do whatever it takes’. Here we see the short-term commercial debt paper market. In early April it went into a liquidity meltdown and basically failed to operate and this was reflected in sky-rocketing margins. The Fed very rapidly intervened to provide the necessary liquidity through direct action and ongoing targeted short-term funding programs. The result is normality has returned to this funding market.

I raise this commercial paper example because it highlights a new and evolving role for central banks in addition to just conducting monetary policy through the setting interest rates – and that is back-stop funding of markets and ensuring overall liquidity if and when required. In the short term this provides a lot of confidence to money & bond markets that the Fed will be there. In the medium term however, there is risk of abuse by market participants.

US commercial debt paper

‒ Federal Reserve back-stopped the commercial paper market

‒ Central banks enlarging role as the banker of last resort

‒ In the medium term this risks ‘gamed’ behaviour which delivered us the GFC, but…

‒ in the short run provides confidence and substantial $ floor

Turning to longer-term interest rates, we expect long term rates might edge lower but otherwise will be flat over the next 2 years. Beyond 2 years we see: Low for a very long time

‒ Significant government debt has been accumulated, with more to come

‒ Currently low and in short term might edge lower, but otherwise flat next 2 years

‒ Level of fiscal stimulus will be important to longer-term rates with significantly more debt otherwise pressuring rates upwards

‒ Higher rates would be counter-productive to economic growth and some inflation

‒ So what to do …

Against the debt pile backdrop, is the concept of financial repression.

The act of financial repression is where rates are set by the government and monetary policy. Financial suppression would see both short-term and long-term rates suppressed by policy as the world economy attempts to reflate to healthy economic growth, lower unemployment and acceptable levels of inflation. This would take us back to the post WW2 era where huge war time debt had accumulated to finance the war effort. US bond rates were suppressed from 1945 to the late 1960’s (shown in Figure 12 below).

In Australia at present, the RBA is suppressing bond rates up to 3 years maturity at 0.25%. The trick is to generate sufficient inflation (but not too much!) such that as GDP grows with debt remaining constant and over time the debt to GDP % gets smaller. For this to work, interest rates must remain low for the next 15 years. So it was after 1945 and most likely, so it will need to be for the next 15 years.

For bond investors, this likely provides low nominal yields and probably negative yields adjusted for future inflation. For Fixed Income with longer duration (being fixed interest for longer maturity periods) this increasingly looks like an average deal over the next 2 years and a bad deal beyond early 2023.

Subject to sensible, strategic fiscal stimulus, the broader implications for equities, property and commodities would over time be broadly supportive.

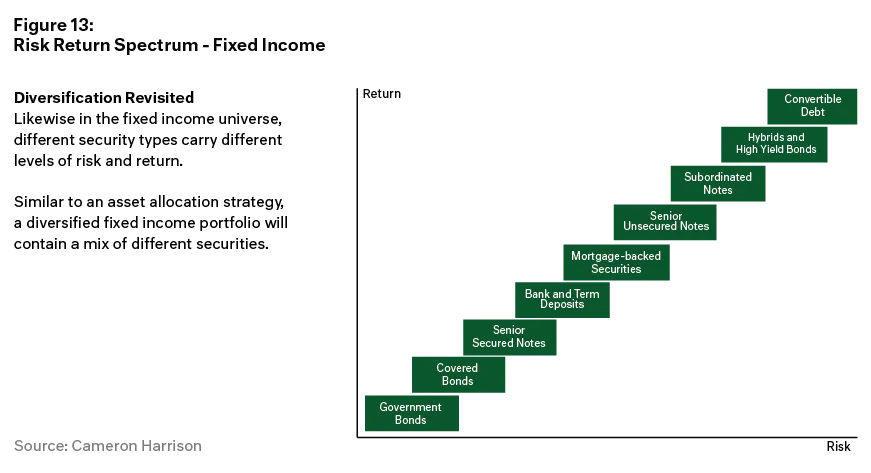

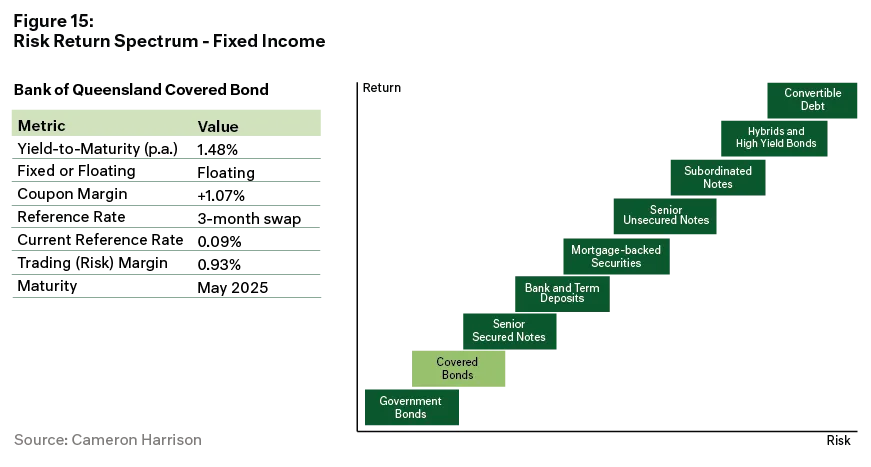

As we know, asset classes have different levels of risk and return, and likewise so do fixed income assets. We can see this in the diagram in Figure 13 below. At the lower end of the risk spectrum are government bonds and at the higher end are equities.

