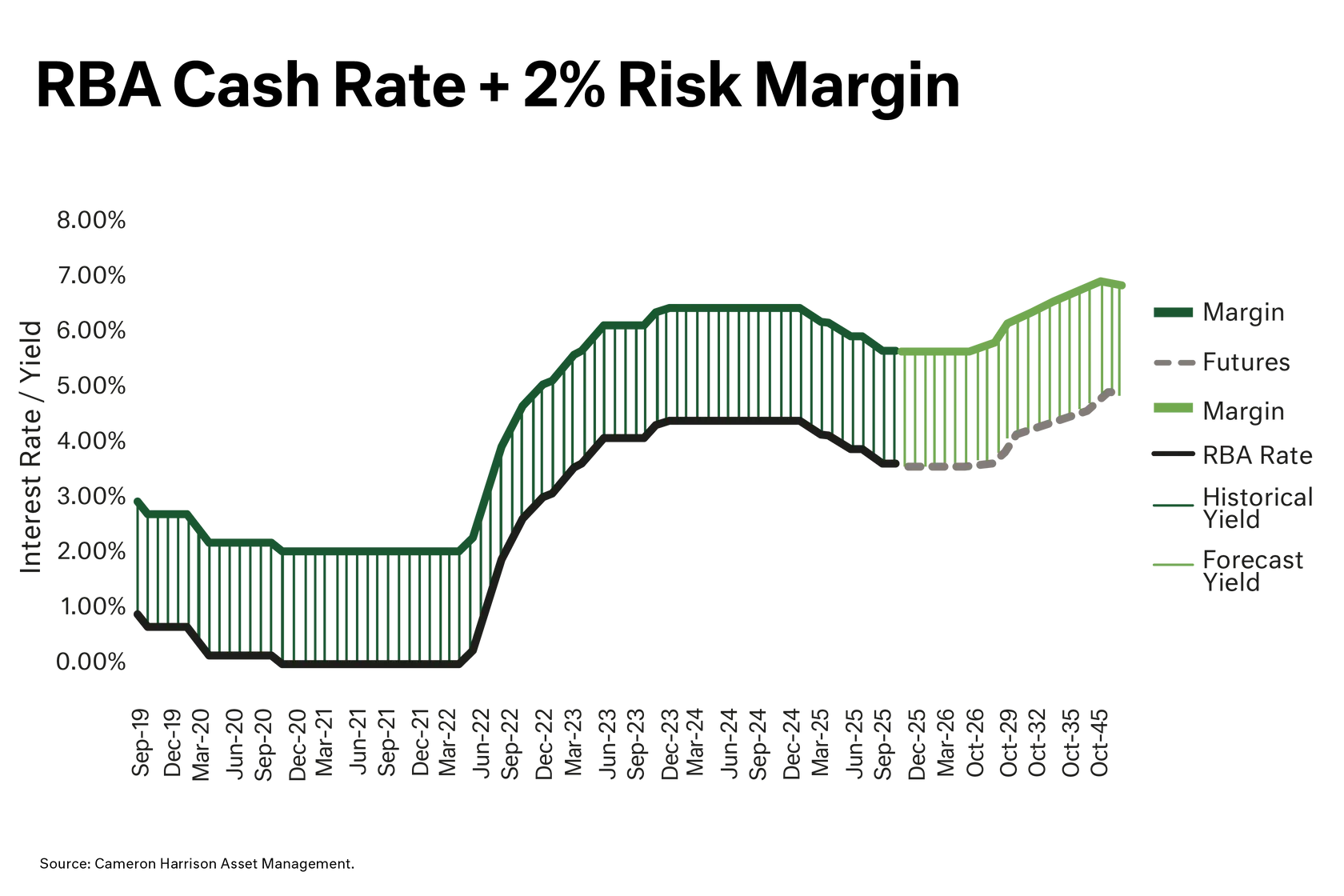

For unleveraged investors who derive an income stream from their capital, higher rates is a good thing. In essence, it means you can generate higher levels of income per unit of risk, meaning investors are less reliant on capital growth to generate appropriate returns to fund lifestyle expenses.

