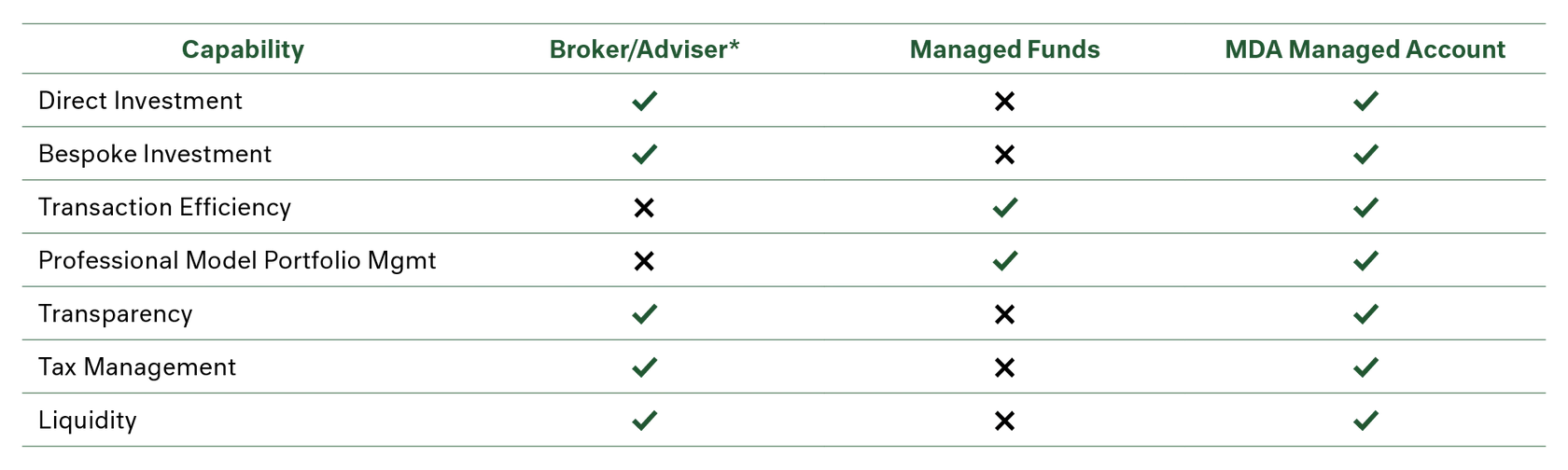

Portfolio investors in the US have had the benefit of managed, directly invested portfolios for well over 25 years. That is, clients have specific direct ownership of their underlying investments which are directed by a manager(s). The client receives a strategically planned portfolio, managed in real time, which is fully transparent as to holdings, trading, costs and performance.

In Australia, this form of portfolio management had been slower to take on, largely due to the embedded influence of bank and insurance company controlled financial planning and wealth management. The current Banking Royal Commission provides ample evidence of the banks' vested interest in not adopting more transparent and effective models like directly managed client portfolios. However, the good news is this is now changing quite rapidly.

As at December 2017, funds under management in managed accounts amounted to over $57bn of assets, a 45% increase on the 2016 figure. Whilst still a small part of the total investor pie, the rapid growth is a sign that investors are pivoting towards discretionary portfolio management.

Cameron Harrison and its partners have been at the forefront of directly managed client portfolios for over 25 years and are specifically licensed by ASIC to provide this service. We welcome its broader adoption in Australia as we consider it being vastly better for clients’ interests, especially when compared to the alternatives of financial planning platforms and broker commission trading.

Cameron Harrison operates directly invested and managed portfolios for its clients through its Complete Investment Solution and Complete Superannuation Solution, providing bespoke and professional portfolio management based on 25 years of experience managing client portfolios.