At the beginning of the year, we warned of the increasingly aggressive foreign policy employed by China (Further reading: China Enters Adolescence). Rather than a more penitent China in the wake of the COVID-19 pandemic, we have instead seen a more assertive approach: extending sovereignty in Hong Kong, testing boundaries in the South-China Sea and imposing trade sanctions on countries it views as obstacles to its grand plan.

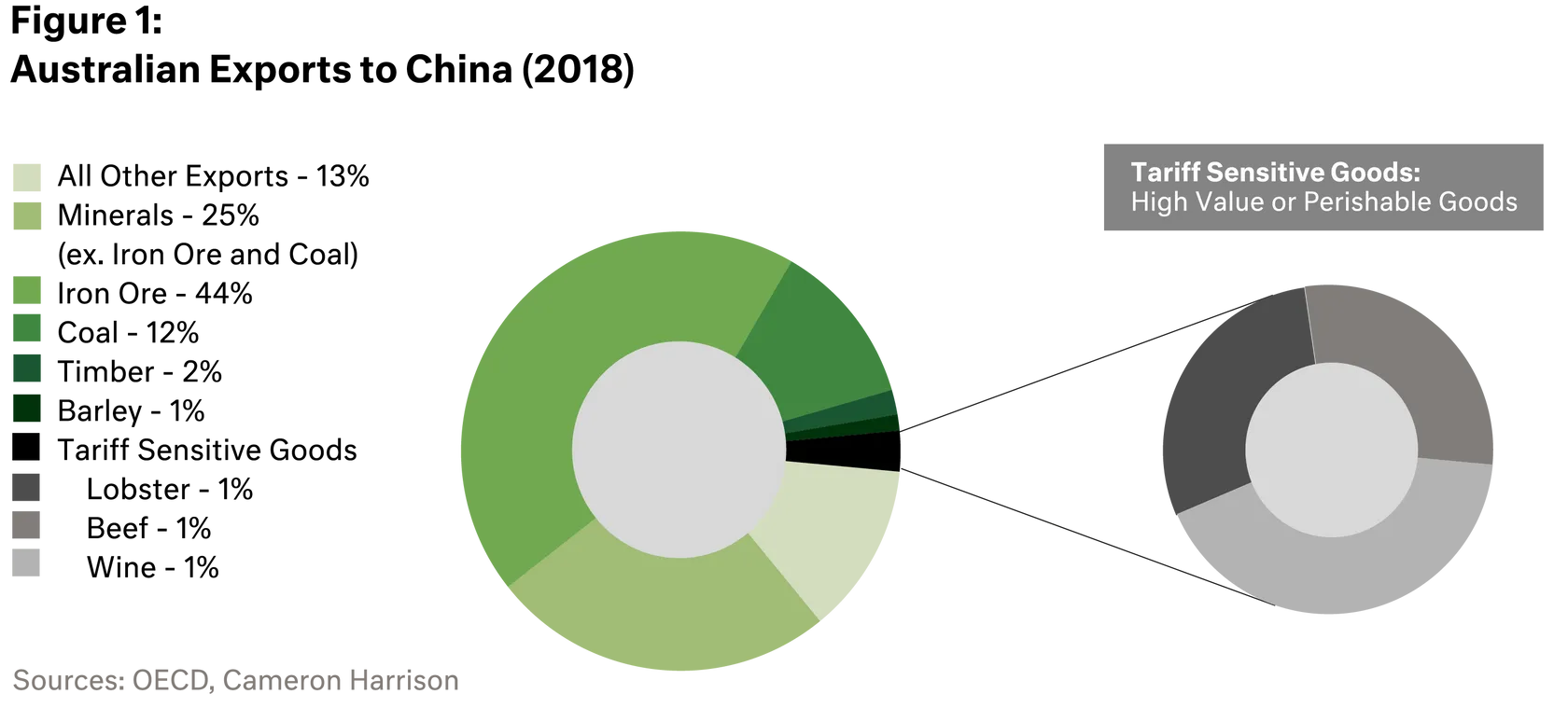

The use of economic coercion through trade is a tactic that has garnered significant media attention, as the list of Australian industries impact continues to grow - to include barley, wheat, coal, lobster, wine, and timber. The trade sanctions make for sensational news headlines, as does the visual of tonnes of lobster rotting in a storage container, but the economic impact will be far less dramatic.

The bulk of the trade targeted by China is in highly commoditised goods (such as coal), where suppliers from other countries will be unable to ramp-up production to meet the Australian shortfall. As recently noted by Glencore CEO, Ivan Glasenberg, the outcome will be that Australian exports will most likely be purchased by other large importing nations (like Japan in the case of coal).

On the other hand, the impact on wine and lobster will be far more severe as they are more reliant on China as a sole importer. For the wine sector, the tariff increase to between 107% and 212%, compared to 12% for beef, will decimate the export market. Likewise, 94% of Australian lobster exports are shipped to China, and it will be very difficult to find new markets for this quantity of product... However, as shown on Figure 1 below, the total value for these goods is relatively small, circa 2-3% of total exports and does not sound the death knell for the Australian economy, despite the headlines.