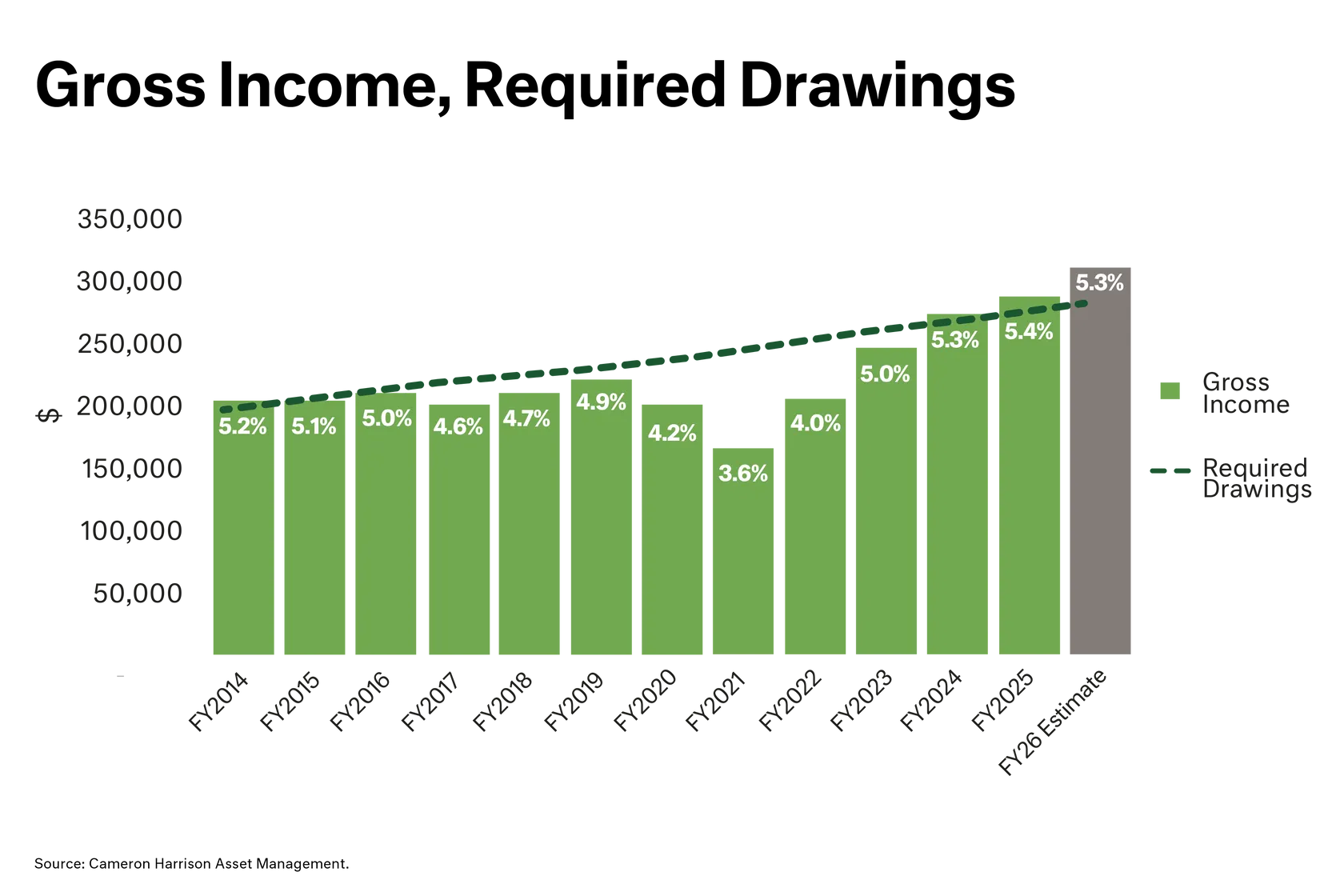

Take an investor who is retired with $4 million of superannuation to fund their lifestyle expenses which was $200,000 in 2014 and has been indexed by 3% each year. They have a moderate risk tolerance and seek to protect against the downside. The chart below shows income (cash flow) compared to drawings over a 10-year period. In FY2022 the market risk exposure was over 60%, today it is just over 50%.