In Australia for example, we have been significantly focused on workforce growth through new arrivals. This we consider important in terms of easing labour supply pressure and moderating wage price pressure. It will in turn greatly assist in de-accelerating inflation and its expectations. But first, people need to get visas and then make their arrangements or coordinate with their college or university based on their start date. It is not a linear process. From here, it will still take a period of time before we see this additional labour flow through to easing wages growth, and in turn, reduced inflationary expectations.

De-accelerating Inflation is not a straight line process

Market Insights |

Investment Solutions

Noise about inflation measures from month to month, especially by news outlets and short-term markets, seeks a linear trend. Fair enough, straight lines are easier to understand and interpret and act on. De-accelerating inflation is however not a straight line process, but it will de-accelerate (albeit not to the sleepy and stubbornly benign levels for the 10 years after the GFC).

Posted 01 March 2023

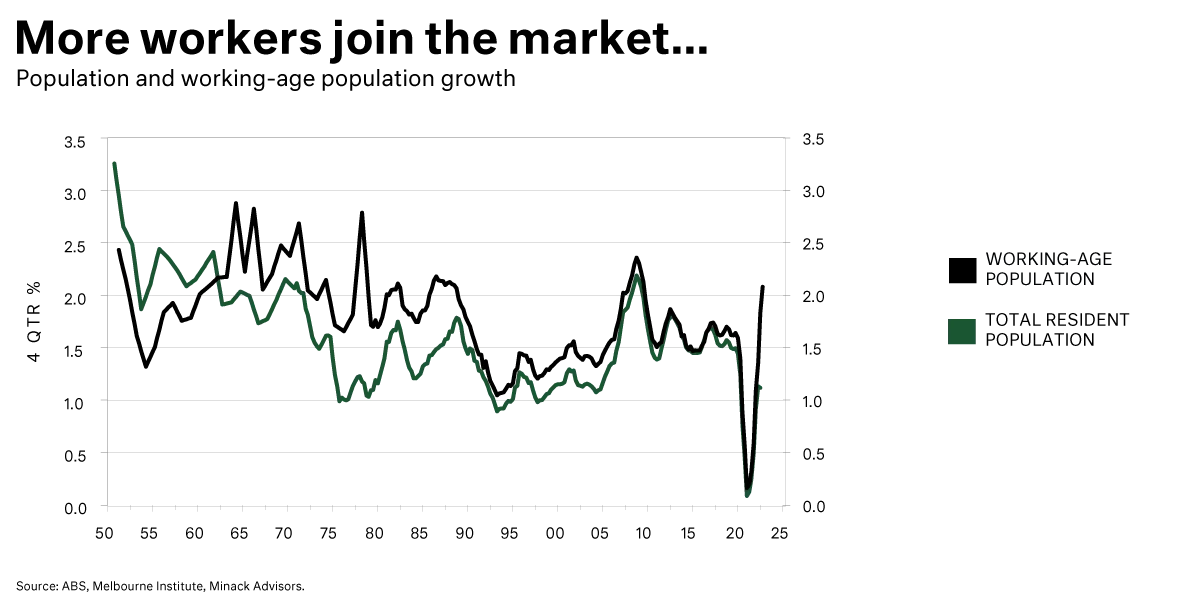

The addition to the workforce over the last 12 months is astonishing, as shown in the chart above, with over 2% overall growth or 270,000 people (and visa issuance well on foot). Over 18 months, this same data point is 455,000.

Just to underscore the non-linear implications of this growth in the workforce, whilst it might ease wages pressure, it potentially throws up housing pressure and the question of where will sustained population growth be housed given COVID construction curtailment and now tight financial conditions through restrictive interest rates.

We do see the path of de-acceleration of inflation in Australia and the US, but we certainly do not see it in a straight line course.

In Australia, we view the February retail sales figures as a key light on how fast the Australian economy is slowing. If weak, as we expect, then the path for interest rates may be somewhat more straightforward. In the US, we likewise see de-acceleration but without the clear capitulation of the consumer which looks more likely in Australia. The labour market in the US doesn’t have the benefit of supply growth like Australia, nor is household debt as restrictive to households.

So don’t confuse short-term noise with a linear path – you’ll be very disappointed and are likely to miss that the path to de-acceleration from restrictive monetary policy is far from linear.

Speak to one of our advisers to learn more:

paul.ashworth@cameronharrison.com.au

Sourced from:

Photo by Unsplash