Depending on an investors risk tolerance, specifically volatility and the likelihood of positive and negative returns, they will adopt a blend of these asset classes to create a diversified portfolio to mitigate concentration risk – that is, being too heavily exposed to one asset class.

In the Cameron Harrison Interest-Bearing strategies, we operate to an objective return outcome which is the 3-year Commonwealth Bond rate + 2% pa. Accordingly, you can think of this objective as an optimising return objective not a maximising return objective. Fundamentally, it is to provide an appropriate level of income yield with low risk to capital.

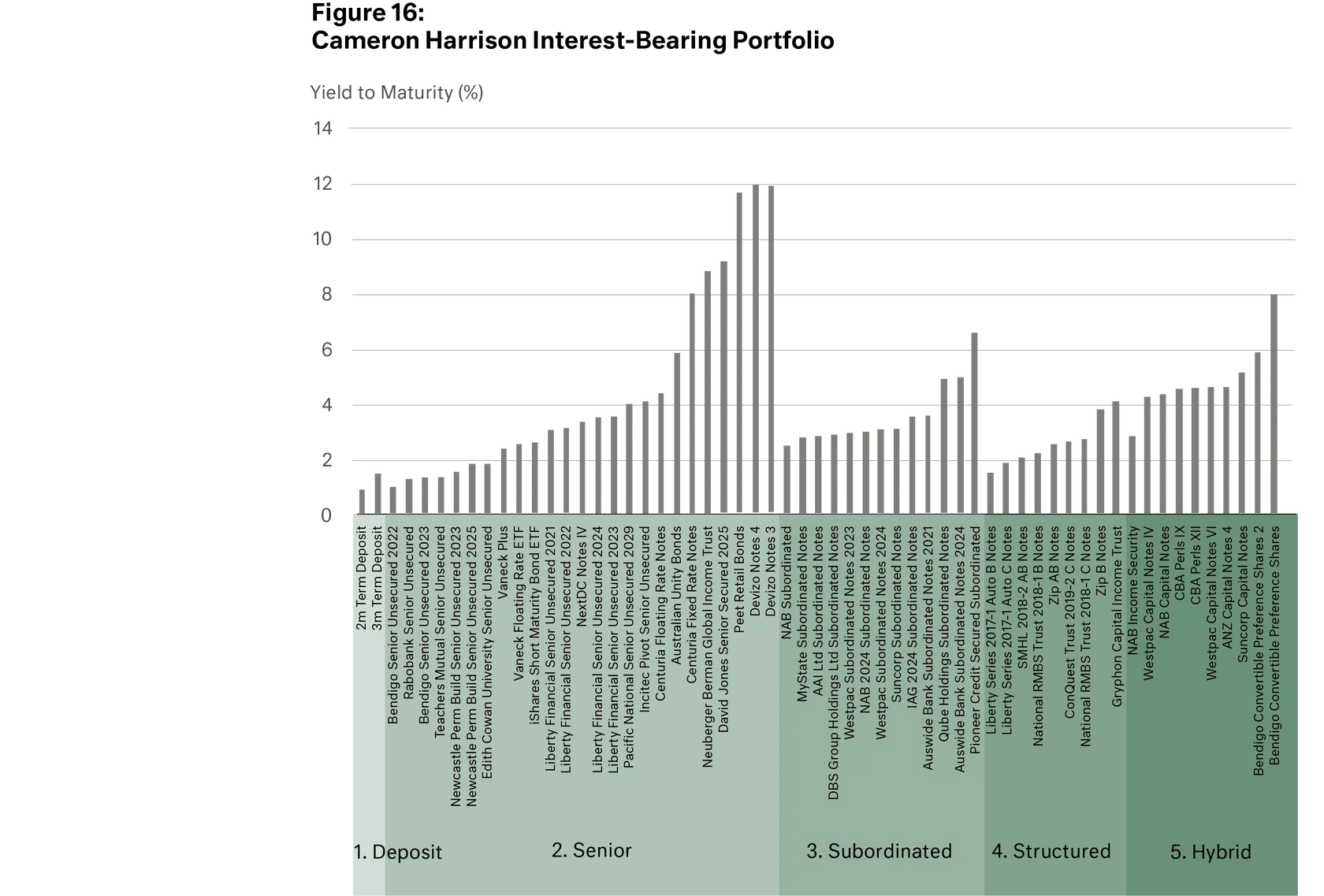

The management and achievement of appropriate income with low risk to capital are delivered through a highly diversified portfolio of securities; from government guaranteed securities, to senior secured notes, hybrids and some higher-yielding bonds. The result is a strategy which reflects our strategic settings, risk parameters and of course, return objective with capital stability.

