Amidst a global pandemic which threw jobs and industry into disarray, the last thing you would expect is for the average adult wage in Australia to experience its greatest biannual rise in almost a decade. Thanks to record stimulus and compositional changes in the workforce, the increase in the Average Weekly Ordinary Time Earnings (AWOTE) has triggered the indexation of superannuation contribution limits for superannuation.

Superannuation Contributions Indexation

Wealth Management Solutions

New superannuation contribution limits are coming. Taking advantage of the changes will enhance your retirement strategy.

Posted 02 June 2021

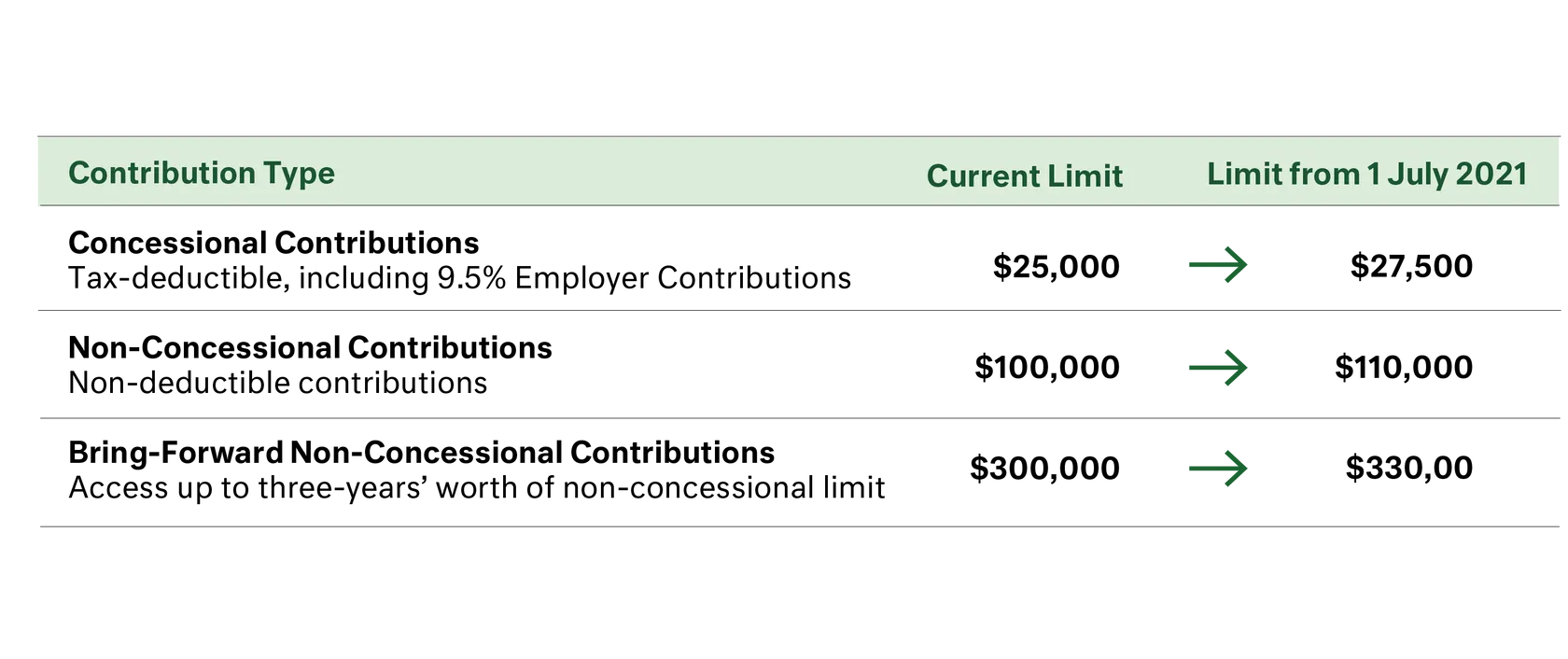

With the end of this financial year upon us and a new one soon to begin, a significant opportunity exists for eligible contributors to add up to $482,500 to superannuation over the next three months by straddling their contributions either side of 30 June.

