The substantial second round of Commonwealth Government stimulus completes the co-ordinated integration of monetary policy with fiscal policy. This is a historically important event which is being repeated in economies around the world. It represents a new chapter in economic policy and probably sees government and fiscal policy take the leading role going forward (having been dominated by monetary policy for the last 35 years). We will comment on this separately as it has implications for the post-crisis investment environment.

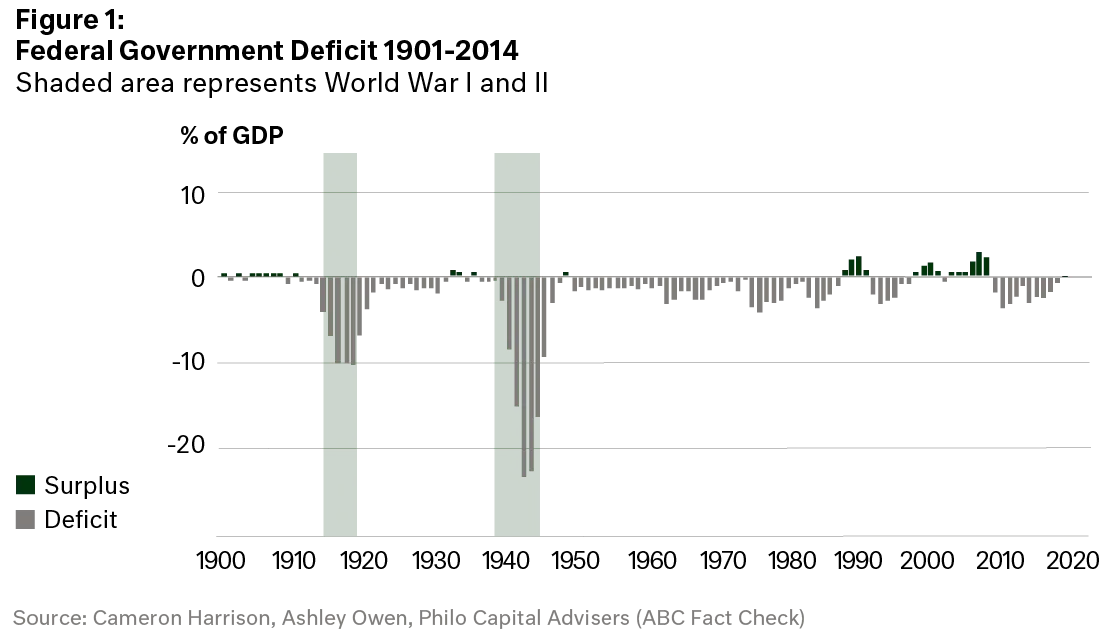

The ‘cratering’ of the economy might come to look like a World War, with government resources mobilised across all elements of the economy to address the enemy. Such is our modern world and economy, the efforts are not likely to be as long, but the short term severity much greater. Notwithstanding the short-term 'kitchen-and-sink' being thrown at COVID-19, and assuming reasonable community and business normalisation over the next six months, the duration and depth of fiscal stimulus should not get to the extreme lows of 1918 or 1943. We do see severe recession over the March, June and perhaps September quarters. As already noted, we see the fiscal stimulus over the next two years as needing to be substantially more than this 4.6% of GDP spend – a realistic figure with war time precedence is at least 10%, if not 15%.

The next stage of fiscal support we await is big business, particularly those most impacted by shutdown now and for a period of time – airlines, hotels, entertainment.

A potential silver-lining is the relatively fast response of policy makers compared to a ‘normal’ financial crisis. In a regular downturn or recession, the response of governments and central banks significantly lags the economic data, as they wait to see the severity of the issue before responding. In the case of COVID-19, the high-level health data has led the economic indicators, allowing stimulus to be deployed up to six months earlier than is typically the case. Make no mistake, the government's stimulus actions are significant and unparalleled in peace-time.