To hear Paul's thoughts, watch the interview below. A summary follows.

Australia – the recession train has left the station… and the return journey doesn’t look too good either

Market Insights

Economic commentators have a (perverse) preoccupation with both the measure and reaching of a technical recession (i.e. two consecutive quarters of negative real GDP). For us, it’s the journey that is most important, for as recessions unfold, the damage and its velocity differ.

One central theme is that the household, as the master of consumption, is invariably the central victim; whether self-inflicted or not. Australia’s circumstances are further complicated this time around by resurgent population growth.

Posted 22 June 2023

If we compare the economy to a train, and the train driver suddenly brakes from 200 km/hr to 40 km/hr, then, for those inside, it will be harrowing and cause serious injury. In Australia’s current context, the RBA is the train driver, and the passengers are generally families with mortgages, rent and significant family living costs. Of course, not everyone is on the ‘train’ and this includes mortgage-free property owners who are typically near or post-retirement (with elevated income from higher interest rates on investments, albeit negative in real terms), and young adults with little or no accommodation obligations and adequate disposal income. For perspective though, 75% of households have a mortgage, and on average, this mortgage debt has increased in size by 46% to $280,000 per household since 2018.

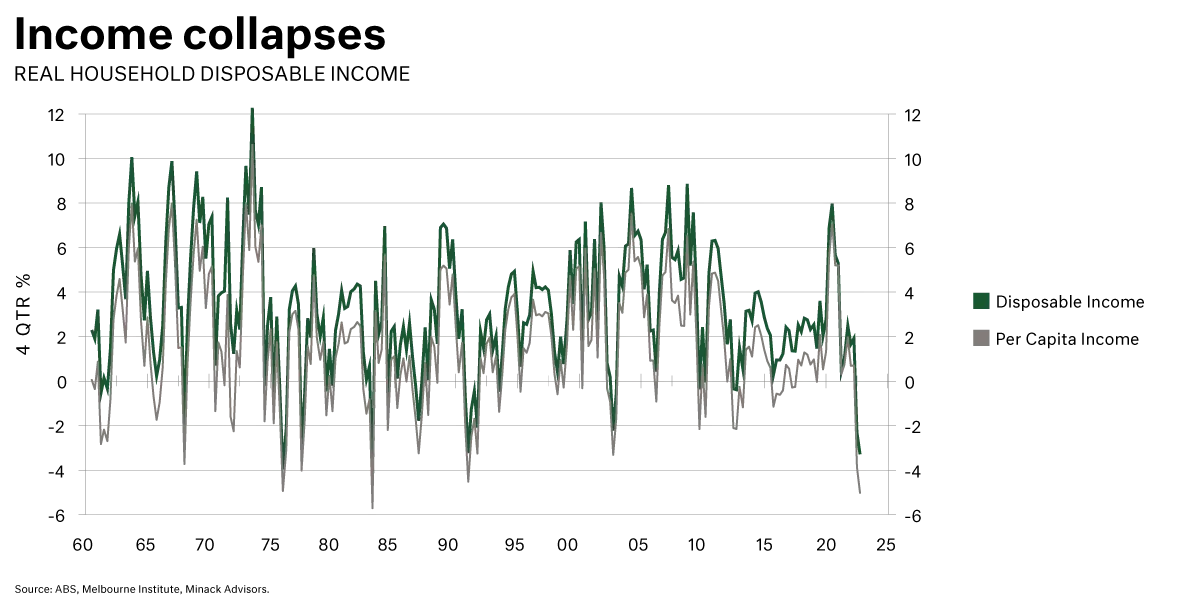

Households have just experienced their train suddenly going from 200 km/hr to 40 km/hr, and they are in awful shape. The household is facing a historic lowering in real household disposable income. We can see this in the graph below in the dark green line. Bad enough on an aggregate level, but the significant point we want to make, is on a per capita basis it is a real crisis – a recession. We see per capita real disposable income as negative growth in light grey, and it is at historically low levels when compared with the last 45 years. This is important for Australia in particular because as we will see shortly, the extent of real per capita disposable income is being driven by net migration, which will act as a medium to long-term suppressant of income growth.