It means that from 1 July 2021, the amount an eligible contributor may add to their superannuation account will increase:

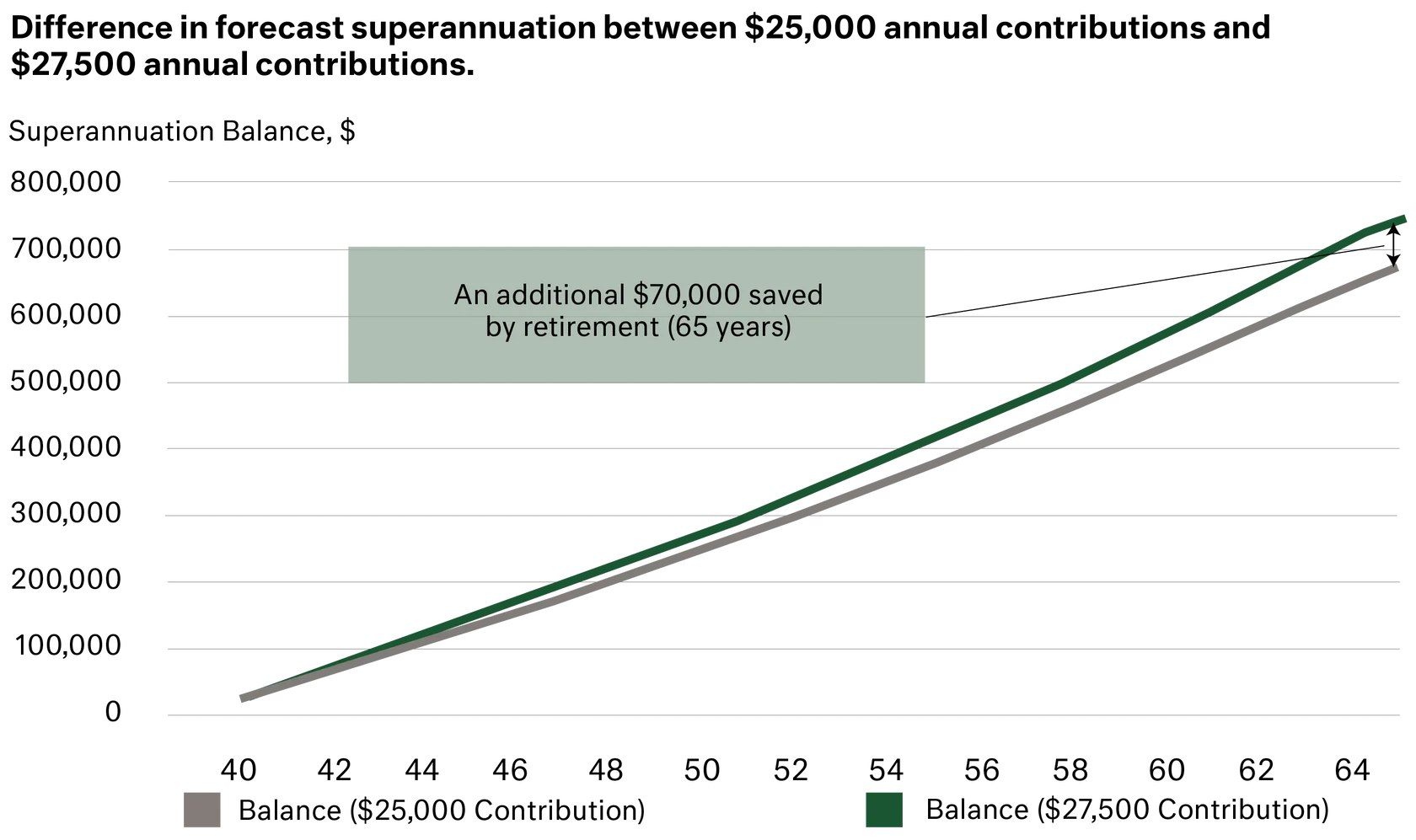

While the increases in the contribution limits might only seem slight, small differences add up over time. The power of compounding returns means greater opportunities to contribute can lead to significantly better capital accretion in retirement. The benefits are more pronounced the younger and further away from retirement you are. Take for example, a 40-year-old who has been ‘topping up’ contributions made by their employer to the concessional contribution limit each year. They can now ‘top up’ an extra $2,500 each year which could add $70,0001 to their retirement ‘nest egg’ by the time they reach age 65.

The above portfolio projection is based on long-term economic and return variables estimated by Cameron Harrison, based on Cameron Harrison’s Core investment strategy (50% ‘market risk’ exposure to Equities and Listed Property).

Estimated returns are not a guarantee or predictor of future returns and should not be relied upon as a basis of making current and future investment decisions.

Assumes capital growth is unrealised, and therefore not taxable.

To discuss your superannuation contribution or longer-term retirement plans, please contact us on +613 9655 5000.

Cameron Harrison have been advising business owners and their families on asset allocation and intergenerational wealth management for over 50 years. We have demonstrated over a long period our ability to manage investments through both the good times and bad by keeping the client at the centre of our business.

Speak to one of our advisers to learn more:

paul.ashworth@cameronharrison.com.au