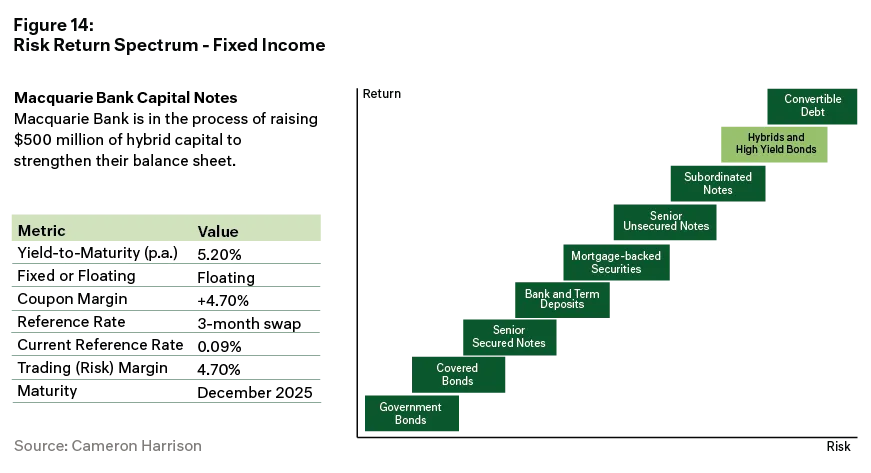

Example 1 – Hybrids

Macquarie Bank Note

We have last week added a Hybrid Security issued by Macquarie Bank, part of the Macquarie Group. The hybrid name refers to the security having elements of debt, being fixed interest payments, and equity as the notes can convert to equity if the regulators intervene to strengthen the bank’s balance sheet.

The coupon paid reflects current market pricing for hybrid securities – it pays a floating coupon of +4.70% above 3-month swap rates – a level of compensation which we view as appropriate for the level of risk. The trading margin will fluctuate through the life of the note as the risk premium demanded by investors will change to reflect the market and economic environment.

These securities are rated by Moody’s as the equivalent of BBB- and the trading margin is appropriate for that rating.

Example 2 – Covered Bonds

Bank of Queensland Covered Bond

At the lower end of the risk spectrum sit Covered Bonds. These bonds are secured by specific mortgage collateral relating to loans issued by the bank and are therefore viewed as very secure.

In our Wholesale strategy we have recently added a covered bond issued by the Bank of Queensland, secured by a pool of mortgages and therefore the property that those mortgages are secured against. Like Australian government bonds these are AAA-rated and sit at the low end of the risk spectrum.

The coupon paid reflects the lower risk of the bond – it pays a floating coupon of +1.07% above 3-month swap rates.

Highly diversified portfolio across:

‒ Borrowers/issuers

‒ Security type

‒ Holding and issuer limits

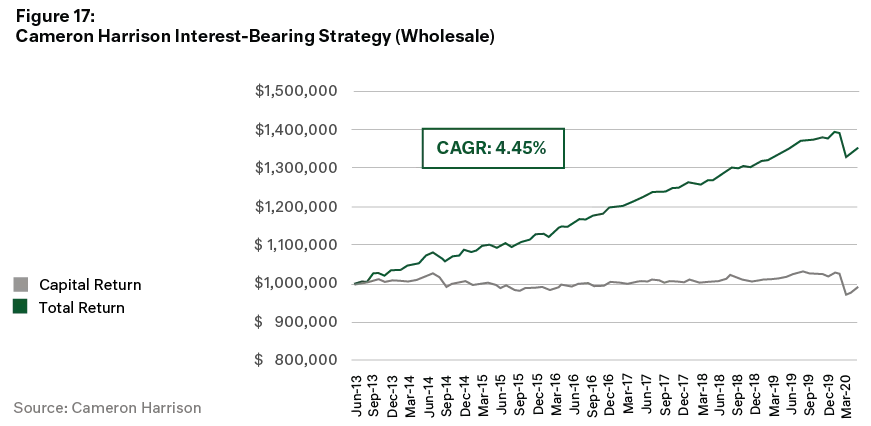

Objective:

‒ To produce stable cashflow with modest capital growth – income strategy

‒ Benchmark currently 2.54% pa

Key settings:

‒ Weighted maturity of 3.3 years

‒ Duration of <1

‒ Weighted yield to maturity

‒ Floating rate 78%/ fixed rate 22%

‒ Poor outlook for sovereign government debt

Interest-Bearing Strategy achieving stability of income and capital, even with most recent market volatility

Generated return of 4.45% pa from July 2013 to May 2020 – the benchmark return for this period was 4.05% pa

Cameron Harrison have been advising business owners and their families on asset allocation and intergenerational wealth management for over 50 years. We have demonstrated over a long period our ability to manage investments through both the good times and bad by keeping the client at the centre of our business.

For more information on our approach to investment strategy or any other inquiries, please contact us on +613 9655 5000.

Speak to one of our advisers to learn more:

paul.ashworth@cameronharrison.com.au