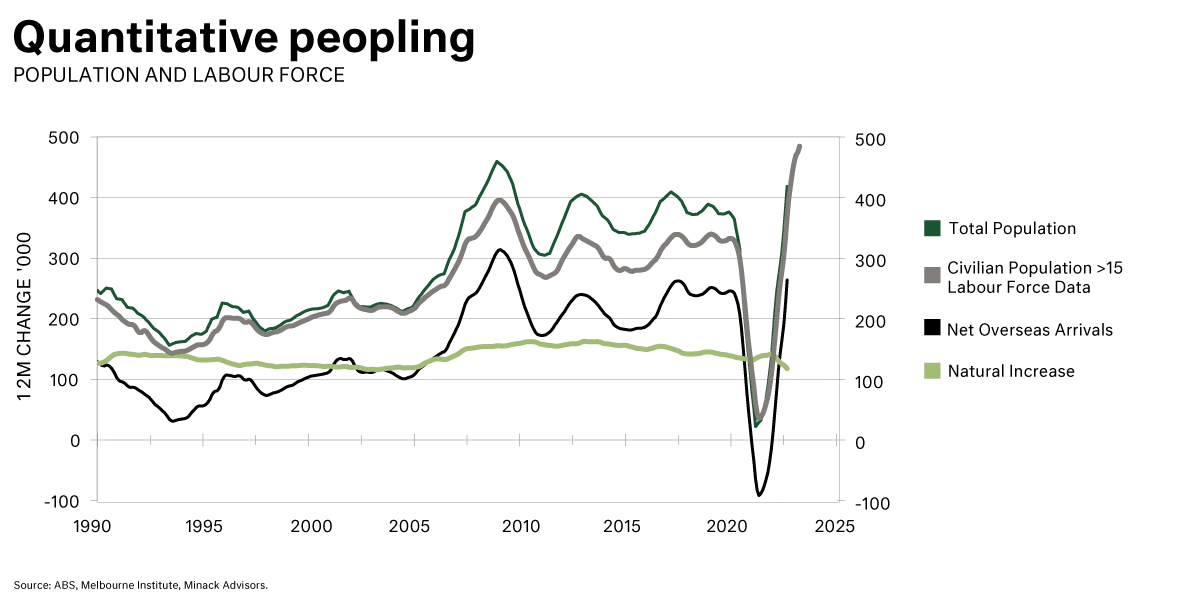

In our next graph we starkly see the extent of resurgent population growth. In particular, the stunning growth reversal in the working population greater than 15 years of age, shown in the grey line, is approaching 500,000 additions over the last 12 months. This directly relates to the labour force.

In the case of already dismal real disposable income, it makes it a whole lot worse on a per capita basis, and therefore in terms of standard of living. Importantly, the prospects for disposable income on an improvement in consumer inflation are muted at best. The key residual effect is a debt-financed household in a ‘zombie’-like state with no real income growth to meet inflated debt (off the back of elevated residential property prices).

Increased government tax receipts and various duties from the increased working age population underpins the new order of fiscal dominance – the government's position in the economy becomes more dominant

No or minimal real growth in disposable income – in the short to medium term, this will test the banking sector with mortgage rescheduling and restructuring. For households, it creates a dour medium-term outlook, and over time, a decline in living standards

Reliable, increased demand from the working-age population growth, supports non-discretionary spending (and the industrial logistics assets that support this sector) and healthcare

Poor productivity in Australia has little prospects for improvement, especially if policy direction and action is sought from Federal and State Governments. Over the medium term this supports strategically selected Australian equity exposure, and exposure to economies like the United States who have an outsized track-record compared to other G7 countries.

Speak to one of our advisers to learn more:

paul.ashworth@cameronharrison.com.au

Sourced from:

Photo by Unsplash